Listed in 2011, Sheng Siong Group Limited is the owner and operator of one of the largest supermarket chains in Singapore. As of 7 July 2019, Sheng Siong is worth S$1.65 billion in market capitalisation. In this article, I’ll give a review of its latest results, long-term financial performance, and valuation ratios.

Here are 12 things to know about Sheng Siong before you invest.

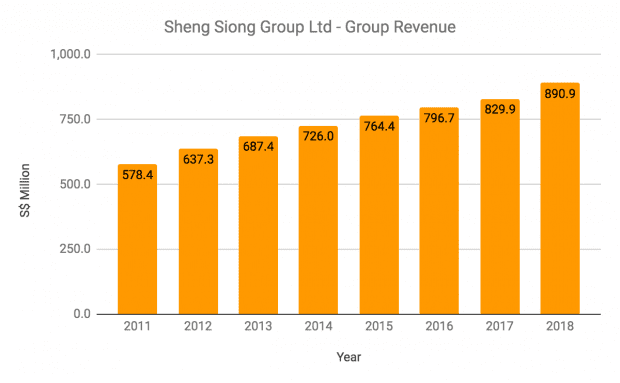

1. Group revenue has grown at a compound annual growth rate (CAGR) of 6.4% over the last eight years, from S$578.4 million in 2011 to S$890.9 million in 2018.

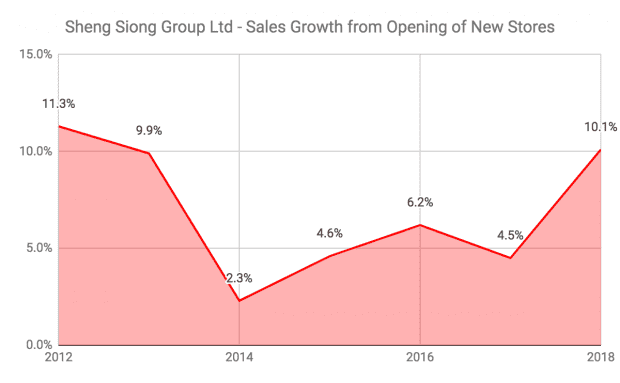

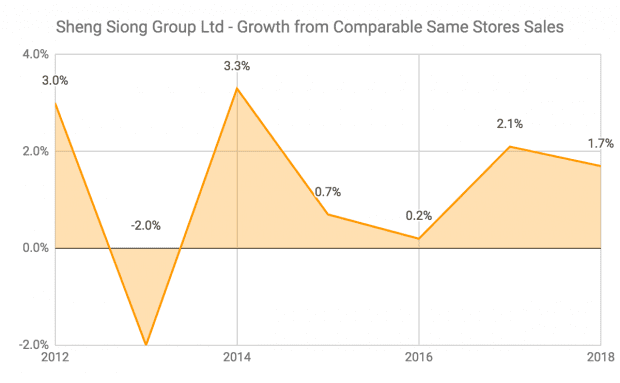

Sales growth has come mainly from the opening of new stores, while same-store sales growth has remained positive every year since 2012, except for 2013. As at 31 December 2018, Sheng Siong has 54 stores in Singapore — an addition of ten brand-new stores from a store count of 44 in 2017. Total retail area increased to 496,200 square feet in 2018 from 404,000 square feet in 2017.

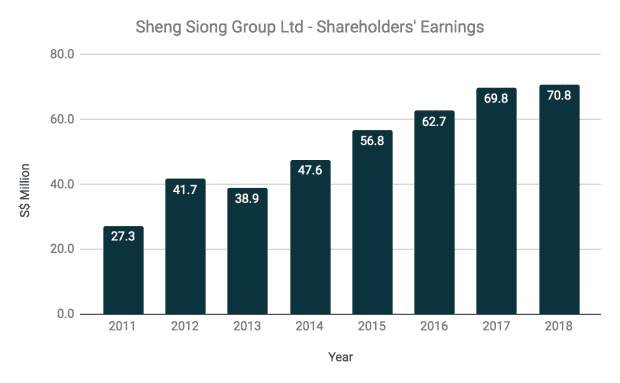

2. Shareholders’ earnings has grown at a CAGR of 14.6% over the last eight years, from S$27.3 million in 2011 to S$70.8 million in 2018. Earnings growth outpaced revenue growth as Sheng Siong incurred lower cost of goods sold as a result of better buying prices, higher rebates given by suppliers for special promotions and volume discounts, and improvements in its product mix.

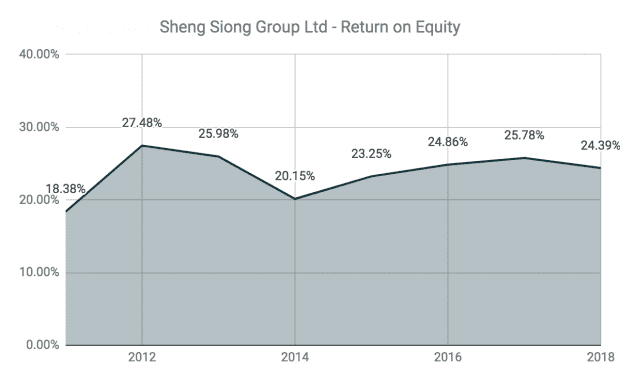

3. Sheng Siong has an eight-year return on equity average of 23.78%. Since 2012, Sheng Siong has maintained an ROE of above 20.0%. As at 31 December 2018, Sheng Siong has no borrowings and S$290.2 million in shareholders’ equity. It has a total of S$170.1 million in current assets and S$141.1 million in current liabilities, which gives it a current ratio of 1.21.

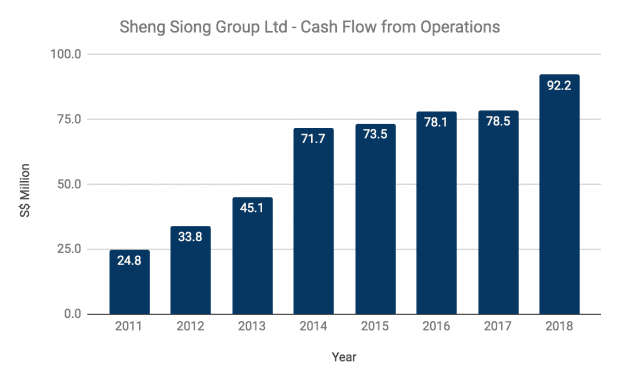

4. From 2011 to 2018, Sheng Siong generated S$497.8 million in cash flows from operations and raised S$157.1 million in equity from its IPO in 2011 and a private placement in 2014. Out of which, it has spent:

- S$293.4 million in net capital expenditures

- S$22.3 million in net repayment of long-term borrowings

- S$326.2 million in dividend payments to shareholders

Sheng Siong is a cash-producing business and doesn’t need to continually raise equity or debt to expand its operations and reward shareholders with dividend payments.

5. As of 15 March 2019, Sheng Siong’s major shareholders and their direct shareholdings are as follows:

| Shareholder | Direct Shareholding (%) |

|---|---|

| Sheng Siong Holdings Pte Ltd | 29.85% |

| Lim Hock Eng | 9.14% |

| Lim Hock Chee | 9.14% |

| Lim Hock Leng | 9.14% |

The Lim family remains influential as they hold stakes in Sheng Siong directly and indirectly through Sheng Siong Holdings Pte Ltd. They also occupy four out of 10 seats at the board of directors and hold the following key leadership positions:

- Lim Hock Eng, executive chairman

- Lim Hock Chee, CEO

- Lim Hock Leng, managing director

- Lin RuiWen (daughter of Lim Hock Eng), executive director

6. In 2015, Sheng Siong rolled out its ‘Hybrid Self-Checkout System’. The system which allows customers to scan, pack and pay for their own items is now in 47 stores and the company is aiming for full implementation by 1H 2019. The system has reduced customer checkout waiting time by more than 30 seconds on average and allowed cashiers to take on roles that enlarge the scope of their responsibilities and skill sets. Sheng Siong is also planning to launch Nets QR code by 1H 2019 which would provide an additional cashless payment option for customers.

7. In 2016, Sheng Siong leased a piece of land measuring 1,800 square metres at 6 Mandai Link located adjacent to its existing warehouse. The following year, it commenced the construction of a new extension to the existing warehouse. Upon completion, it would add another 97,000 square feet of warehouse space for Sheng Siong. The completion was initially scheduled for Q1 2019 but has been delayed to Q4 2019.

8. In November 2017, Sheng Siong opened its first supermarket in China in the city of Kunming. The store incurred a loss of S$0.7 million in 2018, of which Sheng Siong’s fair share of loss was S$0.4 million. The amount is relatively small compared to Sheng Siong’s total earnings of S$70.8 million for the year. Sheng Siong still plans to continue expanding in China and has signed a new lease for a second store in Kunming. The management expects to open the store in Q3 2019.

9. In 2018, Sheng Siong launched its first ‘$tm machines‘ in Singapore at its ITE College Central and Block 417 Fernvale Link stores. The machines allow customers to withdraw cash from their bank accounts. The cash in the $tm machines is topped up from supermarket sales and reduces the amount of cash that Sheng Siong needs to physically deposit at the bank daily. Thus, this helps the company to save on some cash handling charges and improves productivity as the cash will be recycled at its outlets. Sheng Siong plans to install these $tm in all of its stores by 1H 2019.

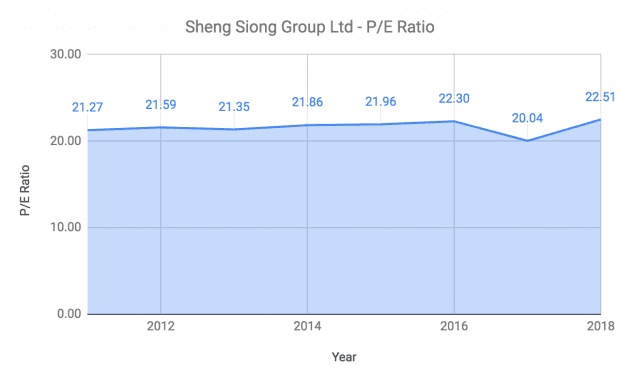

10. P/E ratio: Sheng Siong made 4.71 cents in earnings per share in 2018. Based on its share price of $1.10 (as at 7 July 2019), Sheng Siong’s current P/E ratio is 23.35, which is which is a higher than its average of 21.61 from 2011 to 2018.

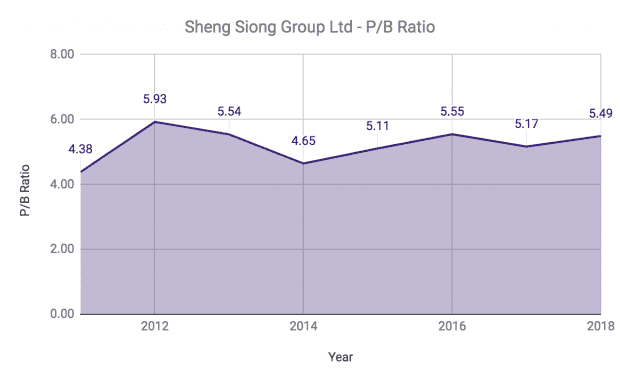

11. P/B ratio: As at 31 December 2018, Sheng Siong reported 19.3 cents in net assets per share. Therefore, its current P/B ratio is 5.70 which is higher than its average of 5.23 from 2011 to 2018.

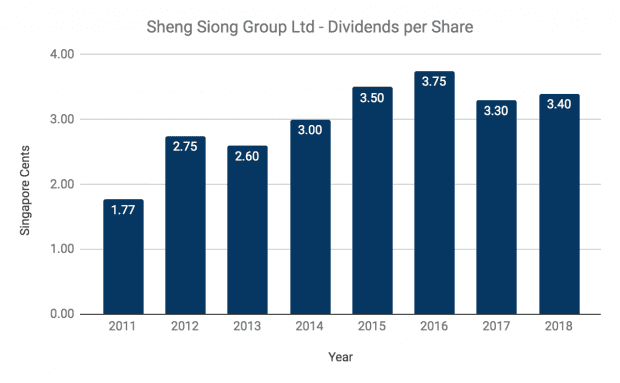

Dividend yield: Sheng Siong has a track record of paying a growing dividend per share (DPS) since its IPO. DPS has increased from 1.77 cents in 2011 to 3.4 cents in 2018.

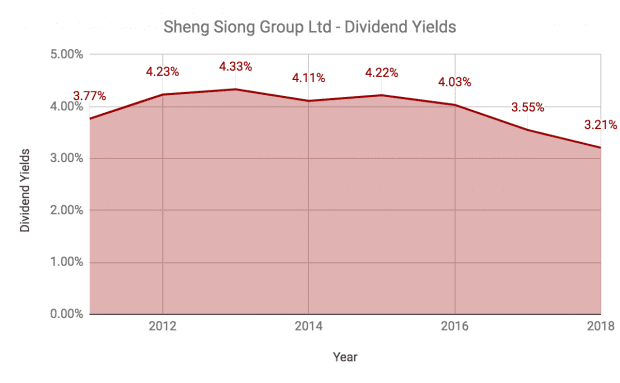

If Sheng Siong maintains its DPS, then its current dividend yield is 3.1% — which is below its long-term average of 3.93%.

The fifth perspective

Overall, Sheng Siong has delivered consistent growth in revenues, earnings, and dividends for shareholders. The company is conservatively run with no debt and S$87.2 million in cash reserves. In terms of valuation, however, the stock is currently trading above its long-term valuation averages, while its yield has fallen to a historical low. An investor may want to wait for a better price before considering Sheng Siong.