Every year, Warren Buffett writes an annual letter to the shareholders of Berkshire Hathaway. His annual letters are one of the most widely read documents in the business world as investors clue in on Buffett’s outlook for the market and economy as well as Berkshire’s performance the past year:

To the Shareholders of Berkshire Hathaway Inc.:

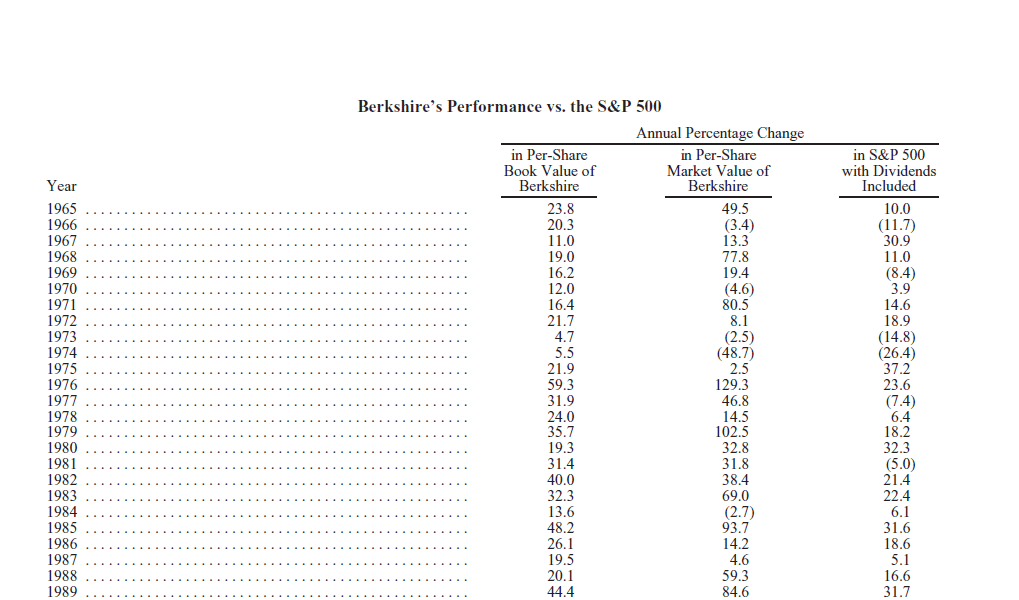

Berkshire’s gain in net worth during 2015 was $15.4 billion, which increased the per-share book value of both our Class A and Class B stock by 6.4%. Over the last 51 years (that is, since present management took over), per-share book value has grown from $19 to $155,501, a rate of 19.2% compounded annually.

During the first half of those years, Berkshire’s net worth was roughly equal to the number that really counts: the intrinsic value of the business. The similarity of the two figures existed then because most of our resources were deployed in marketable securities that were regularly revalued to their quoted prices (less the tax that would be incurred if they were to be sold). In Wall Street parlance, our balance sheet was then in very large part marked to market.”

By the early 1990s, however, our focus had changed to the outright ownership of businesses, a shift that diminished the relevance of balance-sheet figures. That disconnect occurred because the accounting rules that apply to controlled companies are materially different from those used in valuing marketable securities. The carrying value of the “losers” we own is written down, but “winners” are never revalued upwards.

We’ve had experience with both outcomes: I’ve made some dumb purchases, and the amount I paid for the economic goodwill of those companies was later written off, a move that reduced Berkshire’s book value. We’ve also had some winners – a few of them very big – but have not written those up by a penny.

Over time, this asymmetrical accounting treatment (with which we agree) necessarily widens the gap between intrinsic value and book value. Today, the large – and growing – unrecorded gains at our “winners” make it clear that Berkshire’s intrinsic value far exceeds its book value. That’s why we would be delighted to repurchase our shares should they sell as low as 120% of book value. At that level, purchases would instantly and meaningfully increase per-share intrinsic value for Berkshire’s continuing shareholders.

The unrecorded increase in the value of our owned businesses explains why Berkshire’s aggregate market value gain – tabulated on the facing page – materially exceeds our book-value gain. The two indicators vary erratically over short periods. Last year, for example, book-value performance was superior. Over time, however, market-value gains should continue their historical tendency to exceed gains in book value.

Read the entire Berkshire Hathaway 2015 Annual Letter here.