We often talk about buying great businesses. But what makes a business ‘great’?

Profitability is one. And we measure profitability by return on capital. We look at efficiency by studying net income margins, free cash flow margins, cash conversion cycles among others. We examine capital intensity by looking at capital expenditures, equity, good will (normally acquisitions), debt, among other things. But further, how do we differentiate the great business from the average business?

I argue that the difference is made in the reinvestment rate.

A quote initially made by Buffett himself goes as such:

‘Leaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return.’

So what exactly does it mean?

To make it simpler to understand, we can simply translate that as — the best business to own is one that can (re)invest a lot more money at very high profits over a long period of time.

Let us put this into practice and show you why this is crucial.

Coffee shop dynamics

Imagine today you could buy the bustling, busy, fight-a-war-to-find-a-seat coffee shop near you for $10 million dollars. After tax, and after paying off the bills you need to pay, you net a profit of $1 million at the end of each year. Not bad right? That’s $1 million in profit out of a $10 million initial investment. That’s 10% right there.

Let’s progress down the timeline a little bit. Let us imagine that nine more years have passed and by year 10, you’ve recouped your entire initial investment. From now on, every year, the coffee shop simply generates another $1 million of cash to put into your pocket. Sound good? Sure.

Is the coffee shop a great business?

I’d argue not so much. First, earnings aren’t growing. It spits out cash reliably, but that cash is worth less and less every year due to inflation. Second, we argued above that the difference between the average business and the great business is one that can employ a lot more money at much higher rates of profitability. In this first example, we have a coffee shop with 10% returns for an initial $10 million investment.

So what would make this coffee shop a great business? Let’s imagine we built a brand around it. We allow customers to use a dedicated payment system to earn a discount on all items bought at our coffee shop. And then we expand. Aggressively. We use the management skills, the logistics knowledge we have, the supply chain we have, and we go from just one coffee shop to 10 coffee shops. All with the same layout, same management, same shops, same discounted items, available at reasonable prices to the people.

Let us imagine that the returns stay the same: 10%. But now that we can pour the profit of $1 million into expanding the business every year to earn even more money. What would our returns look like every year?

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Annual Profit ($ million) | 1.0 | 1.1 | 1.2 | 1.3 | 1.5 | 1.6 | 1.8 | 1.9 | 2.1 | 2.4 |

| Total Capital Invested ($ million) | 10.0 | 11.0 | 12.1 | 13.3 | 14.6 | 16.1 | 17.7 | 19.5 | 21.4 | 23.6 |

By Year 10, we would generate $2.4 million per year in profits. Assuming we don’t grow anymore, we already clawed back our initial outlay of $10 million by Year 7-8, and the rest is a home run at double the rate of what we had originally.

Neat.

This is what it looks like when we can reinvest our profit at the same 10% returns. However, reinvesting doesn’t necessarily mean that you can only earn the same returns; it can often be higher if done well.

Take our example. Would an expanding chain of coffee shops with inbuilt card payment systems encouraging users to pre-fill cards with cash, a more efficient supply chain, and larger orders only earn the same return on capital as a singular coffee shop?

I’d argue no. Pre-paid cards mean more cash in the bank. More coffee shops means a more efficient supply chain which means every dollar we spend on our supply chain nets more returns (since one truck can now deliver to 10 coffee shops instead of just one). Larger orders mean we can negotiate for lower prices. It’s increased efficiency with scale all around.

So let us imagine instead that we are able to now reinvest cash at 15% returns. What does that look like?

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Profit ($ million) | 1.0 | 1.7 | 1.9 | 2.2 | 2.5 | 2.9 | 3.3 | 3.8 | 4.4 | 5.0 |

| Total Capital Invested ($ million) | 10.0 | 11.0 | 12.7 | 14.5 | 16.7 | 19.2 | 22.1 | 25.4 | 29.3 | 33.6 |

By Year 10, instead of drawing back just $2.36 million in profits, we’re now doing about $5 million! We’ve clawed back our initial investment within 5-6 years, and leaves us drawing five times the initial profit of $1 million per year.

Reinvestment has real benefits.

But what about real-world examples? Let’s take a good look.

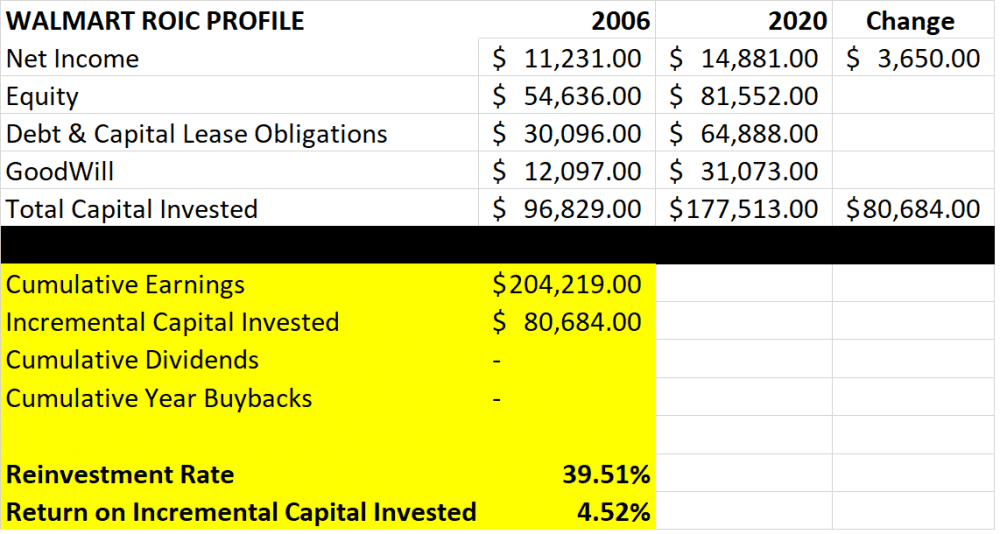

Walmart

This is Walmart.

If you look closely, you notice that Walmart reinvests at decent rates (39.51%), and they haven’t been able to earn high returns on the extra cash they invested (4.52%).

Let’s look at another retailer.

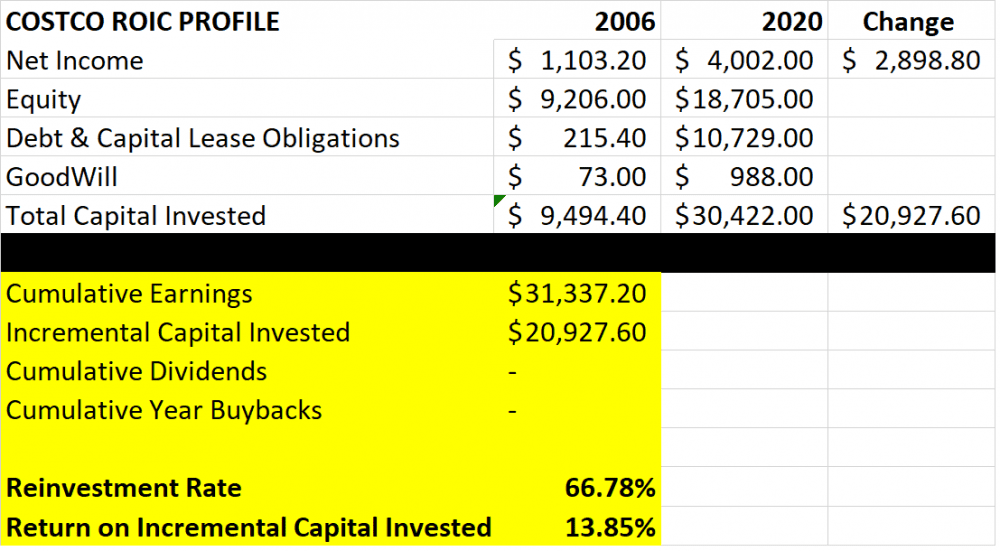

Costco

This is Costco.

The real difference here is in the reinvestment rate and returns. Costco reinvested 66% of its earnings back into its business versus Walmart’s 39%, and earned 13% returns on their reinvestment. (Costco memberships are paid in advance and that accounts for more cash coming in than going out in case you’re wondering how a business can reinvest more than 100% of its earnings.)

How did reinvestment rates affect both companies?

In 2006, Walmart was worth $46 a share. By end-2021, it was worth $144 — a 209% increase.

In 2006, Costco was worth $50 a share. By end-2021, it was worth $567 — a 1,000% increase.

There’s a small host of other factors, but by and large we can agree that reinvestment rate and the returns these reinvestments earn are extremely important.

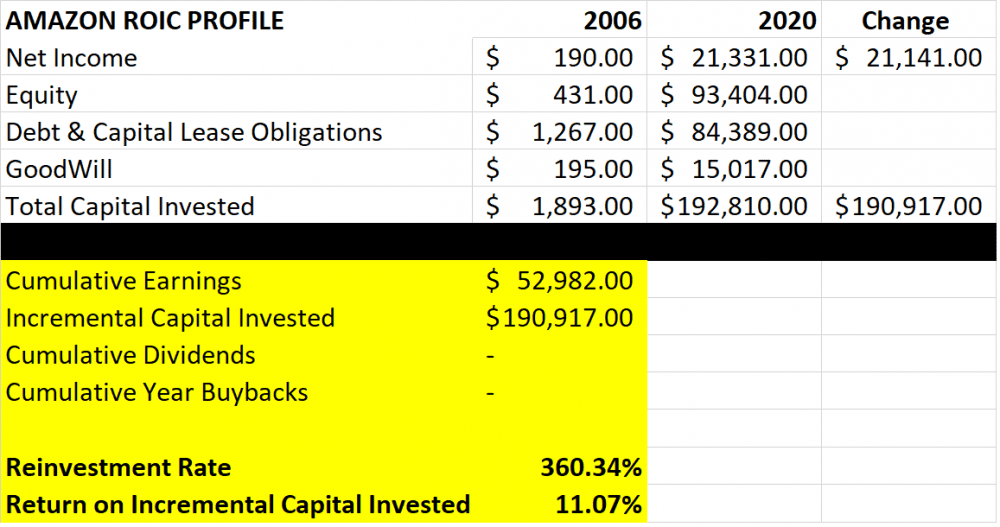

Amazon

I know my headline only mentioned Walmart versus Costco. But what if we want to take a look at an even more insane example?

What about Amazon?

The thing about Amazon’s amazing growth is its cash conversion cycle. Because customers pay before products are shipped and Amazon is able to strong-arm suppliers for favorable term payments, Amazon enjoys a significant negative cash conversion cycle. Amazon also enjoys significant cash flow from its subscription services like AWS and Prime.

They always have more cash coming in than going out. And because of that, their reinvestment rate is a gigantic 360%. The returns on their incremental investments are great as well: 11%. Needless to say, Amazon’s share price has been spectacular.

What is the one thing separating all of these companies? The reinvestment rate. And the returns on that reinvested capital.

The fifth perspective

On top of figuring out what the business models are, how profitable they are, how good leadership is, whether the company has good capital allocation policies, whether managers are overpaying themselves, what the risk factors are; I find myself 90% of the time, trying to figure out these two simple factors.

- How much extra money can these business employ?

- How much profit can they derive from extra money employed?

The first is limited by their reinvestment runway. Netflix is obviously not as limited by capital reinvestments as say Ford Motors or Tesla. How many cars can an average person own? One or two? But that same person can consume endless amounts of content over their lifespan. So that’s kind of how I think about reinvestment runways.

And the second is how much extra money the business can make off its reinvested capital. Which is directly linked to either (1) size and efficiency (à la coffeshop dynamics) or (2) pricing power (how much can Netflix raise prices on you and me before we say no more and cut our subscriptions. I’d wager they can raise prices a little bit each year and consumers will happily pay up if we find the value in it.)

The next time you’re thinking about buying a company, think about these factors. It could make the difference between a decent return versus a great (or insane) one.

Dear Irving Soh,

Thanks for sharing the idea of looking into Reinvestment Rate and Return of Incremental Capital Invested.

Reinvestment Rate

I think this rate is looking into efficiency of Invested Capital (Incremental) over Net Profit (Cum.), given period of Time.

Can you share with me why Invested capital was using Delta (Recent Year minus Beginning of Year), while Net Profit was summation accross the period of interested year?

Return of Incremental Capital Invested

Can you share with me why you are using Delta of Net Profit (Recent Year minus Beginning of Year), instead of summation across the period of interested year?

Hi Alex,

The change in net income over periods and change in total capital used over periods is useful to help measure how much capital was required to generate how much additional net income. The use of net profit summations across time is simply to measure reinvestment rate. there’s no linkage between the two.