The hospitality industry in Singapore has been among the hardest hit industries due to travel curbs imposed in view of COVID-19. Singapore hospitality REITs have seen their share prices crash by 40-50% between the start of year and April, and their share price recovery since then has also been tepid.

However, in a post-pandemic world where normalcy eventually returns, we can possibly expect hospitality REITs to recover as pent-up demand for travel and leisure return. But how do we go about analyzing the hospitality REIT sector?

In this article, I will share four areas you need to analyse before you invest in Singapore hospitality REITs.

1. Operational performance

The performance of hotels can be measured with the following three key indicators:

ADR

Total paid room revenue ÷ Number of paid rooms

An increasing ADR (average daily rate) means that the demand for hotel rooms is outstripping the supply of hotel rooms. This shows that a hotel is increasing the money it’s earning from renting out rooms. However, an increasing ADR can also come about even when occupancy rates in hotels fall. This happens when the revenue collected from hotel rooms falls to a lower extent than the decrease in the number of paid rooms. Hence, it is important we also look at the trend of occupancy rates of hotel rooms.

Occupancy rate

Number of paid rooms ÷ Total rooms available

An increasing occupancy rate of hotel rooms means that the total number of paid hotel rooms is growing faster than the total number of hotel rooms available in the market. This indicates healthy demand for hotel rooms. However, a rising occupancy rate does not necessarily mean an increase in revenue. If a top hotel chain charges a dollar for a night’s stay in its rooms, it would most likely have a 100% occupancy rate. However, this is unsustainable as they are unlikely to cover the maintenance costs and property taxes it incurs. Hence, we must consider both the hotel’s ADR and occupancy rate in our analysis.

RevPAR

ADR x Occupancy Rate

An increase in RevPAR (revenue per available room) means that either ADR or occupancy rates of hotels are rising or both. However, growth in RevPAR does not mean that a hotel’s profits are increasing. RevPAR can increase even with falling revenue and profits. So looking at occupancy rate and ADR figures tells us more about the hotel’s ability to raise prices and fill its hotel rooms.

No single metric of hotel performance should be used in isolation. They should complement one another to plug the gaps in information any one indicator would have. A rising occupancy rate, room rate, and RevPAR are indications of a healthy hotel industry.

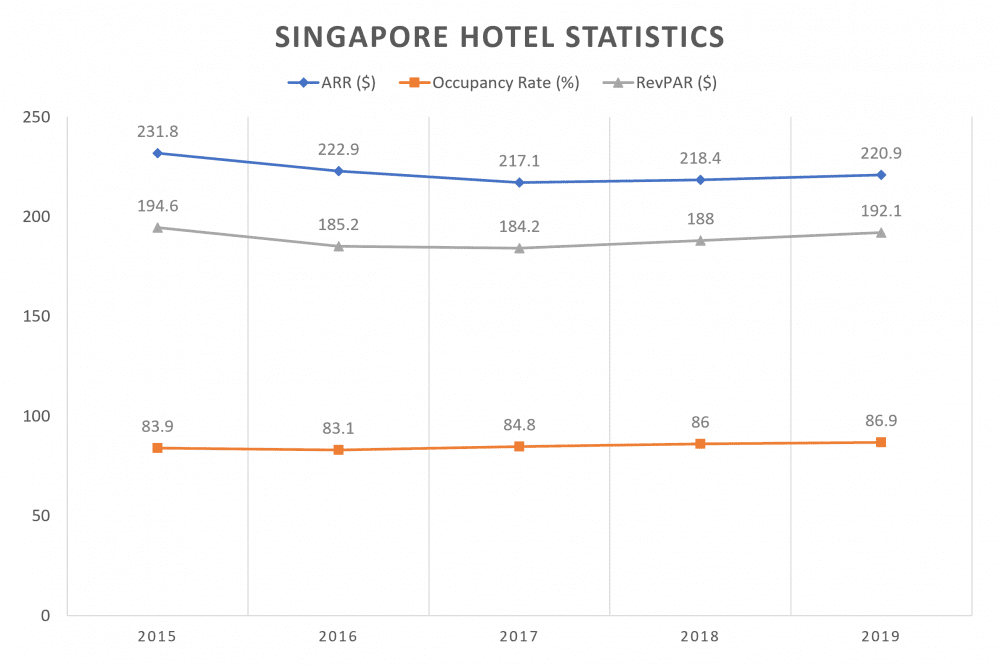

Here’s a snapshot of the Singapore hotel industry’s metrics over the past five years:

Data: You can retrieve Singapore’s hotel statistics under ‘Monthly Hotel Statistics’ from Singapore Tourism Analytics Network.

From 2017, Singapore’s hotel industry seemed poised for a recovery until COVID-19 struck. The recovery was due to the tightening supply of hotel rooms from 2016 onwards and robust demand from the Chinese and Indian markets.

2. Hotel tiers

The figures and trends of the above metrics vary across different hotel tiers. Thus, it is important to observe how the above metrics measure across different hotel tiers. Let’s take a look at the four different hotel tiers as categorised by the Singapore Tourism Board (in an ascending tier order):

- Economy hotels. Generally located in outlying areas with an average room rate in 2019 of S$107.9. (E.g. Hotel Bencoolen at Rochor.)

- Mid-tier hotels. Primarily located in prime commercial zones or immediate outlying areas with an average room rate in 2019 of S$170.1. (E.g. Link Hotel at Tiong Bahru.)

- Upscale hotels. Generally found in prime locations or hotels with boutique positioning in prime or distinctive locations with an average room rate in 2019 of S$264.7. (E.g. Orchard Hotel.)

- Luxury hotels. Predominantly in prime locations and/or in historical buildings with an average room rate in 2019 of S$457.4 (E.g. Ritz Carlton, Raffles hotel.)

The different hotel tiers may not correlate strongly with the overall performance of the hotel industry. There are some hotel tiers which may outperform/underperform the others. We need to identify the hotel tiers that are outperforming the others, so we have a rough idea of which hospitality REITs to look out for based on the types of hotels they own. Investors can then decide which categories are worth putting money into.

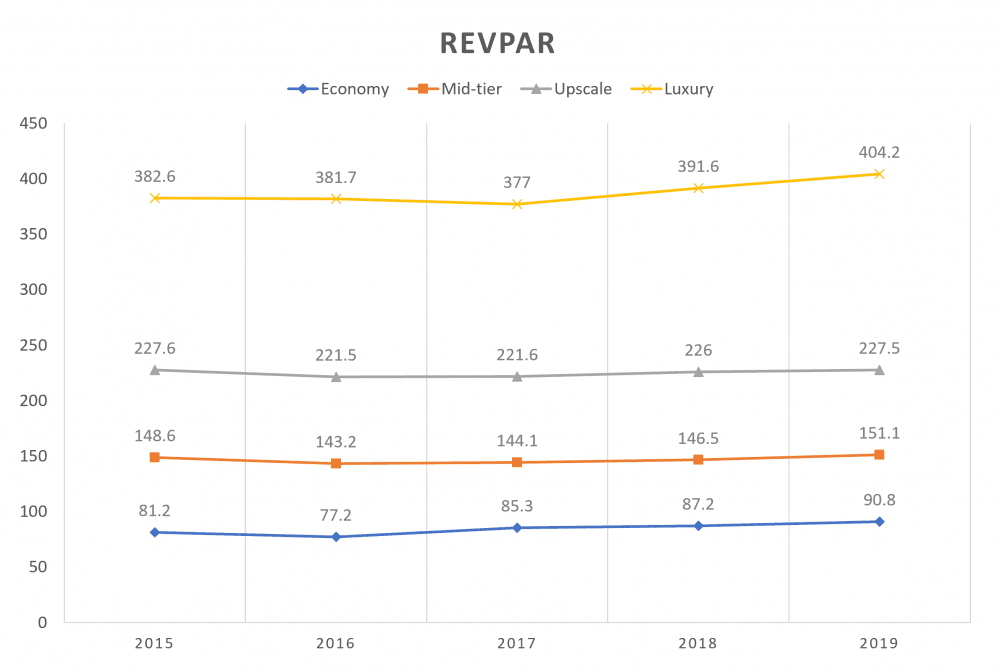

In the chart below, it is clear the economy and luxury hotel tiers are doing much better than the rest in terms of RevPAR over the past five years:

However, as restrictions lift, the mid-tier/upscale hotels could see a recovery in demand first as middle-income travellers remain cautious with their travel spending due to a post-pandemic recession.

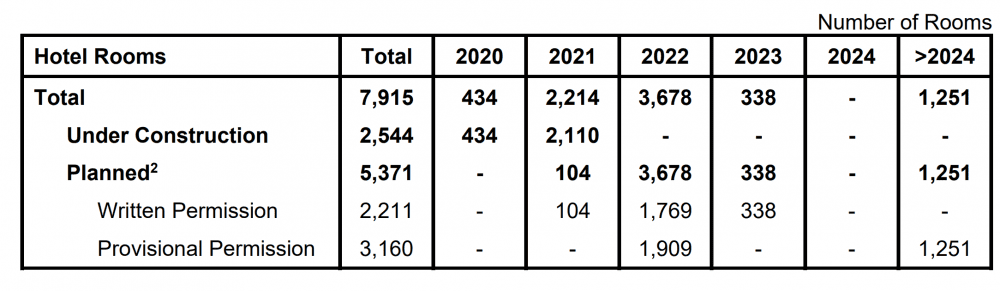

3. Supply of hotel rooms

A limited supply pipeline of hotel rooms is beneficial in adding to a hotel’s profits. A huge supply pipeline of hotel rooms has the opposite effect.

For example, from 2011 to 2016, the average occupancy rate, room rate, and RevPAR of Singapore hotels exhibited a downward trend. Curiously, during this period, there was an upward trend of international tourist arrivals to Singapore, which should prop out those figures. But remember, in any market economy, both demand for and the supply of goods contribute towards the price determination of a good.

As we look closer at the supply side of the hotel market, there was a huge supply of hotel rooms introduced into the market during this period. Hence, the downward trend can be mainly attributed to the huge influx of hotel rooms in Singapore, which outstripped demand during this period. Before COVID-19, some industry observers were optimistic about Singapore’s hospitality sector partially due to the restricted supply of hotel rooms in the coming years from 2019 onwards.

So do not be fooled into thinking that a hospitality REIT will automatically do well just because of a headline that reads ‘International tourist arrivals up in Singapore’. The supply side in any equation matters as well.

Data: Click on ‘Pipeline supply of office and retail space, and hotel rooms’ on the URA website. You will be able to view the supply pipeline of hotel rooms in the coming years. If you are analysing office and retail REITs, the supply pipeline of office and retail space is also available in the PDF. Updates are refreshed quarterly by URA.

4. Macro outlook

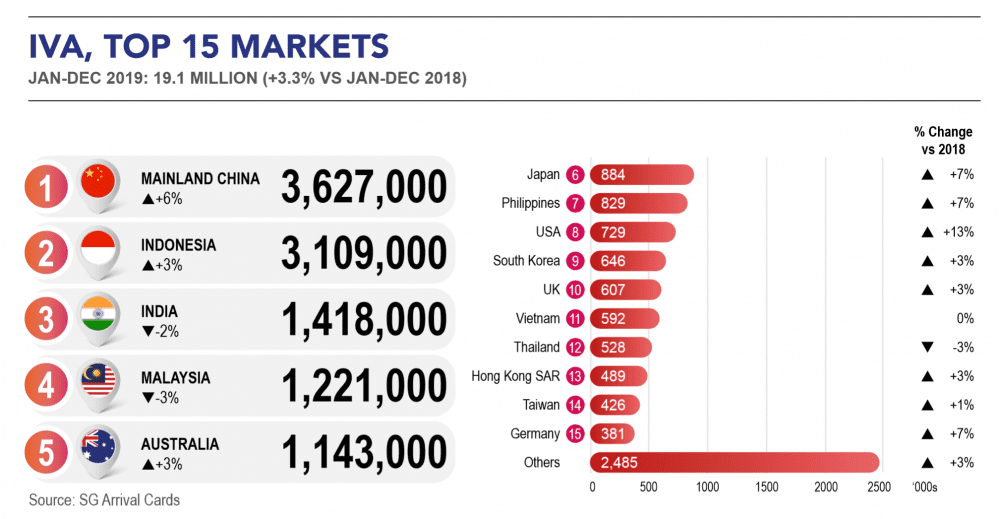

Singapore’s largest tourist markets

Singapore’s tourism industry is very reliant on visitors from China, Indonesia and, increasingly, India. Slowing GDP growth in these countries could dampen the mood to travel, especially since travel is discretionary spending. We want to see strong economic performances from countries that contribute greatly to Singapore’s inbound arrivals. This needs to be matched with strong increases in tourist arrivals and spending by visitors from these countries.

Forex risk

A strong Singapore dollar against the yuan, rupiah, rupee would make Singapore’s goods and services more expensive in the visitors’ local currencies, deterring travel. A weak Singapore dollar has the opposite effect. A weakening dollar also allows Singapore hospitality REITs who derive some of their income abroad to record higher earnings in Singapore dollars.

Geopolitical tensions

Some examples on how geopolitical tensions can affect Singapore’s tourist industry:

The U.S.-China trade tension led by President Trump’s nationalistic inclinations has already led to a slowdown in trade and a subsequent slowdown in GDP growth for China. However, this also means new winners. The diversion of supply chains from China to Vietnam and Thailand has led to positive economic effects for both Southeast Asian nations. But overall, the global slowdown in GDP growth, especially from China, will not bode well for Singapore’s tourist industry.

The high-speed rail (HSR) between Singapore and Kuala Lumpur was supposed to help improve connectivity and economic ties between the two capitals. The HSR connects both cities within 90 minutes, instead of four hours by car. However, the project has been stalled since Malaysia requested to suspend construction of the HSR in 2018. At the moment, the project remains in limbo and the two countries aim to resume discussions by December 2020.

If the project falls through, this means that the projected increase in tourist numbers from Malaysia in Singapore would be affected. Hence, political uncertainties like this will have an impact on Singapore’s tourist numbers.

A closer look at Singapore hospitality REITs

Bear in mind that the above analysis of the hospitality industry was largely conducted in Singapore’s context. It’s important to realise Singapore hospitality REITs also own hospitality-related properties outside of Singapore as well.

Here are the five hospitality REITs listed on the SGX, the main geographic segments they operate in, and the types of hotels they own in their portfolio:

| REIT | Top 3 Geographic Segments | Hotel Tier |

|---|---|---|

| ARA Hospitality Trust | U.S. 100% | Premium/Upscale |

| Ascott Residence Trust | Japan 25%; Singapore 19%; France 16% | Upscale |

| CDL Hospitality Trust | Singapore 62%; New Zealand 12%; UK 9% | Mid-tier/Upscale |

| Far East Hospitality Trust | Singapore 100% | Mid-tier |

| Frasers Hospitality Trust | Australia 36%; Singapore 25%; UK 16% | Mid-tier |

The above table tells us several things about the characteristics of Singapore hospitality REITs:

- Only one hospitality REIT has all its properties located in Singapore (Far East Hospitality Trust)

- One hospitality REIT has all its properties located in the U.S. (ARA Hospitality Trust)

- The other three hospitality REITs have their properties located around the world, with Singapore making a sizable portion of portfolio

- Most of the hospitality REITs’ portfolio of properties are in the mid-tier/upscale hotel tiers

The above points carry several implications when we analyse Singapore hospitality REITs.

Just because the REIT is listed on the SGX does not mean all of its properties are located in Singapore. Hence, if you are looking to invest in Singapore hospitality REITs, it is not sufficient to analyse only the Singapore hotel industry (unless you are looking to invest in Far East Hospitality Trust). You need to analyse the hotel/tourism industries of countries which the REIT’s properties are located in as well.

Just because the hotel industry is doing well overall does not necessarily mean that hospitality REITs will do well too. For example, the stock performance of Singapore hospitality REITs has been sluggish over the past few years despite the decent growth of Singapore’s tourism and hotel market. This is partly because they own mostly mid-tier to upscale properties which have, unfortunately, not benefited from the recent boom in the Singapore hotel industry prior to COVID-19.

The fifth perspective

The travel sector is cyclical as it tends to follow the trend in the overall economy. We also know that the travel can be affected with the snap of a finger — when terrorists strike, pandemics happen, natural disasters occur, or political transitions take place. So if you are looking to invest in hospitality REITs, be prepared to stomach some volatility along the way.