Parkway Life Real Estate Investment Trust (PLIFE REIT) owns a portfolio of 63 properties with a total portfolio size of approximately S$2.23 billion as of 31 December 2023. PLIFE REIT invests primarily in assets that are used for healthcare and healthcare-related purposes.

Most of its assets are located in Singapore (67.6%) which include Mount Elizabeth Orchard Hospital, Gleneagles Hospital, and Parkway East Hospital; followed by Japan (32.2%); and a small portion in Malaysia (0.2%). Here are eight things I learned from the 2024 PLIFE REIT annual general meeting.

1. Gross revenue increased 13% to S$147.5 million in FY2023 from S$130.0 million in FY2022. Net property income (NPI) also increased 14% to S$139.1 million in FY2023 (FY2022: $121.9 million).

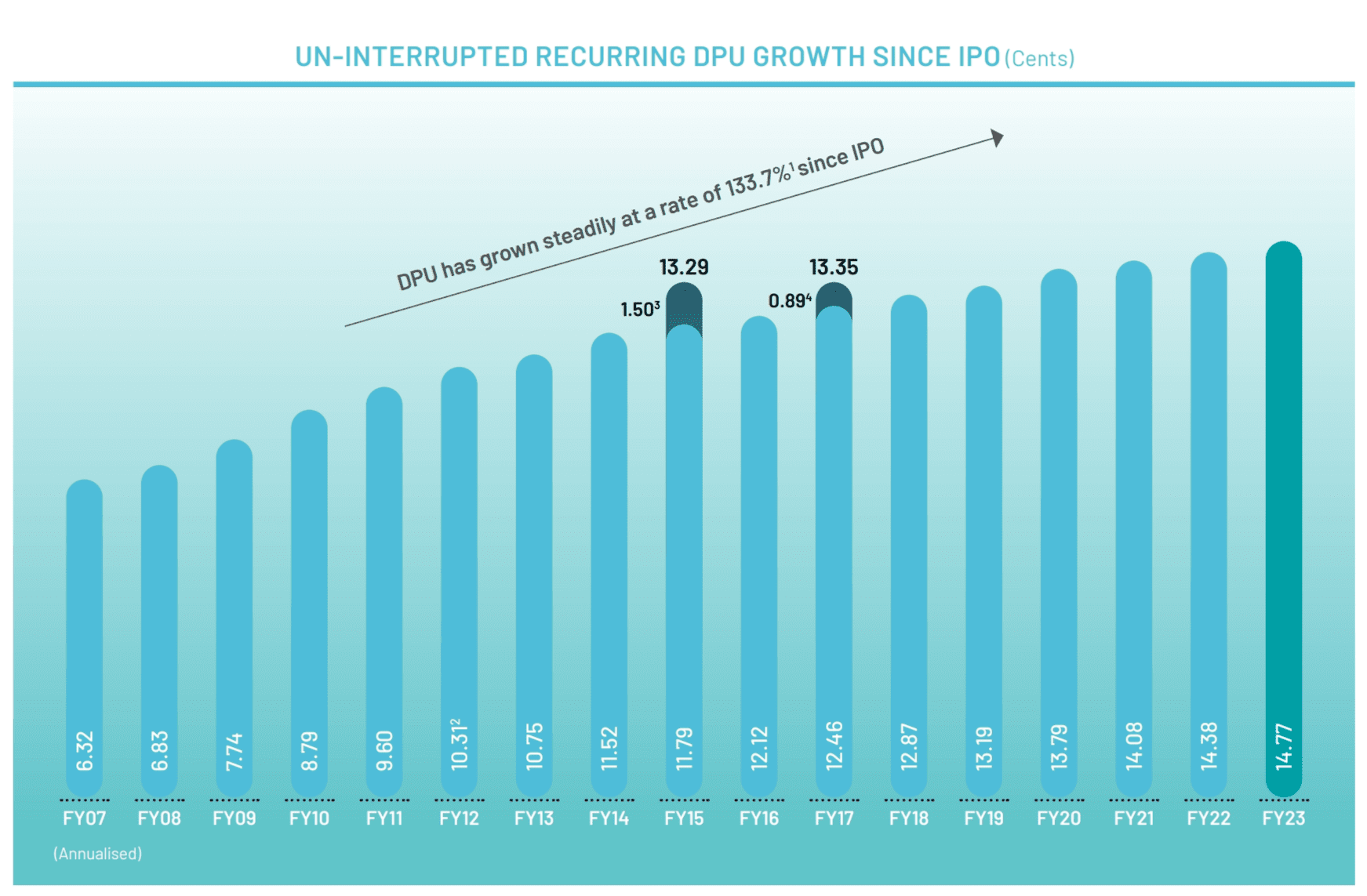

2. PLIFE REIT achieved its 16th consecutive year of uninterrupted distribution per unit (DPU) growth since its IPO, excluding one-off divestment gains in FY2015 and FY2017. In FY2023, its DPU reached a record high of 14.77 cents. Distribution income increased by 2.7%, reaching S$89.3 million, up from S$87.0 million in FY2022. The increase in DPU is attributable to organic rental growth in Singapore hospitals and additional rent contributions from Japanese properties acquired in 2022 and 2023.

3. PLIFE REIT maintains a healthy gearing ratio of 35.6%, which provides ample debt headroom from the target optimal gearing of 40%. All-in debt cost is 1.27%, which the CEO, Yong Yean Chau, highlighted as probably the lowest among Singapore REITs. The REIT’s exposure to low-interest rate markets like Japan aided the low borrowing costs. Interest coverage ratio is 11.3 times, well above the regulatory requirement of 2.5 times, underscoring the REIT’s ability to service its debt obligations comfortably.

4. The REIT maintained a committed occupancy rate of 100%, and its portfolio weighted average lease expiry (WALE) is 16.34 years. Its Singapore portfolio has a master lease that runs until 31 December 2042, with an option to renew for another 10 years.

5. PLIFE REIT is investing S$350 million in a project called ‘Project Renaissance’ to rejuvenate and modernise Mount Elizabeth Orchard Hospital in collaboration with IHH. It aims to completely modernise and transform the medical institution into an integrated multiservice hub. The project commenced in early 2023 and is targeted to be completed by the end of 2025.

6. The CEO disclosed the REIT’s intention to diversify, in collaboration with its sponsor, into a third major market beyond its existing presence in Singapore and Japan. The management is open-minded to Malaysia, but the CEO mentioned concerns about the country’s risks, such as the ringgit’s prolonged currency depreciation against the Singapore dollar. He added that the third market will be in the healthcare sector in a mature economy.

7. Some unitholders raised concerns about the high-interest rate environment and the REIT’s strategy to manage its interest rate exposure. The management explained that PLIFE REIT renews its debt facilities ahead of maturity and aims to lock in interest rates for an extended period of 6-7 years. This pre-emptive strategy helps stabilize interest rates over the long term. It has also issued long-term Japanese fixed-rate bonds, which account for approximately 20% of its total liabilities, to fix its borrowing costs.

As of Q1 2024, the REIT has an average interest rate hedge duration of 3.6 years. With its well-spread debt maturity profile to 2030, no more than 30% of debts will be due in a single year. In any case, around 62% of PLIFE’s revenue is linked to the Singapore Consumer Price Index, providing a natural hedge against interest rate hikes.

8. A unitholder raised concerns about PLIFE REIT’s exposure to potential earthquakes in Japan. The CEO addressed these concerns and highlighted that all acquired properties in Japan are seismically compliant. Additionally, the nursing home assets are predominantly low-rise buildings, reducing earthquake risks. Furthermore, the REIT’s Japanese portfolio is well-diversified across different regions to mitigate the impact of a localized earthquake event. PLIFE REIT also insures all its properties based on potential damage, land cost, and replacement values.

The fifth perspective

PLIFE REIT’s consistent DPU growth, strategic investments, and prudent financial management demonstrated its well-rounded approach to value creation and risk management. The REIT is also actively exploring new markets and undertaking significant enhancements, making it well-positioned to continue its growth. It is still a compelling addition to the portfolio for investors as it is stable and provides sustainable returns.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »