Imagine working hard to save and invest money for your future financial freedom. With each penny saved, you’re one step closer to your dream. However, there’s one factor that often gets overlooked by most people – investment fees. These fees may seem small, but over many years, they can really add up and eat away at your investment returns.

Investment fees come in different forms – management fees paid to fund managers, operating expenses for mutual funds and ETFs, and transaction costs for buying and selling. While these fees don’t seem like much on their own, they steadily chip away at your hard-earned savings over decades.

Understanding investment fees is crucial for making smart investing decisions. Each fee takes a little bite out of your returns, slowly diminishing what you’ve worked so hard for. The different fee structures can initially seem complicated, but knowing them allows you to maximise your investment growth.

In this article, let’s examine how investment fees impact your long-term savings goals and explore strategies to minimise these costs. By better understanding these fees, you can protect your portfolio from unnecessary opportunity costs down the road.

Common types of investment fees

1. Management fees: These are fees charged by mutual funds, exchange-traded funds (ETFs), or investment advisors for managing your investments. They are typically expressed as a percentage of your assets under management.

2. Load fees: These are commissions charged by some mutual funds when you buy (front-end load) or sell (back-end load) shares. Load fees compensate brokers for their services.

3. Account maintenance fees: These are annual fees charged by some brokers or funds for maintaining your investment account.

4. Redemption fees: Some funds charge this fee if you sell shares within a certain period after purchase to discourage short-term trading.

5. Inactivity fees: Some brokers charge fees if there is no activity in your account over a certain period.

Case study

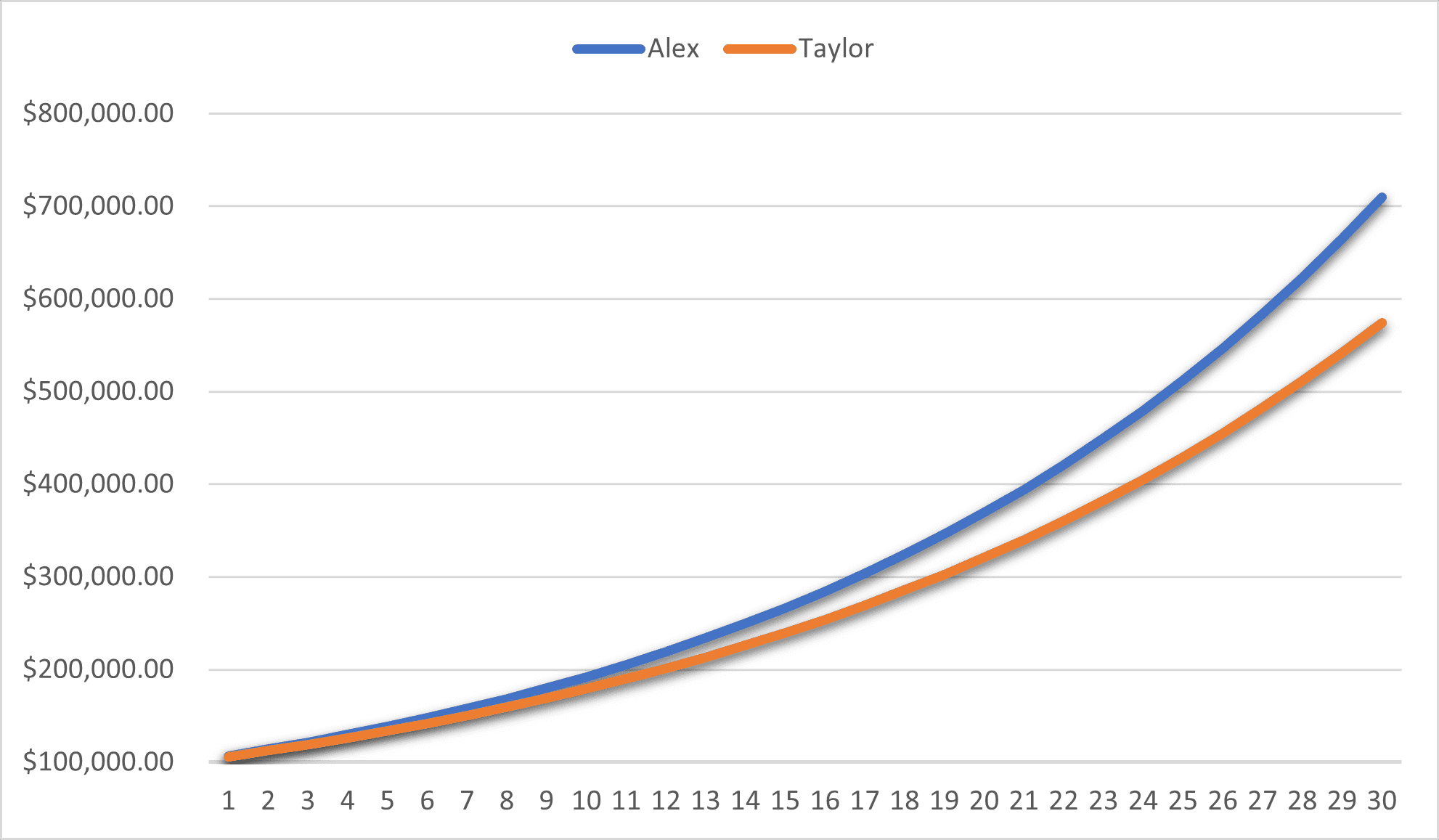

Consider two investors, Alex and Taylor, who put $100,000 into different mutual funds for their retirement savings over 30 years. Alex chose Fund A with a 0.25% annual fee, while Taylor picked Fund B with a 1% annual fee – just a 0.75% difference.

At first glance, that small fee gap seemed trivial. However, the compounding effect caused a massive gap in their final nest eggs over three decades. With both funds averaging 7% annual returns before fees, Alex’s lower-cost Fund A grew to $$709,637. But Taylor’s higher-fee Fund B ended up at $574,349.

That’s a staggering $135,288 difference, all due to the slightly higher fees Taylor paid compounding over 30 years. While 0.75% seemed negligible upfront, it dramatically eroded Taylor’s investment growth in the long run.

This case study underscores a crucial lesson: Knowing about investment fees and choosing low-cost options is just as important as picking good investments. The fees you pay today have a multiplying effect over decades, significantly impacting your future wealth.

The takeaway is clear: do not underestimate the corrosive power of high fees over long periods. A small percentage point difference can translate to a massive disparity in your retirement savings. Minimising costs through low-fee funds can mean hundreds of thousands more for your golden years.

Low-cost investment vehicle

One of the best tools for individual investors to minimise fees and maximise returns is low-cost passive investment products like index funds and exchange-traded funds (ETFs).

These investment vehicles are designed to be highly efficient and low-cost. Instead of paying higher fees for active management, index funds and ETFs simply track a market index like the S&P 500 using a rules-based approach. This streamlined strategy requires less hands-on oversight, translating into much lower overall investor fees.

The beauty is that you can get market-matching returns while keeping more of your money working for you rather than paying high fees that eat away at growth over time. By choosing these low-cost options, a larger portion of your investment continues compounding and building wealth year after year.

In addition to lower costs, index funds and ETFs provide great diversification, making them an easy, hands-off way for beginners to build a simple but effective portfolio across the entire market.

Regular portfolio review

Regular portfolio check-ups are crucial for identifying any investments that may be costing you too much in fees or funds that have changed their fee structures. By reviewing your holdings at least once a year, you can stay on top of hidden costs, high expense ratios, and underperforming funds bogged down by excessive fees.

These days, many user-friendly online tools and resources make it easy to see the fees and performance details for all your investments. With just a few clicks, you can easily spot which funds are charging high fees and evaluate if it makes sense to switch to lower-cost alternatives.

When reviewing your portfolio, prioritise funds with a clear and transparent fee structure. Avoid any institutions that disclose fees in a confusing or opaque way, making it difficult for individual investors to understand the full costs. Instead, pick funds that provide straightforward fee reporting, empowering you to make well-informed decisions confidently.

Look for disclosures that break down every charge, including management fees, administrative costs, trading commissions, and any upfront or backend sales loads. Simple, easy-to-understand fee information lets you see exactly how much you’re paying in fees versus how much is going towards investment growth.

Funds with transparent, readily understandable fee structures tend to align better with investor interests. They promote trust and healthy competition, driving other funds to streamline fees and offer more cost-effective options over time.

The fifth perspective

The impact of investment fees should never be disregarded, no matter how insignificant they appear. Every penny paid in fees is a penny not compounding towards your portfolio’s growth. Over extended periods, these fees compound, substantially eroding your investment returns. Even a modest 1% annual fee can diminish your total returns by as much as 30% over a 35-year investment horizon.

Familiarising yourself with different types of fees, including fund management charges and performance-related fees, is merely the first step. To truly safeguard your investments, you must implement proactive strategies. Opt for low-cost index funds or ETFs which typically carry lower fees. Regularly scrutinise your investment statements to identify and eliminate hidden charges. Additionally, don’t hesitate to negotiate for better rates whenever possible. Taking these proactive measures today can significantly protect and potentially amplify your nest egg for the future.