“A lot of people died fighting tyranny. The least I can do is vote against it.” — Carl Icahn.

Shareholder activism has arrived on our shores. Sunningdale Tech Limited has become the latest battleground between insiders looking to take the company private and activists looking to get a better deal for themselves and other minorities.

Are the insiders at Sunningdale bullying minority investors? Or can this be a case of David rising against Goliath? If you are a shareholder of Sunningdale, what can you reasonably expect next? For the rest of us retail investors, besides an entertaining dose of reality soap, what lessons can we draw?

What is going on at Sunningdale Tech?

Sunningdale Tech Ltd is a precision plastic engineering company with manufacturing plants in eight countries globally. The company has four main business segments: Automotive, Consumer/IT, Healthcare, and Mould Fabrication.

While the company enjoys steady cash flow generation and has weathered the COVID-19 pandemic, its share price has nonetheless underperformed market expectations. Possible reasons for the stock’s underperformance are the lack of awareness about the company’s engineering capabilities, concerns over the cyclical nature of its business, and lower customer demand arising from ongoing U.S.-China trade tensions.

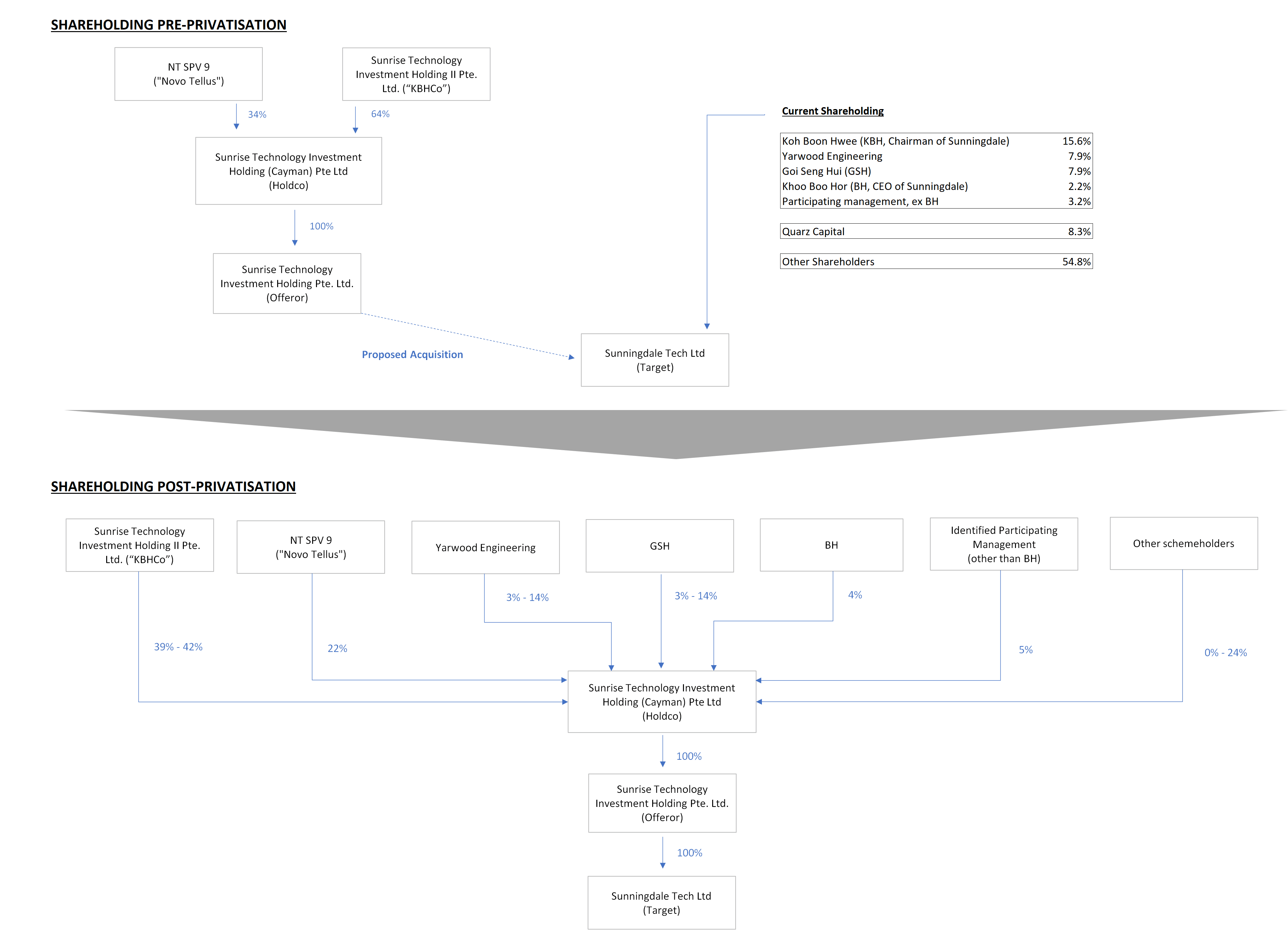

On 9 November 2020, possibly tired of the company’s persistent undervaluation, a consortium proposed a privatisation of Sunningdale at S$1.55 per share. The consortium is led by Sunningdale’s chairman, renowned corporate executive Koh Boon Hwee (KBH), and private equity firm Novo Tellus, co-founded by AEM Holding’s executive chairman Loke Wai San.

Under the terms of the transaction, KBH will roll over his existing 15.6% stake in Sunningdale into the holding company (Holdco) of the acquiring company. KBH’s rollover stake in the Holdco is approximately 27%. As KBH will altogether own 39-42% in the Holdco post-transaction, he will likely be injecting new money as part of the transaction.

In contrast, for all other Sunningdale shareholders besides KBH, while the same conversion rate to private Holdco shares for every Sunningdale share will apply, the total number of shares held by all other Sunningdale shareholders that is eligible for conversion will be capped at no more than 30% in the private Holdco. The remaining Sunningdale shares ineligible for conversion to private Holdco shares will simply be bought out at S$1.55 per share.

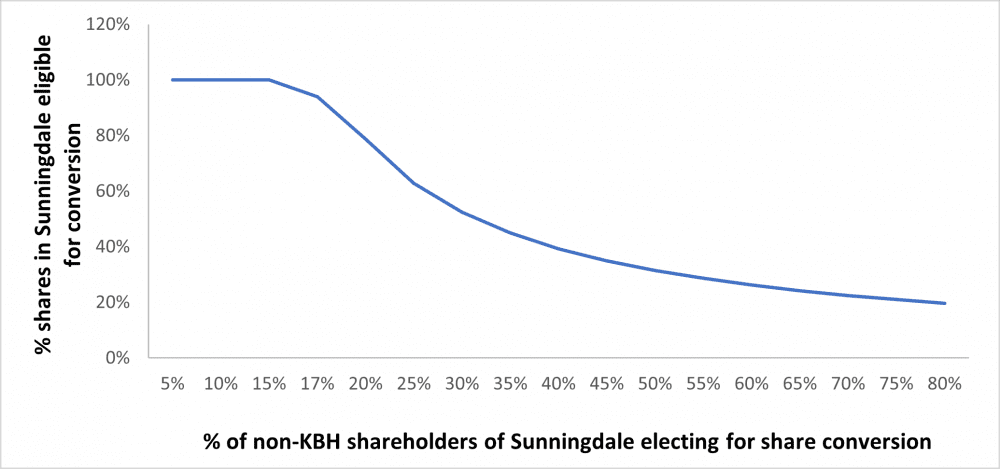

To explain this complicated mechanism via a simplified illustration, let’s assume we own 100 shares in Sunningdale. Based on the initial conversion ratio of 1550, we would be entitled to own 155,000 (= 100 x 1550) shares in the private Holdco. However, if we were to assume 80% of non-KBH shareholders in Sunningdale also decide to convert their shares, then the 30% cap in Holdco will apply. In this case, a pro-rata conversion will result in approximately in 20% of our Sunningdale shares being eligible for conversion, i.e. 20 shares. The remaining 80 shares will each receive $1.55 therefore receiving a pay-out of S$124.

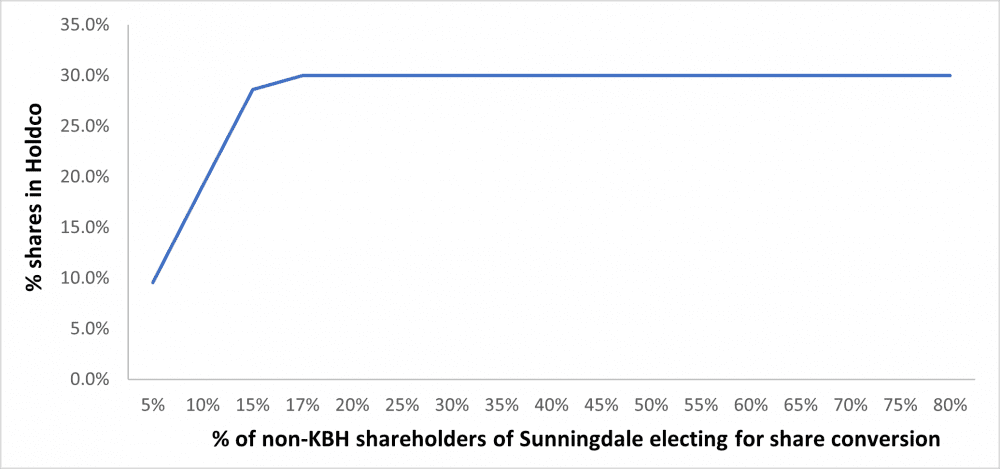

In essence, the greater the number of non-KBH shareholders in Sunningdale who elect to convert their shares to private Holdco shares, the lower the percentage of Sunningdale shares one can convert to private Holdco shares (Exhibit 2).

Another way of illustrating this mechanism is that based on the 1550 conversion ratio, once more than 17% of non-KBH shareholders in Sunningdale decide to convert to Holdco shares, the cap on 30% ownership in the private Holdco will kick in.

If the above is too complex to digest, then the main takeaways are these:

- All non-KBH shareholders in Sunningdale, which includes minority retail investors, will be subjected to a cap that restricts total ownership in the private Holdco to be no more than 30% in aggregate. This is structured in such a manner so that interested parties in the transaction, i.e. KBH and Novo Tellus, will retain control over the private Holdco.

- KBH, who owns 15.6% in Sunningdale, will curiously not be subjected to the same 30% cap and will be able to fully rollover his shares into the Holdco at the share conversion ratio. This preserves the upside for KBH, while non-KBH shareholders of Sunningdale will have to realise their shares that are not eligible for conversion at $1.55; i.e. any upside is effectively capped. KBH will argue that in doing so, he is also exposing himself to further downside risk; but given Sunningdale’s improving fundamentals this is an unlikely possibility.

- It is interesting to note that if less than 17% of non-KBH Sunningdale shareholders elect for conversion, then their post-privatisation ownership share in the Holdco will actually be higher than their pre-privatisation ownership share in Sunningdale. The point here is that especially for minority retail investors, it is unlikely that they will want to hold a highly illiquid stake in a privatised company, especially if it is a relatively small stake and subject to little, if any, investor protection. Paradoxically, not electing to convert the shares in Sunningdale will inadvertently enhance the stakes of other insiders such as Yarwood and GSH Corporation.

Why Quarz Capital is unhappy with the proposed offer

Quarz Capital Management is an activist investor. Similar to the typical modus operandi of activist investors like Carl Icahn and Daniel Loeb in the United States, Quarz has taken a very public position to air their dissatisfaction with the proposed privatisation offer.

The main reasons for Quarz’s unhappiness are the following:

- The offer of S$1.55 a share significantly undervalues Sunningdale and therefore is not a fair price to pay minority investors. Quarz contends that similar takeover transactions in the past valued the companies at or significantly above book value, while the proposed offer values Sunningdale at 23% below its book value.

- The takeover prevents minority investors from enjoying the recently improving financial performance at Sunningdale. Quarz highlights that Sunningdale’s profitability looks to be improving after a series of lacklustre performance in prior periods. Therefore, the takeover prevents minority investors from enjoying the upside from the business turnaround. Perhaps the sharpest criticism from Quarz is that the takeover offer does not recognise and reward the minority investors who have stuck with Sunningdale through a period of heavy capital expenditure. Between 2015 and 2019, the company invested more than S$150 million to build up its production capabilities. Especially if those capabilities were to now start yielding positive operating leverage for Sunningdale, then the privatisation denies minority investors the opportunity to share in the turnaround.

- The proposed structure clearly privatises any benefit into the hands of a select few private individuals and Private Equity firm Novo Tellus. As earlier covered, the structure of the deal caps the total ownership of minority investors in Sunningdale in the new private Holdco, therefore squeezing minority investors to accept the S$1.55 per share offer.

Quarz additionally raises two striking points:

- Why does Novo Tellus choose not to buy a stake via the open market, and instead enters the private Holdco via the backdoor? This is a good question and strikes at the heart of why privatisation might not be the best or only route for Sunningdale. There are other mechanisms for a listed company, such as a rights offering or private placement, to bring in new capital if Sunningdale requires additional funds for investment. Given that Sunningdale had done a private placement to raise S$25 millon (from Yarwood and GSH) to finance potential organic and inorganic opportunities in 2014, why is it that the same cannot be done again?

- Loke Wai San, who is the co-founder of Novo Tellus, was an independent director of Sunningdale up until 12 November 2020. Given that the initial offer was on the 9 November 2020, should he not have been owing fiduciary duties to minority shareholders of Sunningdale to ensure that their rights are protected?

What is the price for Sunningdale that minority shareholders should accept?

On 19 January 2021, after initial pushback from Quarz, the proposed offer was raised by 6.5% from S$1.55 to S$1.65 per share. Besides the egregious structuring of the transaction that limits minority participation in the private Holdco, is the offer price for minorities to exit Sunningdale fair?

The consortium of KBH and Novo Tellus cites how much of a premium their offer is when compared against the share price Sunningdale was trading at prior to the announcement of a possible transaction on 9 September 2020. In contrast, Quarz compares the offer price against the book value of the firm and states that this values Sunningdale significantly lower than its liquidation value.

Both parties will necessarily be self-interested to choose a benchmark that presents their case in a favourable light. As a retail investor, trying to identify the fair value of Sunningdale via the employment of traditional valuation techniques such as discounted cash flows, trading multiples of peers, or precedent transactions is likely to be a very daunting prospect. It is also understandable that the usual tendency is to be backward-looking and merely compare what the offer price is against what our average cost price was.

In determining a reservation price above which it makes sense to accept the offer, one could consider two other factors:

- What returns will I be able to earn if I were to stay invested in Sunningdale?

- What is my opportunity cost of money tied up in Sunningdale, i.e. what can I earn on my money if it was not invested in Sunningdale?

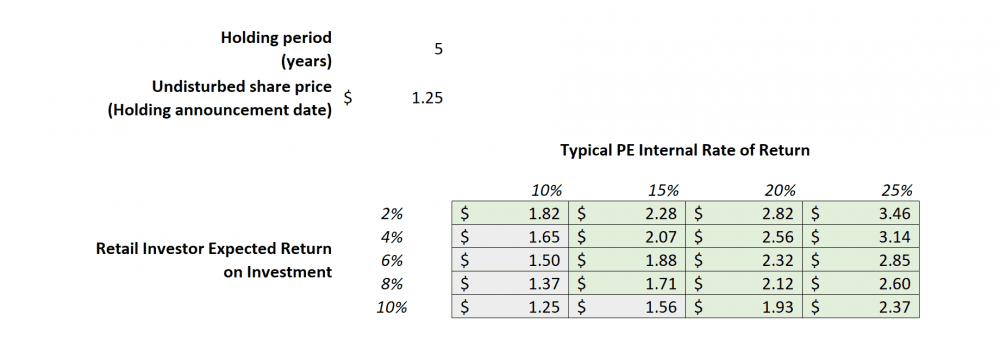

Point one is easy to determine because we can triangulate this number from what private equity investors typically expect to earn from their investment.

On an annualised basis, private equity investors would expect to earn anywhere upwards of 15%. This is typically the return hurdle at which capital providers to private equity investors would demand. Therefore, it is not unreasonable to expect that the upside from staying invested in Sunningdale will yield a return of at least 15% a year.

Novo Tellus will argue that their superior return is only possible if they were to be the controlling shareholders of the firm. However, the question minorities should ask is this: Given that KBH, Loke Wai San, and Khoo Boo Hor were all already contributing to Sunningdale in the capacity as chairman, director, and CEO respectively, how much better can they run the company when it is private?

Point two is self-explanatory and is driven largely by our own choice of investments outside of Sunningdale.

Putting this together would yield us our reservation price, below which we should not accept the offer and above which it makes sense to accept the offer. As a starting point, the undisturbed share price of S$1.25 should be the basis by which we arrive at the reservation price. This is the price on 9 September 2020, when Sunningdale announced a possible offer for its shares. I have used a five-year holding period given that private equity investors typically hold their investments for anywhere between five and seven years.

If one expects Sunningdale to be able to earn a high return in the next five years, and if one is not confident of being able to earn a high return in other investments; then ownership of Sunningdale shares is more valuable.

In contrast, if one expects weak returns from Sunningdale and there are much better alternative investments, then the value of Sunningdale to us is low and it is better to tender the shares and invest the money elsewhere.

The fifth perspective

The first lesson is probably well-known, that is to always look at the shareholding of any company before investing in it. If there are a lot of insiders and if they own a large controlling stake, then be mentally prepared for actions such as this.

The second lesson is about the evolution of our equity markets in Singapore. Perhaps we are still in the early days, but shareholder activism is not as prevalent as in other developed markets such as the UK and US. With 66% of SGX-listed companies trading below book value, and the STI returning a miserable 1.9% on an annualised basis over the past ten years; there is much to be done to improve the state of corporate Singapore.

This is probably where the value of activist shareholders lies, notwithstanding the noise and irritation they will bring to our boardrooms. If they can play a constructive part in structurally improving the way companies are run in Singapore, the value that can be unlocked will benefit all shareholders, including us retail investors. Corporate Japan has embraced the rise in activist engagements in the past two years, and helpfully we might see the same.