Temasek Holdings, an investment company wholly-owned by the government of Singapore, released its financial results for the year ended 31 March 2019 during Temasek Review 2019. Temasek Review is an annual event in which Temasek executives examine the fund’s performance over the past year and share their thoughts on a host of topics from portfolio allocation to market outlook.

After attending the Temasek Review 2019 media conference, I came away with a much better understanding of Temasek’s portfolio, its investment principles and its outlook for global markets going forward. While Temasek is not a listed company that investors like us can buy into, the company’s future developments are definitely worth following. After all, it owns a significant stake in some of Singapore’s largest companies, and its success is closely intertwined with that of the country’s.

In light of that, here are eight things I learned from Temasek Review 2019:

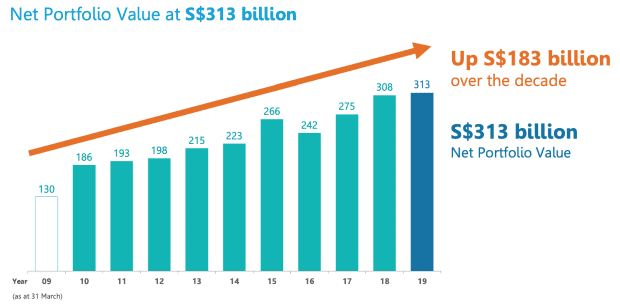

1. Temasek’s portfolio value grew by 1.6% from S$308 billion in 2018 to S$313 billion in 2019. Over the past ten years, Temasek’s portfolio has grown at a compounded annual growth rate (CAGR) of 9%, adding a total of S$183 billion in value.

Temasek’s total shareholder return for the year was 1.49%. While this was below the MSCI World Index’s return of 8%, it outperformed the MSCI All Asia ex-Japan index’s negative 2% return, and MSCI Singapore Index’s negative 3% return. This reflects Temasek’s increased exposure to the Asian markets, as we will explore in greater detail in the third point.

2. Temasek maintains a healthy balance sheet, with total debt of S$15.1 billion against S$44.2 billion in cash and short-term investments. Its debt represents only 4.8% of its portfolio value, but more importantly, the firm’s recurring income sufficiently covers its interest payments. Its dividends alone are enough to cover its interest expenses 22 times over, and recurring income from divestments, dividends, interest income and investment income are 96 times of its interest expenses.

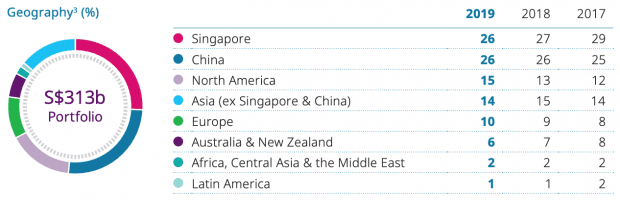

3. Asia accounts for the bulk of Temasek’s portfolio- making up two-thirds of total portfolio value. It has most exposure to companies based in Singapore and China, with the two countries each accounting for 26% of total portfolio value. According to Temasek COO Chia Song Hwee, Temasek has increased its allocation to China over the past few years, in part due to attractive investment opportunities in companies that have access to the large and growing Chinese market. As seen in the table below, Temasek also increased its exposure to the North American and European markets to 25% this year. While Temasek CEO Dilhan Pillay acknowledged that they are ‘relatively underweight in Europe and US’ holdings, exposure to Asia is expected to remain significant going forward since Asia continues to drive global growth.

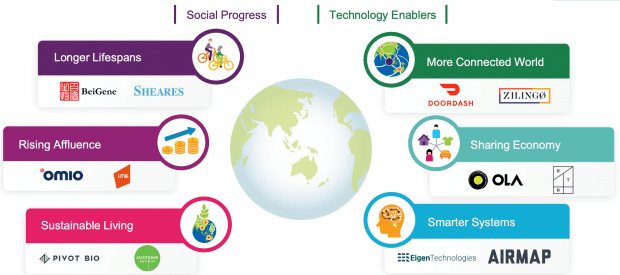

4. Temasek has identified six structural trends that will underpin its future investments. The six trends are: longer lifespans, rising affluence, sustainable living, more connected world, sharing economy, and smarter systems. In his prepared remarks, John Vaske, head of Temasek’s Americas segment, divided the six trends into two main categories — social progress and technology enablers.

Vaske continued by identifying a number of investments that capitalise on these trends. For instance, Temasek’s investment in Pivot Bio, an American biotech developing an alternative to environmentally harmful fertilisers, capitalises on the ‘sustainable living’ theme.

5. Global growth remains weak, and Temasek remains cautious in the face of elevated recession risk. In her prepared remarks, Senior Managing Director Png Chin Yee shared that Temasek expects global growth to remain weak going forward due to trade tensions and disruptive technologies. As a result, global interest rates will likely remain low as policymakers attempt to spur investment and economic growth. For instance, the U.S. Federal Reserve recently signaled its willingness to cut rates if economic uncertainties persist. While low interest rates generally stimulate economic growth, global interest rates are already low as they are, limiting the effectiveness of future rate cuts. This elevates recession risk in the medium term, giving Temasek reason for caution. However, Png noted that the firm remains ‘open and alert to investment opportunities in strong, resilient companies’.

6. Temasek is relatively insulated from the negative impacts of U.S.-China trade tensions despite its exposure to both markets. Most of Temasek’s current investments in the U.S. and China are centered on domestic themes. For instance, its largest Chinese investments, which include the likes of Alibaba Group Holdings, Ping An Insurance and China Construction Bank, are in the consumer and financial industries. These industries are not as reliant on trade and capitalise on structural trends such as increasing domestic consumer spending. Such structural forces will continue to drive growth even in the face of increased uncertainty. Despite this, the firm is actively evaluating the impact of trade tensions on its existing holdings.

7. The weight of private companies in Temasek’s portfolio has increased substantially over the past ten years. In 2009, private companies and unlisted assets accounted for 28% of Temasek’s portfolio. By 2019, that figure has increased to 42%. The company is largely agnostic to the listing status of potential investments, given that it allocates funds in accordance to its investment principles and the six structural trends it’s identified. The increase in weight was driven by capital market trends and Temasek’s increased allocation to early-stage companies. In general, companies are staying private for longer periods of time due to factors such as market volatility and stringent disclosure requirements. Additionally, Temasek made some investments in early-stage companies to better understand a number of nascent yet potentially disruptive trends. Among other advantages, an understanding of these trends provides clarity on their possible impacts on current portfolio holdings.

8. While Temasek’s investment in Bayer AG is underperforming, management is confident about its future prospects. Shares in pharmaceutical giant Bayer has been battered over the past year amid allegations that its herbicide Roundup causes cancer. Having purchased a 3.6% stake in April 2018 at a price of €96.77 per share, Temasek is now sitting on a paper loss of about a third of the initial investment. Head of Americas John Vaske replied saying that their investment in Bayer was underwritten by a long-term thesis that still remains intact today. It plays to two of the six structural trends that Temasek has identified, namely sustainable living and longer lifespans. In addition, Bayer has largely met the team’s initial assumptions and projections, which gives them confidence. Vaske added that the decline in Bayer’s share prices is a function of the uncertainty surrounding the litigation case. As an investor focused on the long term without immediate capital needs, Temasek is able to look past the uncertainty surrounding the litigation issue and focus on the company’s long-term potential.

Read more: 5 reasons why you shouldn’t buy a stock just because a big-name investor owns it