Oversea-Chinese Banking Corporation (OCBC) is the second-largest financial institution in Southeast Asia, with a market capitalisation of over S$72.8 billion as of 15 May 2025. Over the years, OCBC has expanded its international presence and now operates more than 470 branches and representative offices across 19 countries and regions.

Amid ongoing tariff tensions and the possibility of interest rate cuts in 2025, bank stocks have felt the impact. This year, I’ve decided to arrive early at 1:00 p.m. to attend the management presentation before the annual general meeting at 2:00 p.m.

Here are five things I learned from the 2025 OCBC AGM.

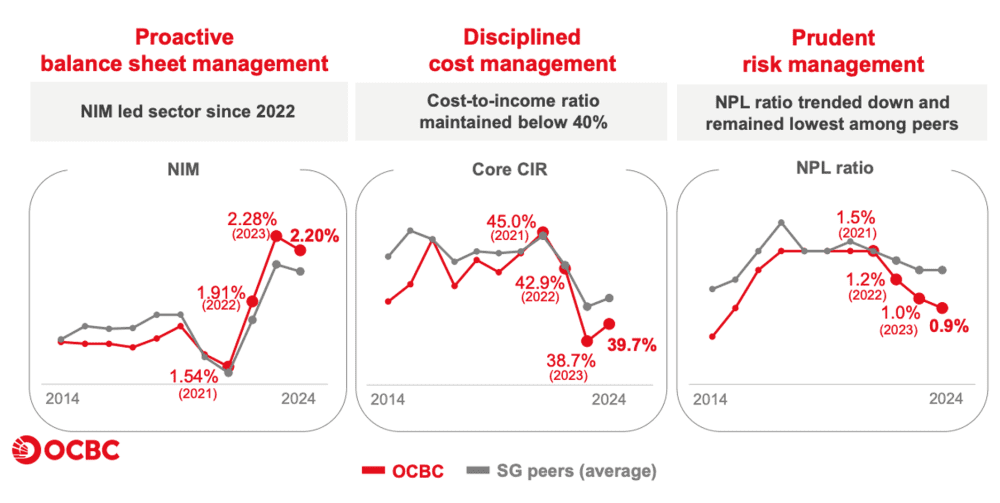

1. During the management presentation, OCBC’s leadership highlighted that the bank outperformed its Singaporean peers across three key metrics. First, its net interest margin (NIM) peaked in 2023 before declining to 2.20% in 2024. While this decline was industry-wide, OCBC’s NIM remained above that of its peers.

Second, the bank maintained the lowest cost-to-income ratio at 39.7%, reflecting disciplined cost management alongside continued investments in business growth, productivity, and operational efficiency. Lastly, the non-performing loan (NPL) ratio improved significantly, falling to 0.9%—a result of OCBC’s prudent risk management practices, again outperforming peers.

2. OCBC’s management shared that, based on customer feedback, the impact of tariffs is expected to be spread across the value chain — affecting producers, intermediaries, brand owners, and consumers. This broad distribution of cost pressures ultimately results in reduced business profitability and higher consumer prices. Customers are also expected to diversify exports to non-U.S. markets and reconfigure their supply chains, although this transition will take time. Management further noted that sectors less reliant on the U.S. market include domestic industries such as construction and food & beverage, as well as growth areas like data centres and renewables.

3. Management expects three rate cuts in 2025 and acknowledged that this will put pressure on the net interest margin, which in turn will affect net interest income. However, CEO Helen Wong stated that the potential impact on net interest income is expected to be offset by loan growth, higher fee income, and continued expansion in wealth management.

4. A shareholder asked about the wealth management business in Singapore compared to Hong Kong. In response, Wong explained that while Hong Kong currently has a larger wealth management market, Singapore’s is growing rapidly. She added that both markets are expected to achieve high single-digit growth. Wong also noted that Singapore and Hong Kong serve as key financial centres in Asia, and wealth is not confined to one location, as investors have the flexibility to access services across multiple financial hubs.

5. During the meeting, Chairman Andrew Lee addressed the rumour regarding the potential sale of OCBC Centre. He explained that, as with any responsible board, they regularly review ways to enhance the value of their assets. A recent study was conducted to explore potential improvements to OCBC Centre, but this was mistakenly interpreted by some as a plan to sell the property. He clarified that OCBC Centre is a freehold property and has been designated as a national heritage site, and therefore, the bank has no intention of selling it.

The fifth perspective

The 2025 OCBC AGM provided valuable insights into the bank’s resilience, strategic priorities, and disciplined management approach amid a challenging macroeconomic environment. Despite headwinds from tariffs and anticipated interest rate cuts, OCBC remains focused on maintaining strong fundamentals, expanding its regional footprint, and growing its wealth management business. The management’s transparency and forward-looking outlook offered confidence that the bank is well-positioned to navigate uncertainties and continue delivering long-term value to shareholders.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

Victor, is OCBC still the Fifth Person’s top pick out of the three big Singapore Banks?

I know Rusimin always seems to like OCBC best (as an investment). As a long-term investor in all three (DBS, OCBC and UOB) I’m a happy camper at the moment.

Hi Jonathan, I think all three banks are equally good. OCBC is cheaper in terms of valuation.