Sea Limited’s stock price has been on a great run in the past year. With the stock up 442% since the 52 week-low recorded on 20 March 2020, Sea’s shareholders are clearly one of the biggest gainers from the pandemic. Despite the bullishness, Sea’s e-commerce platform, Shopee, remains unprofitable.

Proponents of the stock will cite that Shopee is still investing for growth, and the elevated costs today is justified when it emerges as Southeast Asia’s market leader for e-commerce and reaps the benefit of scale.

But given that in the third quarter of 2020, Shopee already recorded 741 million in gross orders and gross merchandise value of US$9.3 billion, is there not sufficient scale now to be profitable even if at least at the gross profit level? More pertinently, is the unit economics for Shopee viable?

In this article we will explore Shopee’s business model, break down its revenue and cost drivers, and peel back the onion to see if it can achieve profitability.

This assessment matters because if you fundamentally don’t believe Shopee can ever be profitable, then the investment case in Sea breaks down. On the contrary, if you believe that Shopee’s profitability will inevitably go the way of Amazon’s and Alibaba’s e-commerce businesses, then this stock has room to run.

Shopee’s business model

Shopee, like any e-commerce platform, intermediates between sellers and buyers of goods. The company’s revenue comes from charging their sellers transaction-based fees, advertising services, and value-added services.

Transaction-based fees are charged to sellers on a percentage of their selling price. Shopee’s website reveals two main types of transaction-based fees: transaction and service fees. Transaction fees are a flat 2%, while service fees can range from 0% to 5% depending on the participating programme a seller signs up for and the type of products sold.

For Shopee Mall sellers, on top of the two fees, another 3% to 5% in commission fee is charged presumably for listing on a premium platform. Shopee Marketplace sellers do not incur the commission fee.

Advertising fees are likely to be charged by clicks each time a potential buyer lands on a seller’s listing. While there are limited disclosures on how exactly Shopee’s advertising revenues are earned, Alibaba’s Pay for Performance (P4P) model can be illustrative. In Alibaba’s case, sellers primarily bid for keywords that matches product or service listings appearing in buyer search results. The seller with the highest bid in the online auction for keywords will then appear on the buyer’s search result and charged on a cost-per-click basis.

Valued-added services (VAS) are likely to be marketing, product and customer management tools based on Shopee’s data analytics. As a large amount of web traffic comes through the platform, Shopee is able to monetise that data by providing business intelligence to sellers. This could be charged as a subscription-based model. Given that these services are highly automatable, the profit margin for VAS would be higher and will be one of the focus areas for Shopee’s revenue growth.

In terms of the costs incurred to generate the above e-commerce related revenues, as disclosed in their annual report, these are bank transaction fees; service fees paid to third party logistics service providers and warehousing costs for goods, server, and hosting costs; and staff compensation.

Bank transaction fees are probably the most punitive as it is charged as a percentage of the amount being paid by the buyer. This means that there are no scale benefits of lower costs per unit as the bank transaction fees rise in proportion with the value of goods being sold.

Service fees paid to third party logistics service providers are probably able to be recouped as Shopee transfers these costs to both the seller and buyer. It is not immediately clear what proportion Shopee bears for the in-transit logistics cost.

Shopee would prefer to match sellers and buyers within the same country, so that the logistics can be managed domestically at a cheaper cost for both seller and buyer. However, in the case of international shipments, Shopee not only has to incur additional import/export duties but potentially the cost to warehouse goods before handing over to last mile delivery providers.

Server and hosting costs are the costs of both the physical and digital infrastructure needed to maintain its online presence.

Revenue less cost gives us Shopee’s gross profit. Gross profit margin is calculated as gross profit as a percentage of revenue.

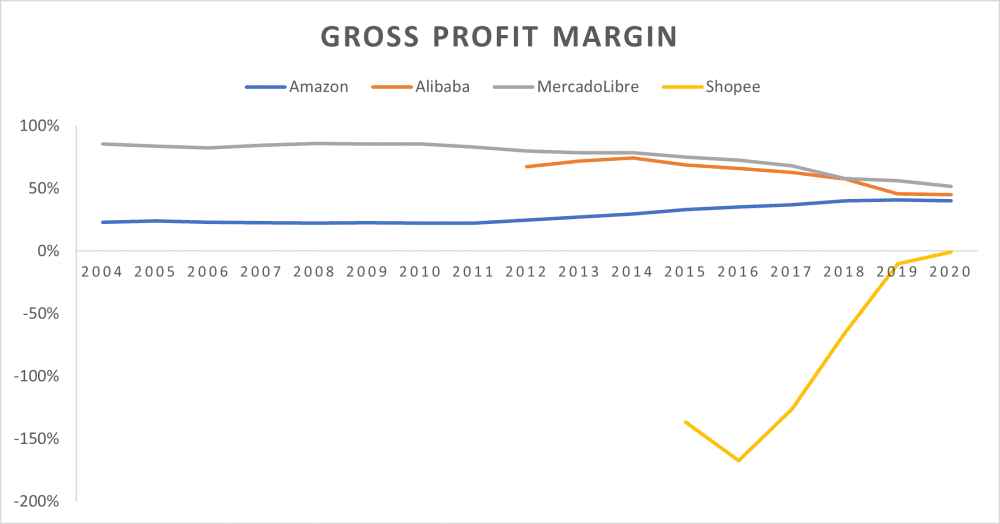

Why is Shopee’s gross profit margin negative and how does it compare to e-commerce peers?

What is most intriguing to me is that Shopee’s gross profit margin is negative. This means that the business is already suffering a loss even before factoring sales and promotion expenses which we know will be significant given the liberal discounts provided, general and admin expenses, and research and development costs.

Exhibit 1: Gross profit margin of Shopee vs e-commerce peers

Compared to e-commerce peers, Shopee is the only company showing negative gross profit (Exhibit 1). In the long history of Amazon and MercadoLibre, especially in the early 2000s, their gross profit margins were consistently positive which are in sharp contrast to that of Shopee.

Nevertheless, the trajectory of Shopee’s gross profit margin is encouraging. We should also be cognisant of the fact that Shopee only began operations in 2015, while its peers have had longer operating histories starting in the mid-late 90s.

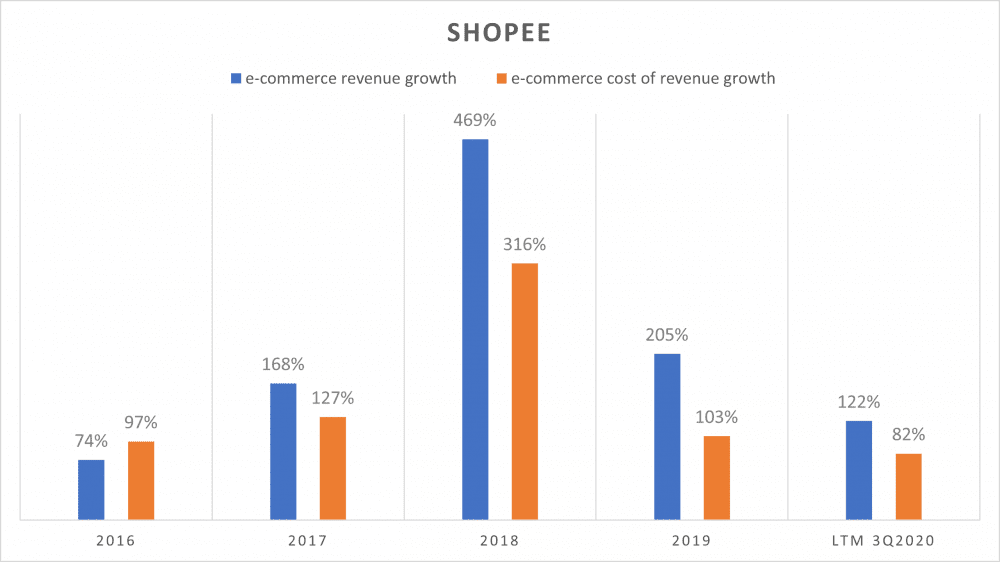

Exhibit 2: Shopee’s revenue vs cost of revenue annual growth

From Exhibit 2, we can deduce that a significant proportion of Shopee’s cost of revenue are variable. As revenue grows, costs increase in tandem. Vice versa, when the growth of revenue moderates so does the growth in the cost of revenue. It is much preferred if Shopee has a lower proportion of cost of revenue that is variable, as this would allow the company to benefit from scale.

One of the main contributing factors for Shopee’s high level of variable costs is due to the bank transaction fees as mentioned earlier. Such fees are charged as a percentage of the selling price and has no benefit to profitability from operating at a larger scale. It is little wonder why Sea had bid for (and won) the digital bank license in Singapore, so that they can cut out the transaction fees currently being paid to the banks. It will be interesting to see if Shopee’s gross profit margin starts ticking upwards once Sea’s bank is up and running.

On a positive note, the absolute growth in cost of revenue is smaller than the absolute growth in revenue since 2017 (i.e. orange bar is shorter than blue bar). This has therefore contributed to the improvement to Shopee’s gross profit margin in the past three years, although it remains negative.

Another indicator I will also be keenly watching for is whether the difference in revenue and cost growths will widen (i.e. how much higher is the blue bar compared to orange bar). This will reflect the pace of gross margin improvements and more specifically whether the fixed component in its cost of revenues have peaked.

Other considerations around Shopee’s profitability

Shopee currently outsources its logistics to third party providers. At some point if not already, the company will have to ask itself if it is better off running the logistics on its own. Alibaba does it through Cainiao, and so does Amazon who operates its own fleet of planes, trucks, and warehouses. Although Shopee passes on the cost of logistics to both sellers and buyers, it should be weighed against whether the overall user cost will be lower if Shopee runs its own logistics network. The lower unit cost of delivery will accelerate the number of transactions (boosting GMV) and could even result in higher profitability with Shopee effectively capturing the current value lost to third party logistics companies.

Geography will also affect the overall cost of running an e-commerce business. Given the varying level of infrastructural development in Southeast Asia compared to China, the United States, and Latin America where its peers operate in, the level of operating cost and efficiency would differ significantly. While Southeast Asia has enjoyed significant infrastructure investments in the past decade, the vastness and fragmentation of the region will likely reflect significant differences in connectivity between larger and smaller cities. The decision to serve both sellers and buyers in certain cities over others will no doubt affect the underlying unit economics.

The fifth perspective: Value or growth?

Howard Marks, in his latest memo, gave his take on the distinction between value and growth investing. His conclusion was that ‘the two should not have been viewed as mutually exclusive to begin with.’ Investing in high-growth companies require a certain foresight into the larger and longer-term trends affecting society. In contrast, investing in value companies are typically based on the traditional concept of observable free cash flows.

It is easy to be sceptical of tech companies with sky high valuations especially when they have not met traditional profitability metrics. The question is therefore whether one has the conviction to accept the proposition that Shopee has a path to profitability.

E-commerce is here to stay in ours and the lifetimes of subsequent generations. The convenience it brings has proven to be lifesaving during the pandemic and it will no doubt remain a pillar of the Internet economy. The fact that Shopee has also entered the daily lingo of everyday conversation proves that it is already passed the tipping point of mass adoption. All that is left as an investor is to critically assess how Shopee’s management is engaging the various levers towards profitability.

Hi TWS,

Thanks for the insight! Would be interesting if you could draw comparison with Lazada instead since they’re going head-to-head in this region.

Cheers!

Hi Darren, it is hard to do a financial comparison with Lazada as it is part of Alibaba and Alibaba does not separately disclose Lazada financials. Qualitatively, though, the growth in South East Asia e-commerce, supported by the relative under-penetration in the internet economy, suggests that the market is large enough to accommodate both players. What I will watch closely are: 1) Evolution of Shopee gross margin, 2) Whether it can sustain high growth in GMV, and 3) Expenditure on sales and marketing as a percentage of total Shopee revenue.

Great article. Is not paying bank transaction fees a significant saving in the big picture of Sea’s costs?

In the long run will there be much more value to Sea from other advantages provided by the digital banking license?

Bank transaction fees: If SEA is earning 3-5% on the value of each transaction (charged to selling merchants on the platform) and have to pay 1-2% to the banks to facilitate the transaction, then it appears to me that bank transaction fees are hefty. There are also costs to executing the logistics but that amount is unclear to me.

Digital banking license: The commonly cited value would be promoting financial inclusion and banking people excluded from the formal banking system. But I yet remain unconvinced. 1) Will SEA be able to underwrite more judiciously than incumbent banks? 2) Will they be financing conspicuous consumption or productive inputs for businesses? 3) I don’t see the value in the business model of a bank which is balance sheet heavy and highly leveraged, more so given SEA’s management have little experience in banking. So in the long run, the jury in my opinion is still out.

Very good article indeed! However, I dont quite understand the fees of bank transfers and also how this cost will be reduced since the got a banking license in Singapore, could you please explain? Thank you!

Hi Daniel, this is because Sea/Shopee becomes the bank itself.