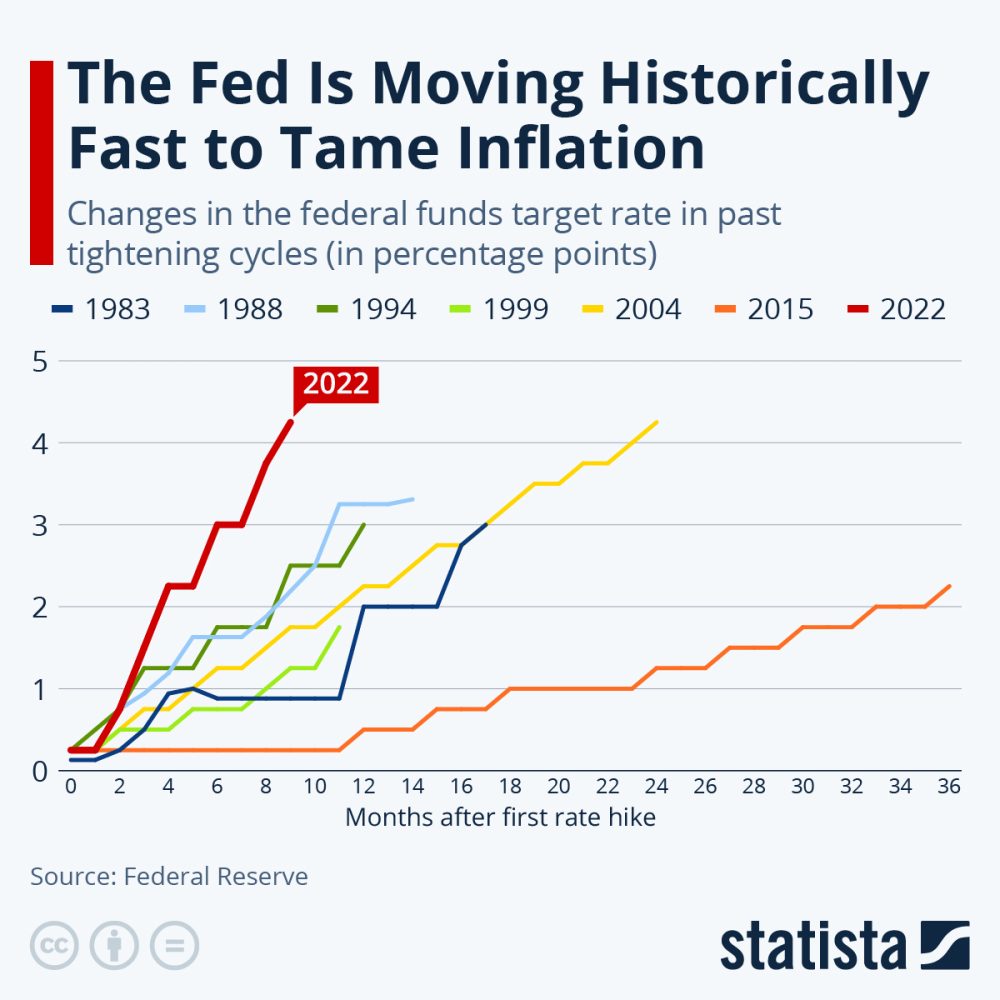

In 2022, the world saw a shift from the impact of Covid-19. Economic recovery globally led to a surge in demand, but supply chain disruptions from the pandemic still lingered, resulting in limited supply and rapid inflation. This caused the fastest rate hike in history, as the Fed took action to curb inflation.

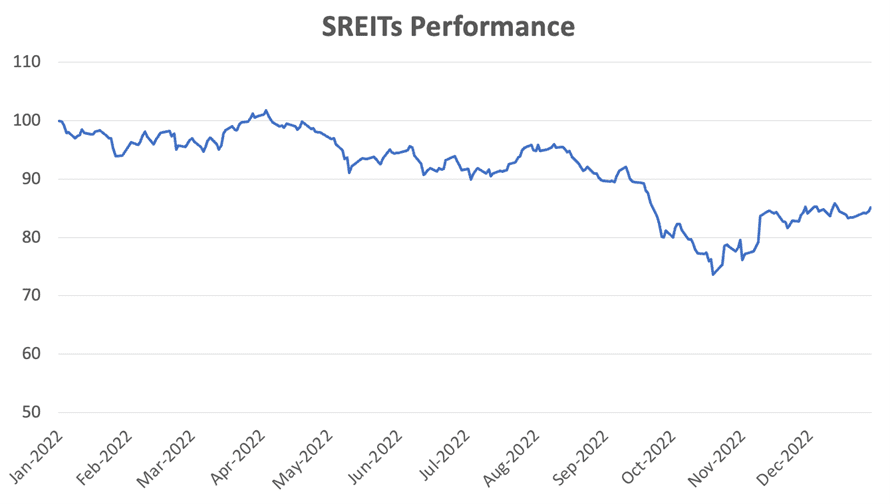

During a rising rate environment, investors tend to dispose of their REITs due to worries over increased borrowing costs that may negatively impact REIT distributions. This scenario was seen in 2015 when the Fed raised interest rates, causing a drop of over 20% in Singapore REITs. Similarly, Singapore REITs declined by 26.4% in October 2022 and the sector as a whole was down 15% for the year. This explains the absence of any REIT IPOs in Singapore in 2022, making it a difficult year for REITs.

Investors are currently seeking refuge in safe investments such as Singapore Savings Bonds and short-term Treasury Bills. Given the option between a risk-free investment yielding 3-4% and REITs yielding 4-6%, one may be hard-pressed to choose the latter. The yield spread between these two options has decreased to only 1-2%, which could be a factor in REITs underperforming compared to the STI (which saw no change) in 2022.

However, it is important to keep in mind the long-term perspective. Income investors should focus on long-term performance rather than short-term fluctuations in share prices. Month-to-month or year-to-year performance measurements may overlook the big picture. A useful benchmark to consider is a ten-year span.

Long-term performance of Singapore REITs

We first wrote about the performance of S-REITs in 2016. Once again, we will revisit their performance by taking into account the latest share prices as at Jan 2023 and distributions paid out to unitholders up to same period.

Although S-REITs have a relatively brief listing history, a few REITs have listings that align with the 2004-2007 period when the Fed Fund Rate rose to over 5%, similar to the current situation today. Although the rate hike is faster now, this historical data provides insight into REIT performance in the coming years.

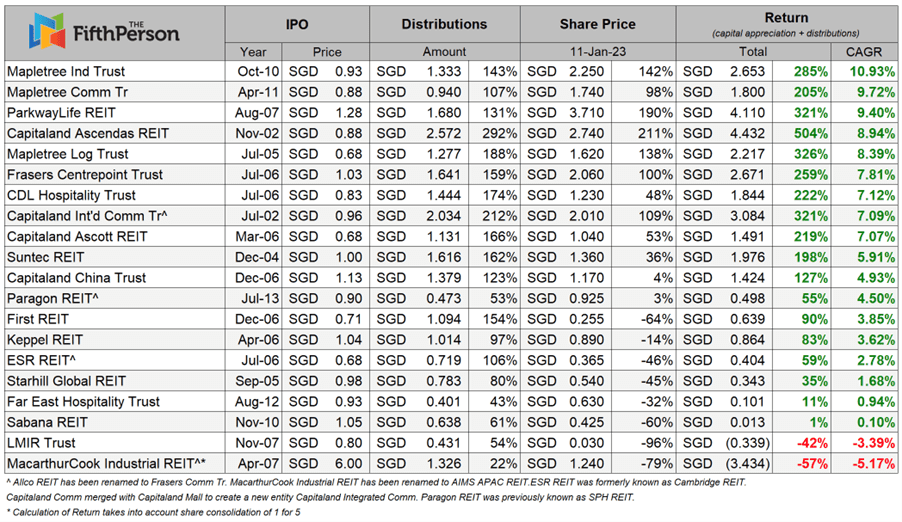

As with all investments, a 10-year listing record is necessary to accurately assess a REIT’s overall performance. I take into account adjustments such as pre-consolidated units and distributions to gain a clearer picture of their long-term performance. This year’s new entry is Paragon REIT (previously known as SPH REIT) which now has a 10-year listing history.

Once again, we will assume that John (a fictional character) invests $1,000 in each of these REITs from the day a REIT is listed. Since John is a hard-core income investor and wants to keep all his cash, he doesn’t want to come out with additional money to subscribe to rights issuances (if any) and is prepared for any share dilution. Let’s also assume that John also forgets to sell his nil-paid rights from which he can make a profit from.

For example, if John invested in Mapletree Logistics Trust (MLT) during its IPO, his initial investment of $1,000 would’ve grown to $2,138 (+138% in capital gains) as at 11 Jan 2023. On top of that, he would have collected total dividends of $1,880 (+180% in distributions).

Overall, John would’ve made a nice return in MLT as his initial investment of $1,000 would have grown to $4,260 (+326% in total return), including the dividends received over the years.

If John invested $10,000, then his investment would’ve grown to $42,600. Similarly, $100,000 would have grown into $426,000. Basically, the more money he invests, the more he makes. And the longer he holds, the more dividends he will receive. All in all, his annualised return from MLT alone is 8.39% from Jul 2005 to Jan 2023. After investing for more than ten years, here are the top 10 best-performing REITs for John.

(Note: We’ve excluded brokerage costs, currency exchange gains/losses and taxes that might be applicable to foreign investors.)

10. Suntec REIT (Annualised return: +5.91%)

Since 2004, every $1,000 investment in Suntec REIT would’ve turned into $1,360. Including the dividends, every $1,000 would cumulatively become $2,980.

9. CapitaLand Ascott REIT (Annualized return: +7.07%)

Since 2006, every $1,000 investment in Ascott REIT would’ve turned into $1,530. Including the dividends, every $1,000 would cumulatively become $3,190.

8. CapitaLand Integrated Commercial Trust (Annualised return: +7.09%)

Since 2002, every $1,000 investment in CICT would’ve turned into $2,090. Including the dividends, every $1,000 would cumulatively become $4,210.

7. CDL Hospitality Trust (Annualized return: +7.12%)

Since 2006, every $1,000 investment in CDL Hospitality Trust would’ve turned into $1,480. Including the dividends, every $1,000 would cumulatively become $3,220.

6. Frasers Centrepoint Trust (Annualized return: +7.81%)

Since 2006, every $1,000 investment in FCT would’ve turned into $2,000. Including the dividends, every $1,000 would cumulatively become $3,590.

5. Mapletree Logistics Trust (Annualized return: +8.39%)

Since 2005, every $1,000 investment in MLT REIT would’ve turned into $2,380. Including the dividends, every $1,000 would cumulatively become $4,260.

4. CapitaLand Ascendas REIT (Annualized return: +8.94%)

Since 2002, every $1,000 investment in A-REIT would’ve turned into $3,110. Including the dividends, every $1,000 would cumulatively become $6,040.

3. ParkwayLife REIT (Annualized return: +9.40%)

Since 2007, every $1,000 investment in PLife REIT would’ve turned into $2,900. Including the dividends, every $1,000 would cumulatively become $4,210.

2. Mapletree Commercial Trust (Annualized return: +9.72%)

Since 2011, every $1,000 investment in MCT would’ve turned into $1,980. Including the dividends, every $1,000 would cumulatively become $3,050. (Note: Mapletree Commercial Trust has been renamed to Mapletree Pan Asia Commercial Trust following its merger with Mapletree North Asia Commercial Trust.)

1. Mapletree Industrial Trust (Annualized return: +10.93%)

Since 2010, every $1,000 investment in MIT would’ve turned into $2,420. Including the dividends, every $1,000 would cumulatively become $3,850.

In summary, here is John’s overall performance:

The most impressive REIT in John’s portfolio, in term of absolute return, is CapitaLand Ascendas REIT. Every $1,000 investment in Capitaland Ascendas REIT would’ve turned that into $6,040! His net gain in Ascendas REIT alone is more than enough to cover two other losses in LMIR and MacarthurCook Industrial.

Most importantly, John is still very profitable without having to come out with any additional capital to subscribe to any rights. However, if he had subscribed to them (including excess rights), he would have made more money since rights are usually sold at a larger discount.

Compared to last year, this year’s REIT overall performance have come down slightly but the dividends have not! John’s portfolio of REITs still pays stable dividends. In fact, the dividends accounted 78% of the total return. So at the end of the day, John continues to receive regular dividends from his S-REITs in good times and in bad.

As you can see, REITs remain a good choice for anyone who wants to build a steady and consistent stream of passive income. However, please note that you shouldn’t buy or avoid a REIT just based on the data above as past performance is not necessarily indicative of future results. The bankruptcy of Eagle Hospitality in 2021 (listed record of only two years) serves as a warning that not all REITs are created equal. That’s why it is important to have a proper investment process to help you identify and invest in the right REITs that will give you a continual stream of passive income and capital gains down the road.

More than half of your holding period is held during an extremely low interest rate environment. One can’t just say some of the REITs are in higher rate period (before 2008) and draw parallels to today’s environment since you are compounding their returns. Also, some of the earlier REITs like Ascendas then went public on lower-than market rate rentals, hence there are a lot of low hanging fruits for those who hold their shares since IPO.

Hi Andrew, that’s a good point! Thanks for bringing it up. Research from the U.S. and Singapore has shown that REITs don’t necessarily underperform in a rising interest rate environment. You can read more below. Hope this helps!

https://fifthperson.com/can-we-buy-reits-in-an-inflationary-and-rising-interest-rate-environment/

https://www.spglobal.com/spdji/en/documents/research/the-impact-of-rising-interest-rates-on-reits.pdf

https://www.lionglobalinvestors.com/en/resources/pdf/reports/LEPF_Rising%20IR%20and%20Impact%20on%20SREITs_Sep17.pdf