We’ve primed you on what qualitative and quantitative factors to consider when looking for companies with economic moats. We’ve also talk about two companies (Apple & Blackrock) with moats and how they’re amassing wealth at such a rapid pace that leaves all other companies in the dust (and some bankrupt). I’m starting this series of articles to help and initiate you to look for wonderful companies, and you decide when it’s a fair price to invest.

Now the search begins with the elephant in the room: Facebook.

The social media industry

This is a relatively new industry, and with all things new, its growth has been meteoric, and so has the asset prices and euphoria surrounding it. The dot-com bust of 2000 has given the markets a healthy dose of skepticism with people crying “Bubble!” during the string of social media IPOs years ago.

The social media industry is a winner-takes-all industry in that there can be many competitors but only one prevails, essentially monopolizing the market. Proof of that can be seen in the earnings of Facebook compared with Twitter or LinkedIn.

Will Facebook’s dominance last forever? No. There will always be someone, somewhere down the line in the distant future that will usurp Facebook’s throne but that will take immense amounts of creativity, effort, and money to do that.

The metrics used by analysts and companies alike in the social media industry are DAU (Daily Active Users) and MAU (Monthly Active Users). As investors, this is how we can evaluate how fast a company is growing, not by the usual financial metrics, but by how many people use their sites on a daily basis. Financial metrics come in after DAU/MAU to show if the company is successful in monetizing their DAU base.

Enter Facebook

It’s a brand that changed our behavior (similar to Apple) like never before. We walk on the streets with our heads down and eyes locked to our phones checking who liked, commented or shared interesting things. We check our phones at almost every passing minute for messages sent via WhatsApp, or Messenger, or see notifications by Facebook or Instagram.

This level of addiction is unprecedented — even heroin can’t give you the same level of obsession (though I’ve never tried). Tobacco and food companies can only dream of making their consumers this addicted to their products; for all you know they’re relying on Facebook to push their products harder to us.

This is Facebook’s moat – psychological addiction to its services by consumers. Schools teach social media marketing as a new subject and companies have no choice but to move into this area in efforts to capture consumer mindshare. Almost every website has a “Share on Facebook” button, this speaks volumes about Facebook’s wide and global reach.

Facebook has four core businesses:

- Facebook – The app and website sees traffic of more than 1.59 billion people every month, and 1.04 billion every day. This is the main engine that drives Facebook but also integrates its other main core businesses.

- Messenger – It’s a “spin-off” from Facebook as a separate app and has 800 million active monthly users. As of Q4 2015, Zuckerberg guided that Facebook would be investing and integrating new AI, payments and transportation platforms into Messenger, allowing users to request an Uber ride through the app and in the future, airlines as well.

- Instagram – Bought for $1 billion (which I think is a steal) in 2012, this app now has 400 million active monthly users. Instagram is now steering towards more visual content with apps like Boomerang and Layout for users to creatively edit and share multiple images and videos. This is also another earnings driver for Facebook as advertisements can be easily integrated into the platform. There has been no cannibalization of services as 98 of the top 100 advertisers on Facebook also advertise on Instagram as of Q4.

- WhatsApp – Famously bought for $22 billion when it only had about 450 million active users, it currently has 1 billion active monthly users. Plans on monetizing WhatsApp have been vague but it has incredible potential for any sort of monetization efforts due to its sheer size.

Facebook doesn’t disclose its revenue breakdown from Instagram but they do report mobile revenue. Facebook’s management has reported incredible growth in mobile revenues as 90% of Facebook users access it via mobile devices. Mobile MAUs were 1.44 billion as of FY2015, an increase of 21% year-on-year. Mobile advertising revenue comprised 80% of advertising revenue for 4Q 2015, up from 69% of advertising revenue in the 4Q 2014.

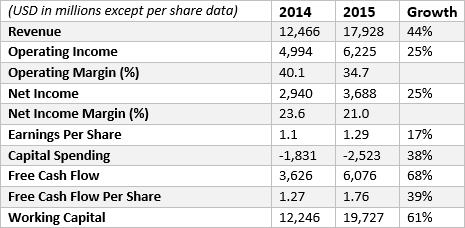

Financials

Facebook’s FY15 revenue grew 44% from FY14 to $17.9 billion, generating free cash flow of over $6 billion with DAU of 1.04 billion people, a YoY increase of 17% (only 5 billion more people to go!). With operating income of $6.25 billion, their operating margin sits at a whopping 34.7%. Again with most “moaty” companies, a fat double-digit profit margin is one very common trait.

Just comparing their latest yearly growth, Facebook saw triple-digit percentage point growth by all measures as monetization of their massive user base kicks in.

However, as with all things famous and wonderful, the market priced in Facebook’s incredible potential and pushed up its stock price to all-time highs. At a share price of $110.56, its market cap sits at $314.7 billion with about $4.7 billion in net cash. It trades at a forward P/E of 30 and P/B of 7. As a growth company, Facebook doesn’t pay a dividend, so buying Facebook’s stock should be mainly for capital gains and a belief that at this current earnings multiple, Facebook can earn its way out or simply rocket even higher.

If you invested in Facebook during its IPO or even earlier last year, you would’ve made a killing as Facebook has finally and successfully monetized its giant user base. Can Facebook still grow at a rapid rate? It could, as they dominate advertising in the social media space; they act as a toll operator collecting more fees on advertisers who want their products to be seen.

If you’ve noticed something, their margins actually dropped despite being fat. That’s is due to their aggressive investments in new ventures and increased capital expenditures. Management has already guided that they would significantly increase investing in these areas. Their next quarter’s earning webcast should reveal just how much they’re increasing it by.

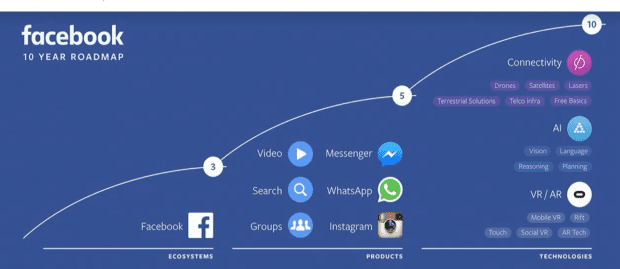

F8 keynote

Source: Facebook

Connectivity

The world’s current population is about 7 billion, growing at about 1.1% annually. Facebook only has 14% of the “market share”; 86% more to go (or 61% if China keeps blocking Facebook). But with many people lacking internet connectivity, it’s tough to grab market share when there’s no infrastructure in place. Most companies would then sit idly by and enjoy their monopoly profits but not Zuckerberg, not Facebook. He would want go a step further to build that infrastructure.

By starting Internet.org, Zuckerberg plans to introduce affordable Internet services to less developed countries. By flying a solar-powered plane to provide internet to hard-to-reach regions. Internet.org is a highly controversial initiative that has been blocked by India for violating net neutrality. These are bold, moonshot initiatives that are typically money-losing which explains the drag on Facebook’s margins.

Artificial Intelligence

AI has been getting more advanced by the day, with the most recent headlines of Google’s DeepMind AI beating Go world champion Lee Sedol. AI can be a potential boon to humanity as it helps automate endless processes to make life easier and now with predictive analytics (yes, those irritating autocorrects are AI-run) and machine learning, we’re headed for the unknown.

Facebook’s AI push can be seen easily. Pictures you upload have tag suggestions of your friends via facial recognition, that’s AI. They’ve recently developed an AI system that combines language and vision comprehension. Show it a picture that it’s never seen and it can answer questions about that picture.

AI is still a black hole and nothing much can be found in their public announcements because it’s highly sensitive and they aren’t legally required to disclose.

Virtual Reality

Facebook’s famed Oculus VR has finally gained traction and hit the streets with over 100 games coming this year albeit with a few snafus in their deliveries. They’ve tied up with Samsung to develop Samsung Gear VR for their Galaxy models. This could be the next big thing like a new console (Wii or Xbox), but it’s still too early to make a call with conviction.

As an investor though…

Facebook with its new, unleashed free cash flow is now free to spend on wild moonshot ideas like many other tech giants. Most of them are money-losing endeavors but in the spirit of free enterprise and innovation only found in Silicon Valley, they could push our world to unimaginable heights.

However, as an investor, one might not support such moves as many are only concerned if they can make money. Early Facebook investors have made a lot of money but as a new investor, how should Facebook treat your interests? Although it has an incredible moat with high earnings power, some may not stomach Zuckerberg’s ravenous appetite for new ventures as it erodes margins. You’d then have to decide if you can entrust your money with Facebook’s current management with full confidence that you’ll reap the reward in the future.