Temasek Holdings is a private investment company wholly owned by the Singapore government. As of 31 March 2020, Temasek manages a net portfolio of S$306 billion. Some notable holdings in the portfolio include Singapore blue chips like DBS Group, Singapore Airlines, and CapitaLand; and foreign stocks like Visa, Alibaba, and Meituan Dianping.

Temasek Review is an annual event in which Temasek executives examine the fund’s performance over the past year and share their thoughts on a host of topics from portfolio allocation to market outlook. We first attended Temasek Review in 2019, and were also invited to cover the event this year as we look at how COVID-19 has impacted Temasek and its portfolio of companies.

Here are 10 things I learned from Temasek Review 2020:

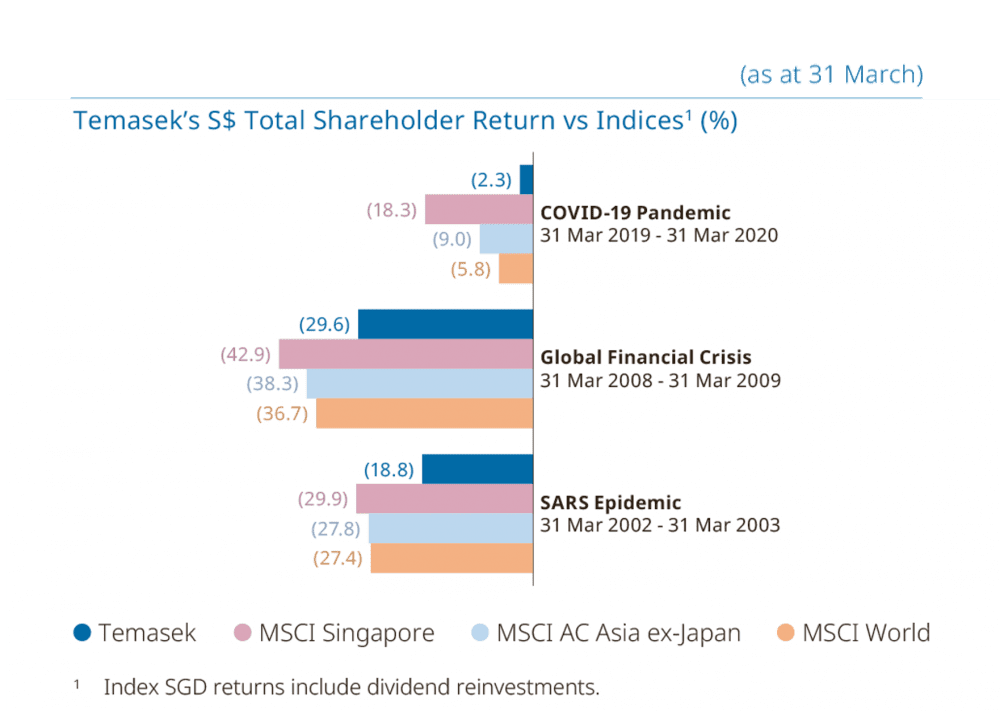

1. Temasek’s total shareholder return was -2.3% and its net portfolio value fell to S$306 billion in FY2020 mainly due to the impact of COVID-19. In comparison with the indices and past crises, Temasek’s portfolio was remarkably resilient despite the widespread losses caused by the pandemic.

This is coupled with the fact that Temasek’s financial year ended on 31 March 2020 when many stock markets were trading near their bottoms. Deputy Head of Singapore Projects, Yeoh Keat Chuan, explained that Temasek’s limited exposure to the travel, hospitality, and entertainment sectors helped to weather the impact caused by COVID-19.

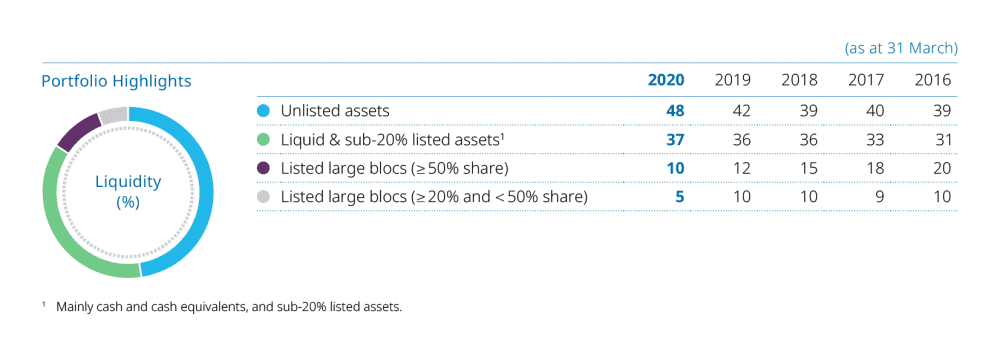

2. Private companies now comprise 48% of Temasek’s portfolio. However, Deputy CFO Png Chin Yee explained that this was partly due to the bottom valuations of Temasek’s publicly listed holdings in March and that the subsequent run-up in prices since should see them comprise a larger share of the portfolio.

At the same time, the proportion of private assets in the portfolio has steadily risen over the years — in 2010, the proportion was just 23%. Yeoh explained that this was in line with the structural trends Temasek invests in where there are currently more opportunities in private equity.

Head of China, Wu Yibing, shared that COVID-19 has also accelerated some of these structural trends such as digitisation and the sharing economy. For example, the use of food delivery apps like Meituan Dianping increased during the lockdown in China, and the habit of ordering food online among younger consumers is likely to grow post pandemic.

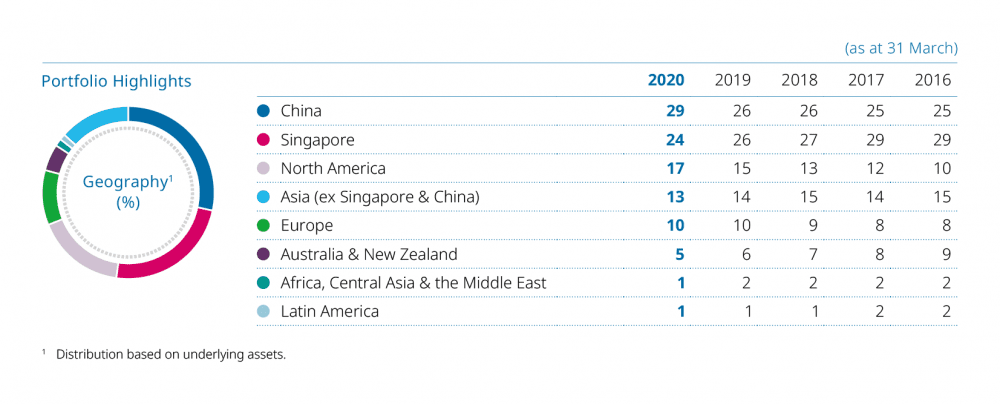

3. China now accounts for the largest geographical market in Temasek’s portfolio at 29%, followed by Singapore (24%) and North America (17%). Png shared that as Temasek’s portfolio evolves, Singapore will naturally account for a smaller share as the Singapore economy is small compared to other markets, especially the U.S. and China.

She added that this shift also reflects the overseas expansion of Temasek’s portfolio companies that are domiciled in Singapore. At the same time, Temasek will continue to invest in Singapore and support the local ecosystem here.

4. Although the current geopolitical tensions between the U.S. and China could see Chinese companies being delisted from U.S. exchanges, Temasek believes that fundamentally strong companies will grow in value over time regardless of where they list. Wu reiterated that Temasek continues to look at resilient sectors which benefit from strong domestic consumption and long-term structural trends.

Pillay said that the relationship between the U.S. and China is critical as the these are the two biggest economies in the world and what happens between them has an impact on economies elsewhere. He added that the U.S. and China have been the top two destinations for Temasek’s investments in the last 5-6 years and will continue to be the case moving forward based on the structural trends that Temasek has identified.

5. Temasek is an early investor in Ant Group – the operator of Alipay, China’s largest mobile payment platform — which is being lined up for a potential US$200 billion IPO. When asked whether Temasek would sell any of its stake at the IPO, Png declined to give any details as she felt it was inappropriate to comment as Ant is still preparing for its listing. She shared that Ant has evolved China’s financial services industry by providing inclusive finance to large parts of the Chinese population through technology and data, and that there’s a lot of potential for Ant going forward.

6. Temasek was actively adding stakes to companies they liked during the second quarter of the year when market valuations were beaten down. Png revealed that Temasek increased their exposure in the payment space in Visa, Mastercard, and PayPal, and was also active in India and China as well. In May, Temasek added a US$3.5 billion stake in asset management giant, BlackRock.

7. As part of its ESG initiatives, Temasek achieved carbon neutrality in 2020 and aims to deliver net zero carbon emissions for its portfolio by 2050. Temasek also views that sustainability efforts can also deliver new investment areas. For example, Yeoh highlighted that 46% of the world’s arable land is already used for crops to feed livestock — which is unsustainable as the world population and demand for protein continues to grow. Due to this trend, Temasek believes that there is an investment opportunity in plant-based proteins and has increased its stakes in Impossible Foods, Memphis Meats, Perfect Day, and Califia Farms.

8. Pillay believes that Singapore Airlines is an exceptional company and will find a way to operate ‘as they did before’ in a post-pandemic world. The airline raised S$8.8 billion in June during a rights issue backed by Temasek as the aviation industry continues to struggle with the impact of COVID-19. Half of the capital raised has already been used and Pillay gave no details whether Temasek would lead another round of financing for the airline down the line.

9. Temasek implemented a company-wide wage freeze due to COVID-19 and its senior management took a voluntary cut in salary and bonuses to stand in solidarity with the wider community. Along with Temasek’s philanthropic efforts, the savings were channelled towards COVID-19 initiatives in Singapore and around the world. They include providing 11 million masks for Singapore residents and donating over half a million test kits overseas.

10. Up to 50% of Temasek’s dividends and expected long-term returns can be used for the Singapore government’ spending under the NII/NIR framework. Along with MAS and GIC, Temasek contributed around 20% of the government’s Budget in 2020. Due to COVID-19, the Singapore government announced four Budgets this year totalling S$193 billion to help the country deal with the effects of the pandemic. However, Png clarified that the NIR framework provides a guideline for what the government can include in its budget and is not reliant on cash flows received from Temasek.

The fifth perspective

Temasek Holdings is one the most widely-followed investment funds among investors in Singapore. Its long-term track record speaks for itself — Temasek’s net portfolio has grown from S$354 million in 1974 to S$306 billion today, delivering an annualised return of 14% over 46 years.

While it is understandable that retail investors may like to copy Temasek’s investment decisions because of its overall success so far, it’s important to remember that retail investors should never blindly follow a big-name investor as they each have vastly different investment goals and time horizons.

One thing that jumps out off the page at me, as the most interesting trend, is Temasek’s move away from listed to unlisted assets. These now account for 48% of their portfolio. Over the past 5 to 6 years it’s become less common for retail investors to have access to investment in some of the most stellar growth stories, whereas private equity has increasingly taken a big share of the action. We can find some sectors (e.g. cybersecurity, innovative battery tech and AI) where about 90% of the top players are not listed, and are very often owned by private equity players. This has even garnered political attention from some surprising people, e.g. Elizabeth Warren (the prominent US Democrat) has said that this is making the investment market less democratic and restricting access to the best opportunities to a small group of billionaire investors (people like Peter Thiel, the Koch Brothers, KKR and so on). For the smaller investor, it really is bad news.

Agree with you, Jonathan. The big boys have always had access to investments not available to the man on the street. Another point I could highlight is that Temasek is also investing at earlier stages in companies in recent years, which is why we see more unlisted assets in its portfolio.

One interesting thing I learned from Temasek Review 2020 can be found in its webpage:

https://www.temasekreview.com.sg/investor/total-shareholder-return.html

If you look at the last 20 years, Total Shareholder Return is less than Risk-Adjusted Cost of Capital. In finance theory, if Total Shareholder Return is less than Risk-Adjusted Cost of Capital, it means that the company is destroying rather than creating shareholder wealth. So, by Temasek’s own calculations, it has been destroying wealth to its shareholders (ultimately the citizens of Singapore) over the past 20 years.

Would you agree with this interpretation or am I missing something here?

Hi Alfred, Yes, a firm’s overall returns should outperform its cost of capital over the long term. In the case of Temasek, it’d be better to measure this using its TSR based on equity which is a more stable gauge of performance. We can see that Temasek’s TSR has markedly outperformed its RACC since its inception, but you are right to highlight that this spread has narrowed in the last 20 years and more recently. This is partly due to the law of large numbers — it is much harder to earn a higher return as your fund increases in size. Temasek is now managing a S$306 billion fund, but yes, Temasek needs to continue outperforming its RACC moving forward in order to create wealth.

Thanks Adam for your response. A few comments.

1. TSR based on equity: This is book value and would be useful as a performance measure only if it is a good proxy for market value. But very often it is not. For companies like Google, Microsoft, Facebook, etc. book value of shareholders equity has no resemblance to market value. Stock prices are based on expectations of future performance whereas book value of shareholders equity is based on historical performance. Also, book value does not capture value of intangible assets which make up a large part of the value of these tech and other companies. For start-ups and unlisted companies, very often shareholder equity is negative but their valuations may be high based on series funding valuations. Best always to use market value performance measures but recognizing as you indicated the volatility of market prices. Can get around this by computing rolling averages of returns based on market values but not just 10 years or 20 years but maybe yearly or even monthly (can put in an appendix so as not to clutter up the main report).

2. Why is it harder to earn a higher return as your fund size increases? I thought there would be economies of scale. And cannot be because of shortage of investment opportunities. Temasek fund size may be S$306 billion but S&P market cap is US$30.5 trillion or S$41.6 trillion. So Temasek portfolio is only 0.7% of the S&P market cap. And there are other markets around the world. So no shortage of investment opportunities.

3. Finally, I find it a bit curious that Temasek’s performance gets better and better when you go back further in time. If you look at TSR by market value for 20 years and 30 years, TSR for 20 years is 6% and TSR for 30 years is 11%. Which means the TSR between 20 and 30 years must be much higher than 11% to pull up the 30 year average to 11% from 6% of 20 years. Why were there such high returns in the earlier years? In the earlier years, Temasek was run by people seconded from the civil service. In the last 20 years, Temasek has hired a lot of high powered investment bankers, fund managers, business advisers, etc. So civil servants did a better job than financial experts? Or were global returns in those earlier years much higher than today? I haven’t researched this so cannot comment. One hypothesis for the much better returns as we go backwards in time could be that earlier asset injections into Temasek were at book values since the GLCs were not listed (so could be injected at much lower than market value even at that time) and now we are capturing their values at market values. But I don’t have the data for this so only a guess.

Hi Alfred,

While larger funds do benefit from some cost efficiencies, it is harder for a much larger fund to grow compared to smaller one, similar to how it is harder for a mega cap to grow faster than a small cap, all things being equal.

Temasek made a US$500 million investment in Alibaba in 2016. That looks like a huge amount. But even if that investment made a 10x return, for example, it is still only ~2% of Temasek’s current net portfolio of S$306 billion.

For Temasek to at grow 10%, it needs to earn S$30.6 billion. The following year? S$33.7 billion. And the amount keeps getting larger just to grow at the same rate. How many stocks out there are able to grow at $30 billion in value in one year? Not many. So Temasek needs to make many successful investments that are large enough in order to grow.

Warren Buffett also alluded to this where he has to look for ‘elephant-sized’ acquisitions for Berkshire Hathaway. This is why Temasek’s performance was better in its early years when it was growing from a smaller base (and it also benefited from the listing of Singtel in 1993).

While the market cap of the S&P 500 and the global market is in the trillions, Temasek still needs to make the right investment decisions at a large enough scale in order to generate a positive return.

Hope this helps!

Alfred, you’re quite correct. In fact, a lot of fund managers have been performing badly. Unit trust managers appear to have been especially egregious in this respect, and charging fat fees for their poor performance. I also read somewhere that in Hong Kong the managers at the equivalent of our Singapore CPF were mainly investing in index funds and doing very little to justify their generous remuneration. Unfortunately, this seems to be a growing problem.

Thanks Jonathan for your response.

You are right and that is why there is a worldwide move towards passive investing these days.

The figures for Temasek’s returns for year ended March 31, 2020 may be distorted by the crash of worldwide markets in March of this year. But if we go back a year to Temasek’s results for year ended March 31, 2019, we see that they had TSR (by market value) for 10 years at 9% and for 20 years at 7%.

For a comparable 10-year period, the annualised returns of three indices are as follows:

STI (10 years to end-December 2018): 9.2% (in SGD)

S&P 500 (10 years to end-June 2019): 14.7% (USD so need to reduce slightly for fx loss)

MSCI World Index (10 years to end-March 2019): 10.1% (USD so need to reduce slightly for fx loss)

In other words, if I had just passively invested in these indices, i would have done just as well as Temasek if not better. But Temasek has a lot more resources and expertise than I have. Should we not expect them to do better than just passive market index investing?

But this is only for the 10 years. Going back in time, Temasek seems to have done better so not sure. Need to look at this in more detail with more data. But useful and interesting to discuss.