Most investors hate waiting.

Most investors like businesses that are easy to explain, grow steadily, and move with the market. In Singapore, this creates a clear bias toward simple, single-focus companies. Anything more complicated is usually written off as too hard. Boustead Singapore, for one, has been filed under “too hard” for years.

Boustead’s business divisions include industrial real estate, energy engineering, healthcare services, and geospatial technology. Bloomberg classifies Boustead as a “construction & engineering” company, a label that captures neither what the company does nor how it thinks. For most of the past decade, the market has seen this spread as a sign of unfocused management.

But what if that spread is the strategy?

When different businesses run on different clocks

Here’s what makes Boustead unusual: Its divisions aren’t supposed to fit together neatly. Some generate steady cash but won’t grow much. Others need years before their value becomes visible. A few compound quietly behind regulatory moats and switching costs that keep competitors at bay.

Most conglomerates try to squeeze different businesses into a single story. Boustead does the opposite. It lets each business stand on its own and shifts capital between them when the timing is right. That isn’t how conglomerates usually operate. It’s closer to how private equity thinks about building a portfolio. Except instead of working toward a five-year exit, Boustead operates without a clock.

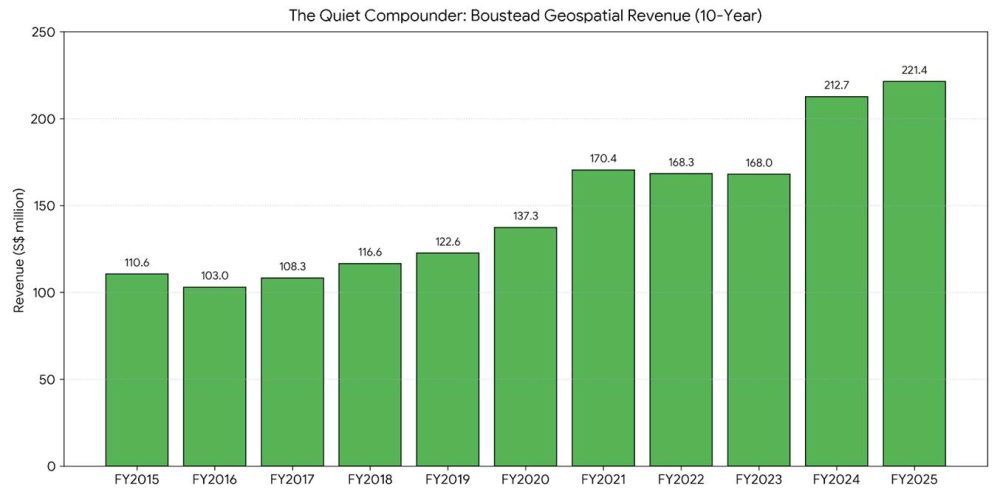

The division Wall Street would actually pay attention to

The Geospatial division is the easiest example of what this patience buys you.

Through Esri Australia and Esri Singapore, Boustead distributes ArcGIS – a software used by governments to manage land records, by utilities to plan infrastructure; and by insurers to model climate risk. Once these systems are built into public agencies, they rarely get replaced. Because the cost of switching here isn’t just money; it’s time, disruption, and political effort.

Revenue here doesn’t surge. It builds quietly. In FY2025, the division reached S$221.4 million, crossing the S$200 million mark for the second year in a row. The figure matters less than what it signals: a business that grows through deep roots, not rapid expansion.

If this division were listed on Nasdaq tomorrow, analysts would likely call it a SaaS business with government-level stickiness. But inside Boustead, the market values it as just another part of a “construction” group.

Here’s why that gap matters.

At current prices, Boustead trades at about 11 times earnings, with a market value of roughly S$1.1 billion. The Geospatial division alone generated S$221.4 million in revenue in FY2025. Historically, this business has delivered profit-before-tax margins close to 20%.

After accounting for tax and Boustead’s partial ownership and applying a conservative 15 times earnings multiple (well below the 25-30x of pure software peers), suggests a standalone value of around S$350-400 million for this one division.

That’s nearly half of Boustead’s entire market value.

For a business with deep government lock-in, multi-year contracts, and dominant positions across Australia and Southeast Asia, the market isn’t valuing Boustead as a company that owns a sticky software business alongside its industrial assets. It’s valuing Boustead as if that software business barely exists.

That gap is the thesis.

Real estate built to wait

Then there’s Boustead’s property arm, which plays a completely different role.

Instead of treating real estate as permanent capital deployment, the company uses it as a “staging” area. Build assets. Stabilize them. Let them season. Then, only when conditions are met, move them off the balance sheet at market prices that reflect years of patient holding. The recent UI Boustead REIT filing in September 2025 marked that moment.

Assets built up over more than a decade, valued at around S$1.9 billion, are now being prepared for a public listing. The properties don’t suddenly become more valuable just because they sit in a REIT. What changes is that the capital tied up in those buildings gets released — capital that Boustead chose to keep locked until the timing was right.

This wasn’t driven by activist pressure or forced by market stress. It was the execution of an option the company had spent years setting up.

That difference matters. It shows a balance sheet designed to wait for the right moment, not react to the urgent one.

When the balance sheet does the heavy lifting

In a high-rate environment, debt limits your options. Boustead’s net cash position does the opposite.

It allows management to build when others can’t afford to. It allowed Boustead to hold assets when competitors are forced to sell. Return cash to shareholders without giving up flexibility. The dividend increase to 7.5 cents per share in FY2025 came alongside the REIT preparations, not after. That order matters. It shows capital recycling isn’t a future idea, it’s already happening.

| In SGD cents | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| Dividend per share | 2.00 | 3.00 | 3.00 | 3.00 | 8.00 | 4.00 | 4.00 | 5.50 | 7.50 |

This isn’t conservatism for its own sake; it’s flexibility built into the structure.

And if there’s one steady hand behind this approach, it’s Wong Fong Fui. He has been running Boustead since 1996. In his FY2025 Chairman’s Message, one line stands out:

“With increasing competition and escalating costs in the industrial real estate space, we continue to explore opportunities and partnerships such as UIB, which holds much potential in further value unlocking for the business on the horizon.”

Read that carefully. He isn’t saying value will be unlocked. He’s saying there is still value to be unlocked. That choice of words suggests the REIT listing is one step in a longer sequence, not the final act.

For a man known as a turnaround artist who transformed QAF from near-bankruptcy into a regional food empire before taking Boustead from S$80 million to over S$1 billion in market cap, that phrasing isn’t accidental.

It suggests the capital recycling process is only beginning.

The fifth perspective

Analysts often say Boustead is hard to value because it doesn’t fit neatly into a single category.

Maybe that’s the point.

Some businesses are built to scale quickly. Others are built to compound in plain sight. Boustead is built to observe, wait, and act selectively. Its divisions aren’t random. They move at different speeds. Each one aligns with a different phase of the capital cycle.

In markets that reward speed and simple stories, that structure gets penalised. But over a full cycle, time itself becomes an asset if you’re set up to hold it without forcing action.

Boustead doesn’t rush to explain itself. It never has.

The real question for investors isn’t whether the company will one day fit what the market wants. It’s whether you’re willing to own a business that runs on a different clock from the one the market checks every quarter.

Most investors won’t.

And it’s why the gap exists.

📢 Announcement: 2026 Enrolment for Dividend Machines is Now Open! Dividend Machines is a training course focused on dividend investing strategies designed to generate a reliable stream of income. If you want to learn how to generate cash flow from your portfolio today, while still benefiting from the long-term, compounding growth of high-quality dividend stocks, then check out Dividend Machines.

Enrolment ends 22 March 2026. We look forward to seeing you inside!

Great article. Thanks for this illuminating piece of analysis.