With more and more electric vehicles (EVs) on the road, have you ever wondered if there are ways to invest beyond just the car brands? The EV revolution is not only transforming how we drive but also reshaping the entire industry, creating a network of investment opportunities that extends from remote mines to neighbourhood charging stations.

In 2024, 17 million EVs were sold worldwide, accounting for over 20% of new car sales and bringing the global EV fleet to nearly 58 million, with China leading at 70% market share. This growth is creating strong demand across the supply chain, from raw materials to semiconductors. In this article, we take a closer look at the EV supply chain and where potential investment opportunities may lie.

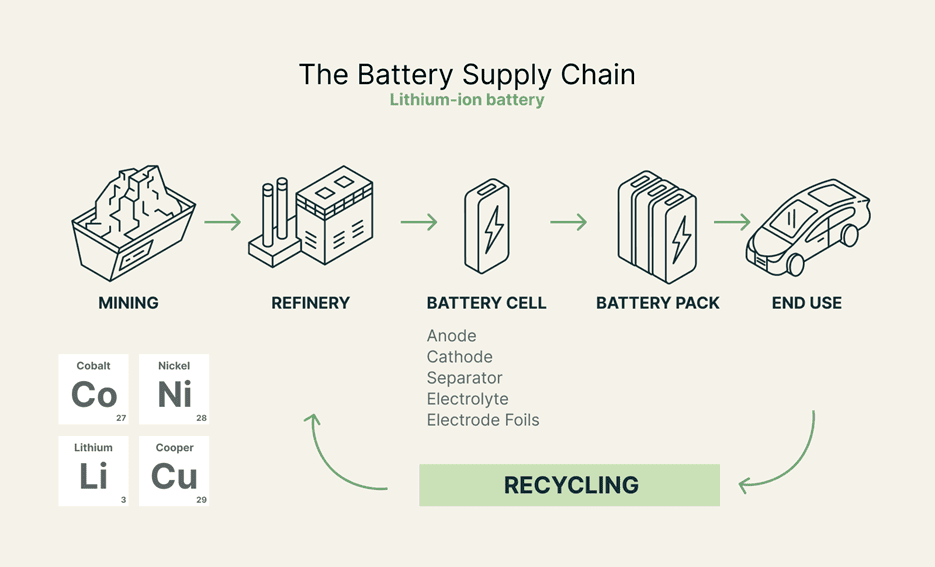

Foundation: Critical raw materials

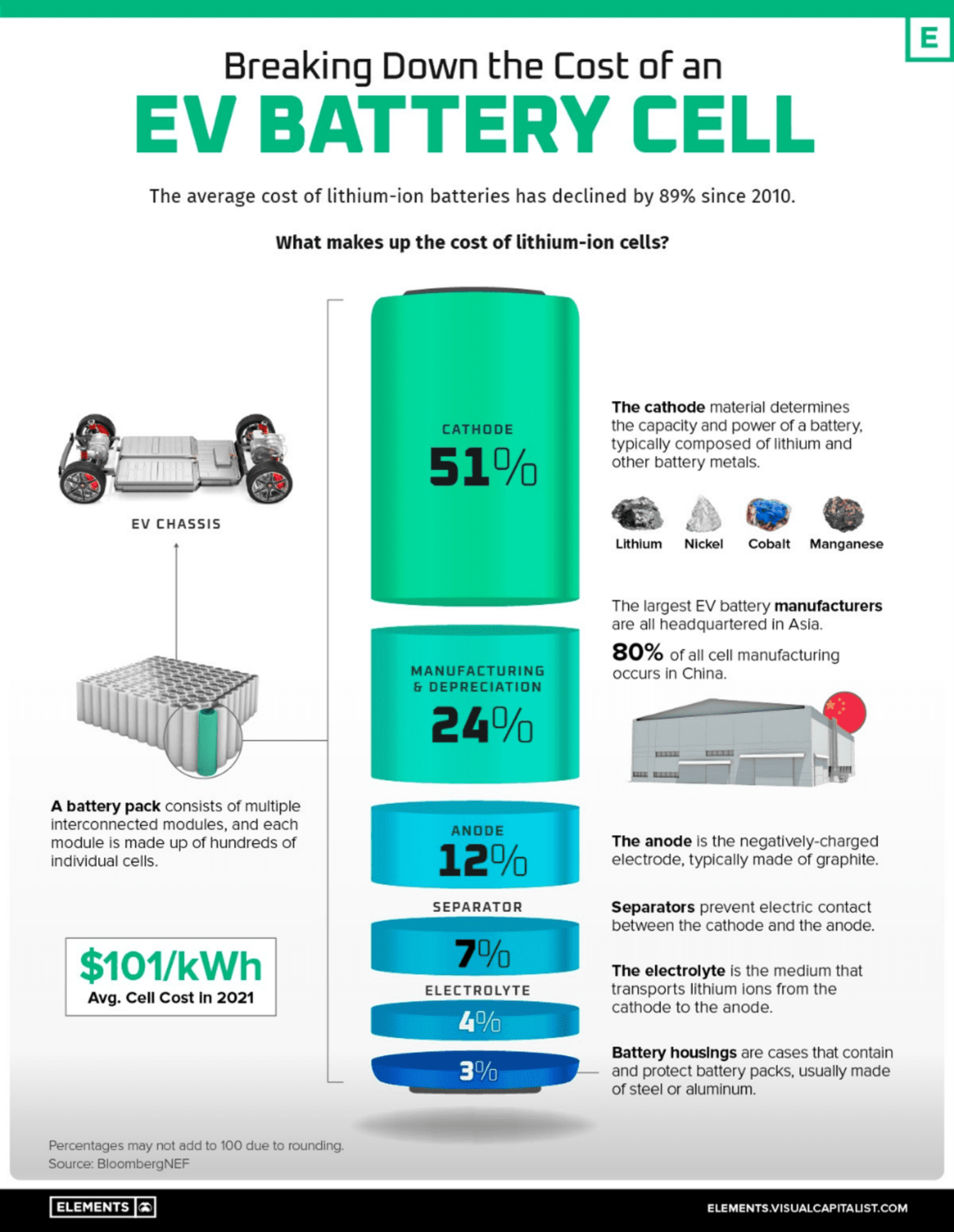

Every EV journey begins deep underground, where specialised mining companies extract the precious metals that power the electric revolution. Lithium, often called “white gold”, sits at the heart of every EV battery, and several publicly traded companies dominate this space.

Albemarle Corporation stands as the global lithium titan, commanding 15-20% of global production capacity. The company operates integrated mining, extraction and purification facilities. They are also one of the key lithium suppliers to Tesla. Meanwhile, Sociedad Química y Minera de Chile leverages Chile’s massive lithium reserves, which hold the world’s largest reserves at 9.3 million metric tons, and is believed to be the second-largest lithium producer.

For those seeking exposure to China’s lithium dominance, Ganfeng Lithium represents the country’s largest producer, with vertical integration spanning multiple continents. If you want a North American alternative, Piedmont Lithium, which is also one of Tesla’s suppliers, position itself as a key player in supply chain diversification efforts.

Beyond lithium, other battery metals present compelling opportunities as well. CMOC Group and Glencore control significant portions of the world’s cobalt, often considered the largest and second-largest cobalt producers worldwide. BHP Group and Vale SA supply the high-purity Class 1 nickel essential for optimal battery performance.

Copper is also critical as EVs require four times more copper than traditional vehicles. Freeport-McMoRan, the third largest copper producer, provides 8.5% of global production (58% in the US) and 70% of US refined copper. Regarding rare earth materials, MP Materials operates America’s only rare earth mine, and recently, they got an agreement and investment from the US Department of Defense and Apple in order to reduce reliance on China.

If you’re curious about how each material is used, the table below provides a summary of their roles in the EV supply chain:

| Mineral | Role in EV Supply Chain |

| Lithium | Core material for cathodes and anodes in nearly all lithium-ion batteries. |

| Cobalt | Improves cathode stability, energy density, charging speed, and lifespan; usage is being reduced in newer chemistries (e.g., Lithium Iron Phosphate). |

| Nickel | Boosts energy density and driving range in high-performance cathodes (NMC, NCA). |

| Graphite | Main anode material in lithium-ion batteries (~95% of EV anodes), with silicon increasingly added to enhance capacity. |

| Rare Earth Elements | Enable high-strength permanent magnets (e.g., neodymium, praseodymium, dysprosium) for efficient EV motors; some EVs are shifting to alternatives. |

| Copper | Essential for wiring, motors, batteries, and charging infrastructure due to superior conductivity. |

Midstream: Processing and Manufacturing

The midstream represents where raw materials transform into usable components, and where China’s dominance becomes most apparent. China processes more than 2/3 of the world’s cobalt and lithium, and more than 90% of the world’s graphite. This critical stage involves multiple specialised processes that most investors overlook.

Battery cell components form the invisible foundation of every EV battery. China controls a staggering 95.9% of global anode material production, 82% of electrolytes (2022 data), plus 85% of global battery cell production capacity.

Specialised companies will normally handle each of the components. Umicore and BASF SE are cathode material specialists, while BTR New Materials and Hitachi Chemica (now part of Resonac) are anode specialists.

Battery cell manufacturing represents the next step, where components are compiled together to become functional energy storage units. CATL dominates with around 38% global market share, supplying to companies like Tesla, Volkswagen and BMW. BYD, being the second largest supplier, offers a unique dual exposure, as they are in both battery manufacturing and EV production.

Moving beyond the battery of EVs, there are still other components required to complete the EV, such as the motor. Companies like Nidec Corporation and Siemens are two major players in the EV motor market. Semiconductors are also a vital part of EVs, as they require 3,000 chips compared to 1,400-1,500 for an average modern car. Infineon leads with a 13.5% share of the global automotive semiconductor market, specialising in power management systems that control how electricity flows efficiently – a crucial aspect for EV operation. NXP Semiconductors holds around 10% of the market, with its automotive processors and vehicle-to-everything (V2X) communication technologies, which enable cars to “talk” to other vehicles, infrastructure, and people for safety and traffic management.

Final mile: Vehicles and infrastructure

Last stage, the downstream segment, where all previous investments culminate in consumer-facing products and services.

BYD, which overtook Tesla in Q4 2024, leads the market with a 15% share. Tesla follows with 12%, supported by its global network of more than 7,000 Supercharger stations and over 70,000 charging connectors. Traditional automakers such as Volkswagen are also stepping up, with significant investments and plans to launch new EV models in 2025.

After your EV battery runs low, you will need to find a place to recharge. Therefore, the development of charging infrastructure creates entirely new investment opportunities. ChargePoint Holdings operates over 342,000 ports and controls about 61% of the public Level 2 charging (faster charging speed than Level 1) market share. EVgo is another leading provider of fast chargers with more than 1,000 locations, which focuses more on DC fast charging.

The fifth perspective

The EV supply chain offers not only opportunities but also significant challenges. Its heavy geographic concentration, particularly China’s dominance across multiple stages, creates vulnerabilities and heightens political risk.

Commodity price volatility will also affect the overall cost; for instance, the lithium price quadrupled between 2021 and 2022 due to rapid EV adoption, which would have a tremendous effect if this ever happened again. Technological advances are also set to accelerate EV adoption. For example, CATL’s sodium-ion batteries – expected to be cheaper, more abundant, and capable of higher storage density – could significantly reshape the industry.

I hope this article has provided a useful overview of the EV supply chain, highlighting opportunities beyond vehicle manufacturers. This is just the beginning; explore the segments that interest you most, and you may uncover hidden opportunities along the way.

Hi Darren,

It will be great to highlighted Nio’s battery swapped infrastructure that they had painfully being building over the past few years.

Thank you for comprehensive report. Nio also hold the one of the biggest charging port in China. The sales of EV car had not picked up and hence the energy sector number look so ugly for past qtr. Once EV cars sales resumed, and moat for BaaS take up, it’s another killer app. Recently they had work with the local grid to invest in smart grid battery swapped kiosk. These are important as it balance up the supply and demand of electricity, further anchored the future of smart grid charging kiosk. Fast charge need a battery storage, otherwise it draw up too high a electricity that actually set the power grid off-balance. NIO battery swap kiosk foresee this issue and solved it few year back in it’s infrastructure construction. in anyway, the financial are terrible due to sales, which they now had picked up and BaaS will kick in a in big way for next year onwards (more EV, better energy revenue, enhance the sticky moat of Nio energy ecosystem (BaaS). This model is heavy investment, not many want to do it, Elon musk brought this before and give up. CATL now are also doing it, this benefit it’s battery business if they built up a network of BaaS.

Hi KC,

Awesome points on Nio’s battery swapping infrastructure. It is a unique angle within the EV ecosystem that complements traditional charging. Seeing CATL and other OEMs to jump in and standardize things so it can finally scale is exciting. It is going to be one of the more interesting parts for us investors to watch over the coming years.