Retail investors are drawn to real estate investment trusts (also commonly known as REITs) because of the passive income they offer. Sinagpore REITs can fetch a decent yield, ranging between 5-8% per annum.

While REITs are great vehicles to build a dividend portfolio, you will still need to pick the right ones at the right price in order to grow your portfolio and maximise your dividends.

So what are REITs?

REITs are investment trusts that pool investors’ money to buy and own income-producing real estate. These properties are leased out to tenants who, in turn, pay rental income to the REIT. Like all property investors, REITs can also acquire new properties, enhance and improve existing ones, or increase rental rates to grow their income.

As an investor, you are entitled to receive a share of the rental income received by the REIT without ‘lifting a finger’.

Here’s an example…

Ever been to Plaza Singapura?

Plaza Singapura is owned and run by CapitaLand Mall Trust. If you remember, Plaza Singapura used to be a single building. In 2013, an extension was created, increasing the net lettable area by 25% and attracting new tenants like Tim Ho Wan, Uniqlo, The Face Shop, etc.

With more tenants paying rent, this also means more income that will be distributed to you as a shareholder. In a nutshell, that’s how REITs work.

As of 31 December 2019, there are a total of 43 REITs and property trusts listed on the Singapore Exchange, each of them with a portfolio of properties ranging from malls, offices, hotels, hospitals, and factories.

Investing in REITs vs. physical property

So why Singapore REITs? Why not own and invest in a physical property instead?

There are several key benefits to investing in REITs compared to a physical property:

1. Low startup capital

Owning one property in Singapore can be expensive, let alone having enough to invest in a second one. However, REITs give retail investors a chance to enter the property market ‘cheaply’.

You can get started for around as low as $200 (e.g. 100 shares of CapitaLand Mall Trust as of 30 July 2020) and start receiving your dividends in the next few months. This is much more financially manageable for most people compared to coming up with a hefty six-figure sum just for the downpayment for a physical property.

2. High liquidity

Because REITs are traded on stock exchanges like any other stocks, they are very liquid. That’s to say you can buy shares in a REIT today and sell the very next.

On the other hand, if you want to sell a physical property, the whole process of doing so can take several months to complete because you need time to find a buyer, negotiate a price that both parties are happy, and so on.

3. Diversified risk

Another key advantage when it comes to investing in REITs is that you are not investing in a single property, but multiple properties with a wide variety of tenants. Tenant risk is well-diversified if you can pick the right REITs to invest in.

On the contrary, when you invest and own physical properties, you need to find your own tenants to lease your properties to. If you can’t find any and the properties are left sitting for several months, you run the risk of heading into negative cash flow. For REITs which are able to attract quality tenants to due to the quality of their properties, the risk of not being able find tenants is mitigated.

4. Tax exemption

When you sell or lease your property, those earnings are subjected to an income tax of up to 20% (depending on the type of property).

For REITs, however, they are exempted from the normal 17% corporate tax rate if it distributes at least 90% of its distributable income to investors as dividends. Because of this, REITs earn a higher income and investors earn higher yields. This tax transparency status is currently effective until 31 March 2025.

5. Hassle-Free

When it comes to property maintenance and the need to deal with tenant requests, the REIT’s property manager takes care of all of them. This includes finding tenants, negotiating the rents, handling the cleaning services, electric bills, etc. This can really help save you a lot of headache especially if dealing with people isn’t really your cup of tea.

The upside of owning and investing in physical properties is that it allows you to use leverage to buy properties. Because of the lack of leverage when investing in REITs (and here’s why you shouldn’t borrow to invest in the stock market), they may not fetch higher capital gains compared to physical properties.

That said, REITs are still one of the best vehicles to build a passive income portfolio that grows over time and should not be overlooked if you want a piece of Singapore’s property pie.

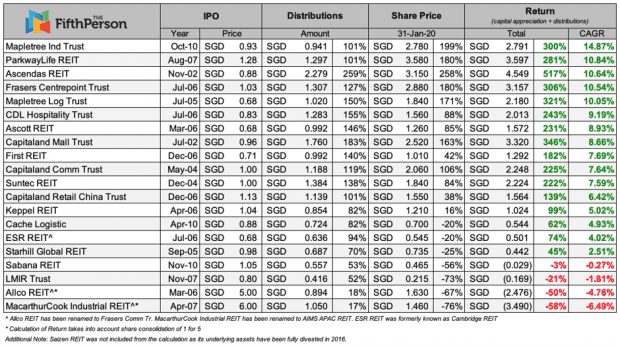

Here’s a look at the historical returns of Singapore REITs since their IPOs:

Please note that past results are not indicative of future performance.

You can see that some REITs have fetched amazing returns, while some have fallen into negative territory.

So the question is, how do you pick the right REITs to invest in?

[cboxarea id=”cbox-d4CTvekj1Gh5nOl6″]Not all REITs are created equal

Which is why you can’t use a one-size-fits-all approach when looking at them as a whole.

For example, healthcare REITs may not fetch higher yields, but the quality of the assets they own and the sector they operate in is more resilient when compared to, let’s say, industrial REITs.

So it is important to know which sector(s) a REIT operates in and compare it to other REITs within the same sector.

REITs operate in five broad sectors:

Retail

As a Singaporean, it is almost impossible to miss retail REITs. These REITs own and manage shopping malls and are probably the most intuitive to understand for the retail investor.

An example of a retail REIT is CapitaLand Mall Trust, which owns malls like Tampines Mall, Raffles City, Plaza Singapura, Bedok Mall, etc. Another example is Frasers Centrepoint Trust which owns malls like Causeway Point, Waterway Point, and Northpoint among others.

Retail REITs usually own two types of retail properties: prime malls which are located in urban areas and suburban malls which are generally located in the heartlands. If you are new to Singapore REITs, you may want to embark on doing research on retail REITs first.

Office

Office (or commerical) REITs own office buildings and earn their income through leasing office space to tenants.

Examples of office REITs in Singapore are CapitaLand Commercial Trust which owns Capital Tower, Asia Square Tower 2, etc.; and Keppel REIT which owns Ocean Financial Centre, Marina Bay Financial Centre, etc.

Office REITs tend to be cyclical in nature and investors are more exposed to the vagaries of economic cycles. So if you are into office REITs, it is important to understand economic conditions and which part of the cycle we are in.

Office REITs usually have longer lease terms (compared to retail REITs) as tenants tend to sign longer leases to house their office operations.

Hospitality

Hospitality REITs own hotels and serviced apartments. They typically earn a pre-determined fixed rent from a master lease from the hotel operator as well as variable income based on the booking of rooms.

An example of a hospitality REIT in Singapore includes Far East Hospitality Trust which owns hotels and serviced apartments such as Quincy Hotel, Rendezvous Hotel, Village Hotel, Regency House, etc.

Hospitality REITs can be very affected by economic cycles and external shocks like pandemics or terrorist attacks which affect tourism in a country.

Healthcare

Probably the most stable of all REITs are healthcare REITs. They own hospitals and nursing homes, and generate income by leasing them to healthcare tenants.

The healthcare industry is defensive in nature and relies on non-discretionary spending to keep its operations running. Healthcare REITs tend to have a long-term master lease since the cost of hospital infrastructure is very high and relocating operations are expensive. Barriers to entry in the healthcare industry are high and it is less prone to a situation of oversupply.

Because of their steady dividends, healthcare REITs normally have lower dividend yields due to their popularity among investors. An example of a healthcare REIT in is Parkway Life REIT which owns Mount Elizabeth Hospital and Gleneagles Hospital in Singapore.

Industrial

Industrial REITs own industrial buildings such as factories, warehouses, and distribution centres. Examples of industrial REITs include Ascendas REIT, Cache Logistics Trust, and Sabana REIT.

Industrial REITs tends to have the highest yields among all the REITs. This is mainly due to the fact that the land lease expiry of industrial properties are a lot shorter. And just like offices, industrial REITs are largely affected by economic conditions and cycles. At the same time, this sector is also seeing more demand right now due to the growth of e-commerce.

Now that you know the different sectors REITs operate in, the next step is to evaluate their metrics.

How to pick the best REITs to invest in

When it comes to picking which REITs to invest in Singapore, you can’t just look at dividend yield alone. You need to assess the quality of the properties they own and if the REIT has any expansion plans – be it via organic or inorganic growth.

Here is a quick breakdown of the five metrics you need to pay attention to when it comes to analysing a REIT:

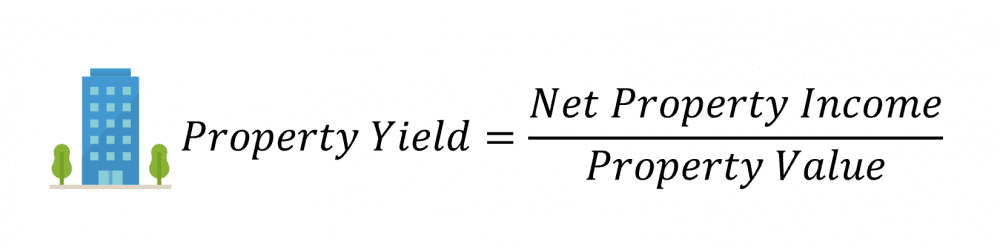

1. Property yield

Property yield is the amount of net property income a property generates as in comparison to its property value. The higher the property yield, the better.

As we mentioned, you want to make an apple-to-apple comparison between REITs in the same sector. For example, you’d want to compare the property yield of CapitaLand Mall Trust with another retail REIT in Singapore like Frasers Centrepoint Trust, and not with an industrial REIT for example.

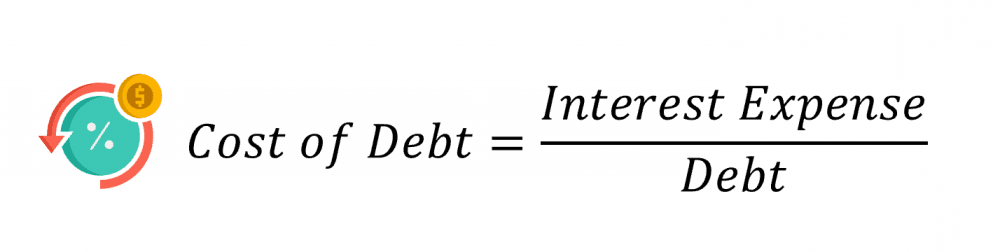

2. Cost of debt

Cost of debt is essentially the effective interest rate a REIT pays for its borrowings. The lower the cost of debt, the lower the interest the REIT pays.

REITs from different sectors will have different costs of debt. So you want to compare a REIT’s cost of debt to other REIT within the same sector.

A REIT with a lower interest rate is often a sign that they are more establihsed and own higher-quality assets. Thus, lenders are comfortable charging them a lower interest rate compared to their peers.

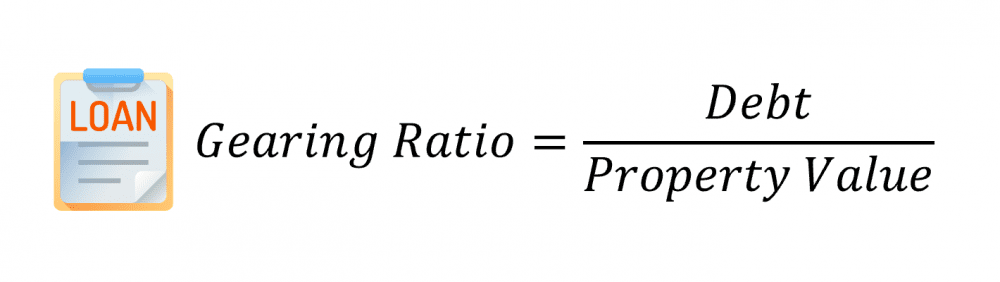

3. Gearing ratio

The gearing ratio is the REIT’s total debt compared to its total assets. The higher the ratio, the more leveraged a REIT is. In Singapore, REITs are only allowed to borrow up to 50% of their total assets.

We prefer REITs to have a gearing ratio of below 40% because it allows them some buffer in case the property market crashes. During a crash, the value of properties will drop and this results in the gearing ratio increasing. At the same time, if the market is doing well, the REIT with a lower gearing ratio will have more debt headroom to borrow money to acquire yield-accretive properties.

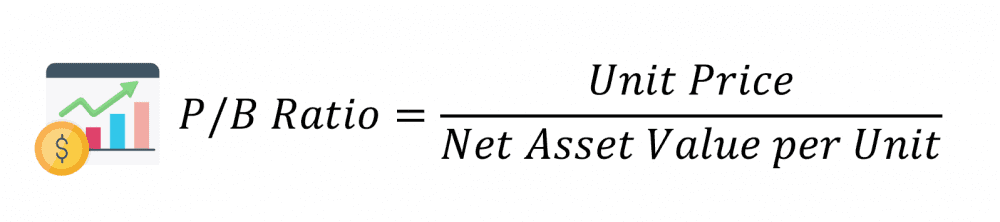

4. Price-to-book

Another metric to consider is the P/B ratio which compares a REIT’s unit price to its net asset value (NAV) per unit. Theoretically, a P/B greater than 1.0 means that the REIT is overvalued, while a P/B lower than 1.0 means that the REIT is undervalued. However, as an investor, you should not rely on this simple interpretation of the P/B ratio to make buy/sell decisions.

Since different REITs can own different kinds of assets (of varying quality), the market may consistently price a REIT above or below its NAV for long periods of time.

So what can do to value a REIT instead is to plot its historical P/B ratio over the past five to ten years, and compare that to its current P/B ratio to find out if a REIT is over/undervalued.

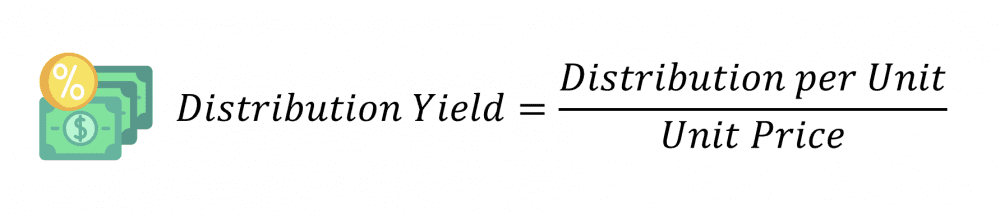

5. Dividend yield

Dividend (or distribution) yield measures the amount of dividend paid as a percentage of unit price. One of the biggest mistakes new investors make when it comes to investing in REITs is that they tend to focus on dividend yields alone.

In simplest terms, the higher the yield, the more attractive the REIT. But this is rarely true, because in many cases an extremely high yield typically points to a risky investment.

What you want to look for instead is a consistent and growing distribution per unit (DPU), which is a better indication of a REIT’s ability to grow your yield on cost over the long run.

To view a summarised table of these five key metrics for Singapore REITs, you can visit Singapore REIT data.

To learn more about the five metrics and how we apply them during our REIT analysis, you can watch the video below:

What if you don’t have time to do any research?

If you want some REIT exposure in your portfolio but don’t have the time to analyse and pick the best individual REITs, you can always invest in a basket of REITS through a REIT ETF.

There are currently three REIT ETFs with Singapore REIT exposure:

- Lion Phillip S-REIT ETF. This is the only pure play Singapore REIT ETF which comprises 26 Singapore REITs including CapitaLand Mall Trust, Mapletree Commercial Trust, Ascendas REIT, and Manulife US Real Estate Investment Trust.

- Phillip SGX APAC Dividend Leaders REIT ETF. This REIT ETF gives you exposure to REITs in Hong Kong, Australia, and Singapore. This fund comprises 30 REITs and count Ascendas REIT and CapitaLand Mall Trust among its top 10 holdings.

- NikkoAM-Straits Trading Asia ex Japan REIT ETF. This REIT ETF that gives you exposure to 27 REITs Singapore, Hong Kong, Malaysia, and Indonesia. Its current top three holdings are Ascendas REIT, Link REIT, and Mapletree Logistics Trust.

While ETFs give you instant diversification and removes the headache of picking which REITs to invest in, you tend to average out your returns by investing in a large basket of REITs.

We personally prefer to pick individual REITs as it gives us more control over the opportunities that are available in the market, which can result in higher yields and returns over the long run.

So what’s next?

REIT analysis and updates

To help you save time, we have compiled a list of Singapore REIT articles below to help you get up to speed of how these Singapore REITs we’ve covered have been performing over the years:

- Ascendas Hospitality Trust

- Ascendas REIT

- CapitaLand Commercial Trust

- CapitaLand Mall Trust

- Frasers Centrepoint Trust

- Frasers Logistics and Industrial Trust

- Mapletree Commercial Trust

- Mapletree Logistics Trust

- Parkway Life REIT

When it comes to REITs, remember to focus on the quality of their assets and the REIT manager’s ability to continually grow the DPU over time. This way, not only will you see your dividends grow over time, you’ll most likely enjoy decent capital gains as well as the value of the REIT grows over the years.

Dear The Fifth Person,

What are your views on Syfe?

Hi Stella,

We haven’t reviewed Syfe, so we ‘re unable to comment. Just like any fund manager you entrust your money with, make sure the manager is reputable and aligns with your financial goals.

Hi, What amount would you recommend if I were to start a portfolio of dividend generating stocks? and is Singapore good enough or what other countries should I look into?

Thank you.

Hi Tommy,

Singapore and Hong Kong are great as dividends are tax free in both these countries.

You can always start small and build your portfolio over time. We suggest at least $2.5K to start because most Singapore brokerages charge $25 per trade and that would keep your brokerage fees to around 1%. Hope this helps!

https://fifthperson.com/how-much-money-do-you-need-to-start-investing/

Sreit also tax free?

Yes, Singapore REITs enjoy tax exemption status.

If Malaysian wanna buy then can tax exemption?

Yes, Singapore has no capital gains or dividend tax.

Hi! Are work pass holders can invest in REITs?

Hi Elaine, yes you can!

Hi. Just to stretch it a little. Most of the overseas dividends be it from REITs or income stocks are subject to withholding taxes which can eat up quite a significant amount of income esp since they don’t get much capital gains generally. Can we avoid this by buying mutual funds or etf with dividend reinvestment? In this case the dividends are technically not distributed by reinvested by the fund manager hence not subject to withholding tax and when we sell, we sell the basket of funds which include the reinvested dividends that form part of the capital gain

Hi Charles,

You can’t avoid the withholding tax either by investing in funds/ETFs; it will still be deducted before reinvestment.

Hi,

Can you advise if I should hold on to Lippo Malls Trust or should I cut losses?

Your advice is appreciated.

Thanks

Jack