Despite being a latecomer to the local telco industry, StarHub has overtaken M1 and has the second largest mobile market share in Singapore. This success is mainly due to their “hubbing” strategy. I’ll cover more about StarHub’s hubbing strategy and the six things you need to know about the company in this article but before I dive into that, let’s gave a quick background on StarHub’s business model.

(You can read my previous analysis on Singtel and M1 in The Battle of the Telco series.)

The Business

StarHub is 55.97% owned by Asia Mobile Holdings whose major shareholders are Singapore Technologies Telemedia, and Otel Investments.

StarHub’s revenue generation is derived from five business segments: mobile, cable TV, broadband, fixed network, and sales of equipment.

- Mobile. The largest revenue generator for StarHub is the mobile segment which accounts for 52.3% of total revenue. This segment consists of the post and pre-paid mobile services.

- Cable TV. The cable TV segment is its second largest segment, which accounts for 16.3% of total revenue. This segment was introduced after StarHub acquired Singapore Cable Vision in 2001. Cable TV subscribers pay StarHub a monthly fee to watch exclusive TV channels on cable. StarHub had the first-mover advantage in this segment and the company is the market leader in this segment in Singapore.

- Fixed Network. Fixed network accounts 15.8% of StarHub’s total revenue and provides voice, data, and internet services for enterprise customers. In recent years, StarHub has expanded its fixed network services by offering solutions like cloud services. During StarHub’s 2015 annual general meeting, the management mentioned that this segment is the next key growth driver for the company.

- Broadband & Sales of Equipment. The broadband segment accounts 8.5% of the total revenue. This segment provides broadband services to residential homes and over three hundred hotspots around Singapore. This segment has been declining for the past four years due to increasing competition. Sales of equipment accounts 7.1% of total revenue and has been growing at 7.6% per annum for the last ten years mainly due to the growing use of smartphones.

StarHub’s “Hubbing” Strategy

With the understanding of StarHub’s individual business segments, we can move on to understand how each segment contributes to the company’s hubbing strategy.

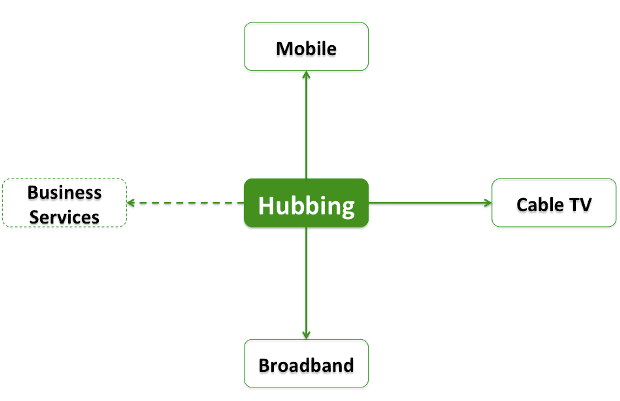

Hubbing is StarHub’s marketing strategy of bundling all its different services together in one package. Customers receive discounts and exclusive benefits when they become a “hubber”. In a nutshell, hubbing provides customers with a one-stop solution for all their mobile, internet and entertainment needs.

Hubbing gives StarHub 4 advantages:

- Reduces churn rate. Churn rate measures the percentage of customers who stop using StarHub’s services. With hubbing, the more services a customer subscribes with StarHub, the lower the churn rate as this creates a stickiness which makes a customer reluctant to switch to other providers.

- Cost efficiencies. Marketing expenses are lower because StarHub is able to promote multiple services with one main advertising offer compared to advertising each service on its own.

- Cross-selling. With hubbing, StarHub is able to easily cross-sell its other services to existing customers which lowers marketing costs.

- Increases average revenue per user. Average revenue per user naturally rises when customers subscribe to more services that hubbing provides

Hubbing currently includes mobile, cable TV, and broadband services. However, StarHub is looking to include its business enterprise services soon to further increase stickiness (especially among enterprise clients).

Let’s move on to…

6 Things You Need to Know about StarHub:

- Hubbing has work well for StarHub over the last ten years. Single and double-service households (households that only subscribe to one or two services) have been decreasing, while triple-service households (i.e. hubbers) have increased from 107,000 in 2005 to 242,000 in 2014.

- StarHub’s number of pre-paid customers fell from 1.141 million to 0.867 million in 2014. This was mainly due to Infocomm Development Authority of Singapore regulations which reduced the number of prepaid SIM cards a customer can own from ten to three. On the other hand, StarHub’s post-paid customers have been growing at 6% per annum for the last ten years.

- Despite the entry of Singtel’s MioTV in 2007, StarHub has been able to maintain its market leadership in the cable TV segment and even saw its Cable TV subscribers increase from 504,000 in 2007 to 542,000 in 2014. In 2009, Singtel won the exclusive rights to broadcast the popular Barclays Premier League from StarHub. StarHub responded by announcing a 50% discount for its sport group subscription and provided new sports channel alternatives for subscribers. StarHub’s cable TV average revenue per user per month fell slightly from $56 to $50. In 2013, the Media Development Authority Singapore (MDA) directed Singtel to offer the Barclays Premier League for cross-carriage to StarHub. This was done to prevent an expensive bidding war between the two telcos to acquire rights to the Barclays Premier League. StarHub’s cable TV average revenue per user per month has since stabilized at $52.

- StarHub’s broadband average revenue per user per month has decreased over the past ten years from $57 in 2005 to $36 in 2014 due to competition. Despite the fall, this segment contributes a relatively small 8.5% of revenue and management would rather continue to focus on hubbing to grow overall revenue.

- Due to disruptive technology that could possibly harm StarHub’s business model in the near future, the company set up the i3 division which focuses on finding new engines of growth for StarHub by investing in digital and tech startups in Asia-Pacific. This is similar to Singtel’s innov8 division.

- StarHub’s former CEO, Neil Montefiore, was also M1’s CEO from 1996 to 2009. Montefiore stepped down to join StarHub in 2010. Having a CEO that knows the inner workings of your competitor was a huge advantage StarHub enjoyed over M1. In 2013, Montefiore retired and handed over the reins to Tan Tong Hai.

The Fifth’s Perspective

This completes my analysis of StarHub’s business model. Next up, I’ll analyze five key financial metrics of the Singtel, M1, and StarHub and wrap up which telco is best positioned to handle the entry of a fourth telco in Singapore. So stay tuned!

Another point to note, Starhub has way more debt compared to its competitors

Hi Joel,

Yes, StarHub has more debt compared to the other telcos due to capital restructuring. Because the company has no growth markets overseas, one of the ways for StarHub to increase shareholder value is to return capital to shareholders and finance the business with higher amounts of debt.

StarHub is able to do so because its business operations generate strong recurring cash flows that are very predictable, so the relatively high debt is less of a worry.

Hi,

Interesting, by that logic would you say M1 can afford to take on more debt?

Hi Joel,

If M1 wants to stretch their balance sheet, they definitely have the room to do so but I doubt they will.

You have to note that M1’s business is slightly different from StarHub’s. M1 only has mobile as their core revenue driver and they’re only No. 3 in this market. In comparison, StarHub has cable TV and mobile, where they are No. 1 and 2 in the market respectively.

The amount of debt a company can take depends on the amount of cash flow it can (predicatbly) generate. StarHub’s cash flow for 2014 was $654 million while M1 comes in at less than half that at $272 million. So StarHub has the capacity to take on way more debt than M1.