Listed in 2010, Sunway REIT is a diversified Malaysian REIT with a focus on retail malls. It generally invests in retail and mixed-used assets in high-growth cities and townships. As of June 2019, it owned 17 assets with a total asset value around RM8.1 billion. Its properties are spread across Peninsular Malaysia – mainly in the Klang Valley, Penang, and Ipoh areas.

I took a closer look at Sunway REIT when its share price was near its one-year low at around RM1.54 last month. During that time, Sunway REIT’s dividend yield was about 6.2%, which is higher than the 5.45% dividend yield the Employees Provident Fund posted in 2019.

Here are 15 things to know about Sunway REIT before you invest:

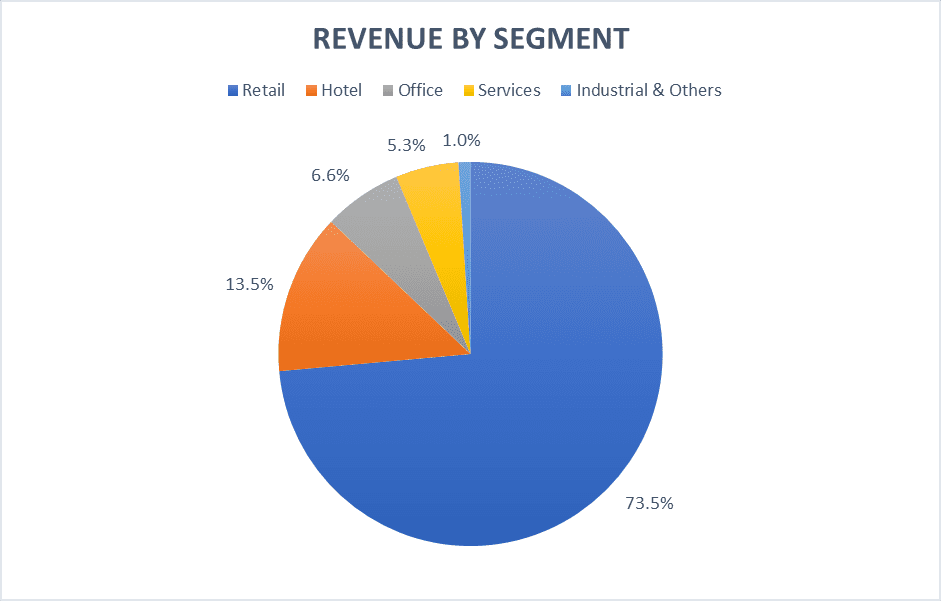

1. Sunway REIT’s retail segment was its major revenue contributor in 2019, followed by the hotel and office segments. Sunway REIT is a retail-focused REIT as the top three properties by revenue contribution in 2019 are shopping malls. In fact, the Egyptian-themed Sunway Pyramid Shopping Mall is Sunway REIT’s crown jewel which contributed to more than half of the REIT’s revenue at 56.5%. The mall is located in Sunway City that attracts both locals and tourists. It registered a property yield of 6.8% and an occupancy rate of 98.2% in 2019, which are commendable figures.

Source: Sunway REIT 2019 annual report

2. Sunway REIT owns six hotel properties across Klang Valley and Penang. Although Sunway Resort Hotel & Spa is Sunway REIT’s flagship hotel, the Sunway Clio Property — which was acquired only in February 2018 – brought in more revenue for the REIT. The property yield of Sunway Clio Property, at 6.0% is the highest among Sunway REIT’s six hotels. All the hotel master leases are a decade long and can be renewed for another 10 years.

3. Sunway REIT’s six offices, all located in Klang Valley, contributed to only about 6.6% of the REIT’s revenue in 2019. One of its office towers, Sunway Tower, has an occupancy rate of only about 20% since 2016 despite being located near the city centre and close to train connections. Sunway REIT wants to redevelop a part of Sunway Tower into a co-working space instead of disposing it.

Since this segment is a small contributor of the REIT’s revenue, the impact of the office supply glut in Klang Valley on the REIT is mild. However, this downside can be mitigated by the organic growth of the REIT’s retail and services segments, and its industrial property.

4. Sunway REIT’s services segment consists mainly of two properties, namely Sunway Medical Centre and Sunway university & college campus. Together with these two properties, the industrial property in the ‘industrial & others segment’ have longer-term triple net master leases. The tenants are responsible for all of the REIT’s property expenses including taxes, building insurance, and maintenance fees on top of rent.

Rental rates can be increased steadily over the years as stated in the leases. These properties with their master leases provide dividend-focused investors with a predictable income stream over the long term.

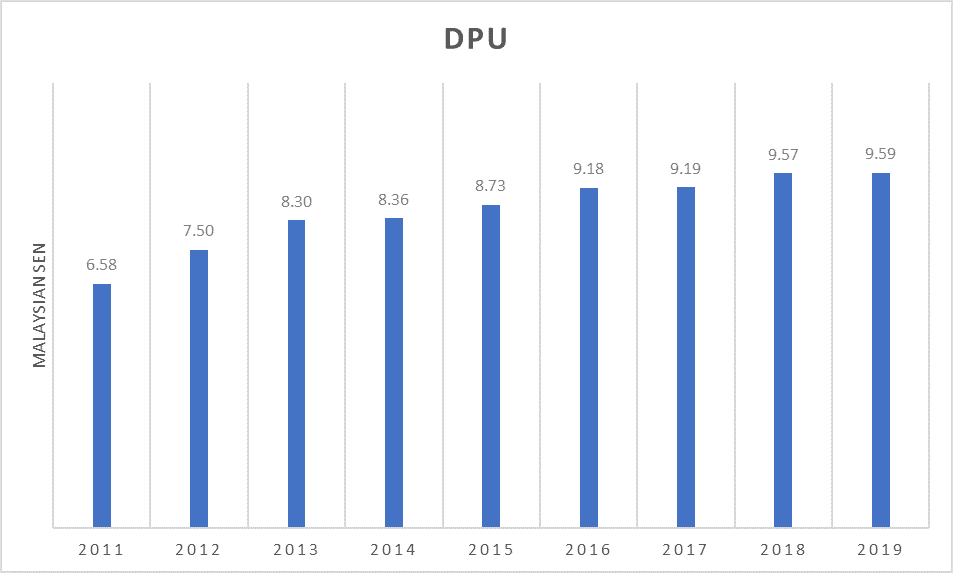

5. When it comes to dividends, Distribution per unit (DPU) was decent at a compound annual growth rate (CAGR) of 4.8% over the past nine years. The DPU growth was due to positive rental reversions over the years. Average annual rental reversions [U7] stands at 9.9%. However, the average rental reversion in the recent four years between 2016 and 2019 was only 3.2%. DPU growth was flatter in 2014, 2017, and 2019 as Sunway Putra Mall, Sunway Pyramid Hotel, and Sunway Resort Hotel & Spa were closed for refurbishment in those years.

Source: Sunway REIT annual reports

6. Sunway REIT will spend RM500 million to expand and renovate Sunway Carnival Shopping Mall. It is the REIT’s maiden greenfield development. The expansion will boost the net lettable area of the mall from 500,000 square feet to 830,000 square feet. Construction works began in 2018 and are scheduled to be completed by 2022.

This mall is doing surprisingly well in mainland Penang; in 2019, its occupancy rate and property yield stood at 97.4% and 7.4% respectively. Sunway Carnival Shopping Mall’s property yield was actually the highest among the all of the REIT’s properties in 2019.

7. The REIT has acquired nine properties since it was publicly listed. The sponsor, Sunway Berhad owns a number of properties that could be injected into the REIT including the Pinnacle Sunway office tower and Monash University Sunway Campus. These two properties are located in Sunway City.

The REIT has the right of first refusal for Pinnacle Sunway office tower. The acquisition of Monash University Sunway Campus is in line with the REIT’s vision to be a diversified REIT with at least 25% of total asset value derived from its services and industrial properties.

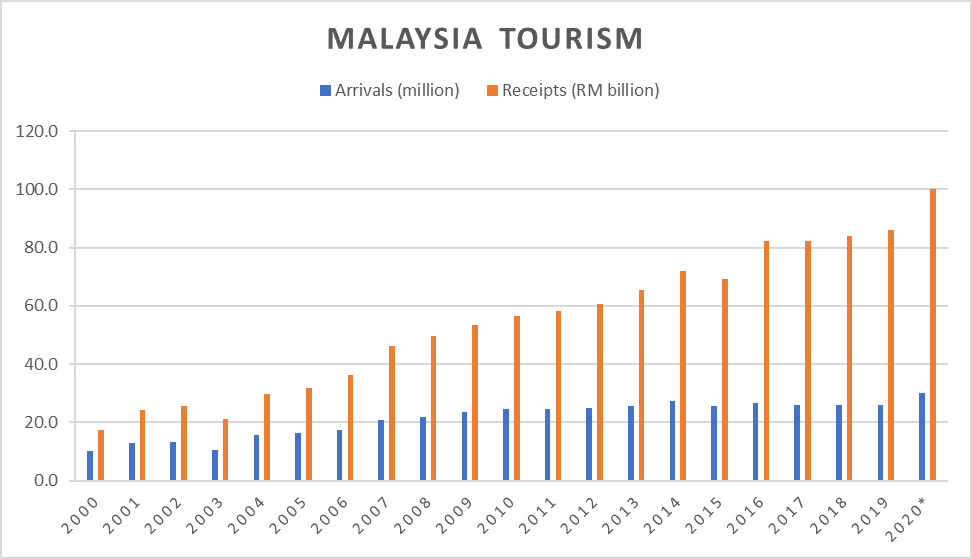

8. According to the Malaysia Tourism Promotion Board, tourist arrivals and receipts grew at a CAGR of 5.1% and 8.8% respectively between 2000 and 2019. The findings also show that tourists who visit Malaysia spend the most on shopping, followed by accommodation and F&B. Sunway REIT will stand to benefit from the organic growth of domestic and international tourism in Malaysia, particularly for its retail and hotel segments.

*Targeted. Source: Malaysia Tourism Promotional Board

9. The assets of Sunway REIT are predominantly located in Sunway City within Klang Valley. Sunway City is an integrated development that receives about 40 million visitors each year. It is about a half an hour’s drive from the Kuala Lumpur city centre. The seven properties in Sunway City accounted for about 75.1% of the REIT’s revenue in 2019.

Although the portfolio concentration risk is quite high, it should be alright so long Sunway City continues to attract visitors. Some initiatives taken to improve the liveability and connectivity of the city include the construction of elevated pedestrian walkways and an elevated bus rapid transit system.

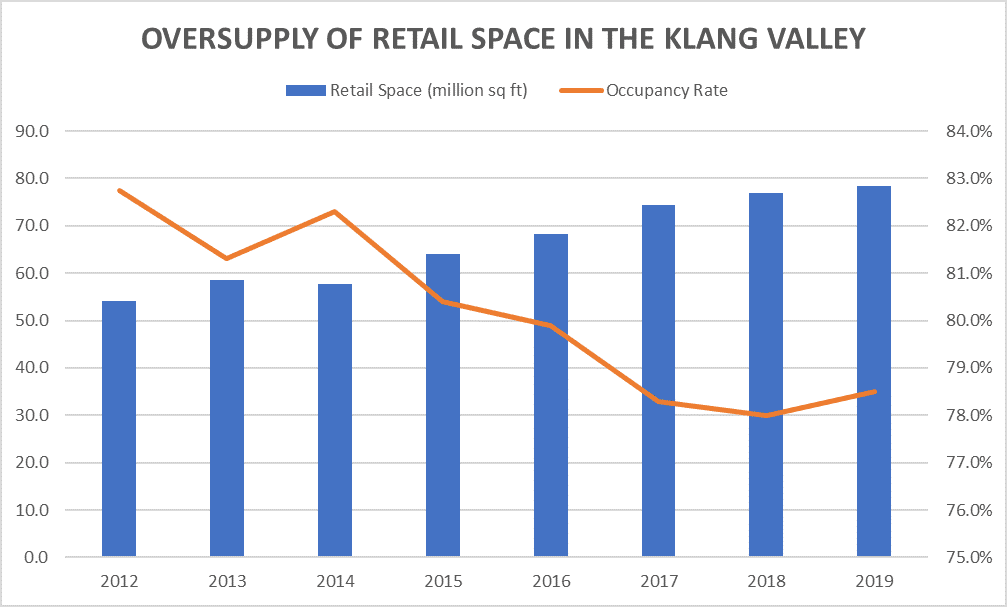

10. Sunway Pyramid Shopping Mall and Sunway Putra Mall are situated in the Klang Valley where there is an oversupply of retail space. As shown below, their occupancy rates have been dropping from 82.8% in 2012 to 78.5% in 2019 while the total amount of retail space available climbed from 54.1 million square feet to 78.4 million square feet over the same period.

Source: Pavilion annual reports

11. The supply glut issue will be exacerbated by the COVID-19 outbreak. Sunway REIT has committed to giving its retail tenants that provide non-essential services with at least 14 days’ worth of free rent. It faces short-term headwinds as it may receive lower turnover rent and car park income from fewer visitors. Sunway REITs short-term future is dim but it is poised to slowly return to normal as Malaysia eases the movement control order.

12. Shopping malls will continue to be cannibalised by e-commerce. However, Sunway REIT’s crown jewel, Sunway Pyramid remains a popular shopping mall in Klang Valley alongside Mid Valley Megamall, Pavilion Kuala Lumpur Mall, and 1 Utama Shopping Centre.

Malaysians in general still like to spend their weekends in air-conditioned malls. Malls that are better managed like Sunway Pyramid will most likely survive the retail space supply glut and COVID-19 by complementing e-commerce and improving customers’ shopping experience.

13. The occupancy rate of Sunway REIT’s hotels stood at 69.3% in 2019, which is above the average hotel occupancy rate in Kuala Lumpur, Selangor, and Penang. The industry’s occupancy rate average is at a historical low as the number of hotel rooms in Malaysia continues to rise. The hotel industry is rather cyclical and will flourish only during good times.

14. The REIT has conducted a private placement of units to institutional investors only once in 2013 since its IPO. The price of the unit placement was at a 2.9% discount from its unit price at that time. The quantum of placement was about 8.0% of its existing number of units. Sunway REIT ensures the minimal dilution on shares of existing unitholders.

15. In 2019, the gearing ratio of Sunway REIT stood at 37.9%. If its perpetual notes are added as borrowings in the calculation, its gearing will increase to 42.1%. This is quite close to the stipulated guideline of 50% and leaves very little room for the REIT to raise money via debt.

The REIT’s retail, services, and industrial properties fare better than the remaining two segments in terms of both average property yield and occupancy rate. Its 2020 performance will be affected as locals shun crowded shopping malls and tourists postpone their vacation plans. But if we take a long-term view of this company, Sunway REIT could still be a decent dividend stock.

Investing in Sunway REIT? Read more articles on Sunway REIT including our analysis of its past years’ performances and the AGMs we personally attended. Click to read more below:

7 things we learned from the 2017 Sunway REIT AGM

14 things to know about Sunway REIT (updated 2017)

13 things to know about Sunway REIT (updated 2018)

15 things to know about Sunway REIT (updated 2019)