Almost every investing article, YouTube video, and financial study will tell you the same thing: reinvest your dividends. Let compounding do its thing. Over decades, the difference is enormous. I know this. I’ve read the studies. I’ve seen the charts. And I still choose not to enrol in a dividend reinvestment plan (DRIP).

Before you think I’ve lost the plot, hear me out. This is not a rejection of compounding or data. It’s a deliberate choice that came from a very specific shift in how I think about investing.

The data is real, and I respect it

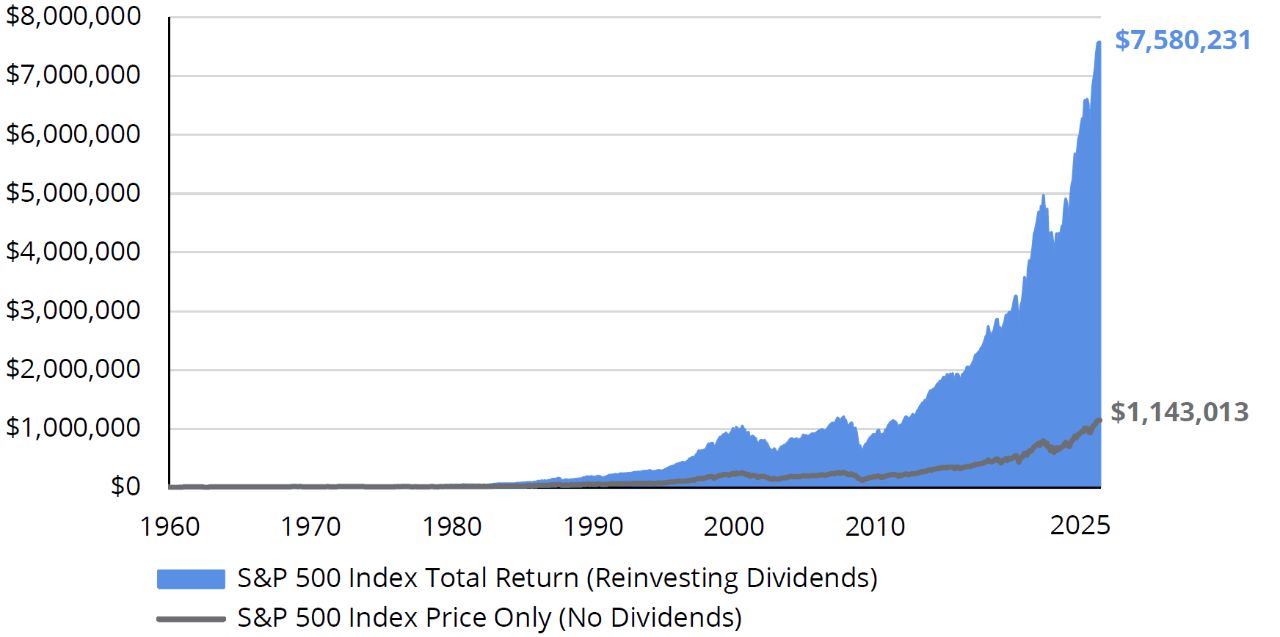

Let me give credit where it’s due. Studies have shown that reinvesting dividends has historically accounted for a massive portion of the stock market’s total returns.

If you had invested $10,000 in the S&P 500 from 1960 to 2023 and reinvested all the dividends, your investment would have grown to over $6.3 million. That is a staggering number.

But if you had invested the same $10,000 decades ago and never reinvested a single dividend, your ending balance would only be $982K; a fraction of what it could have been.

85% of the S&P 500’s total return since 1960 came from reinvested dividends and the power of compounding. The math is clear. Nobody is disputing that. So why would someone who values data make a decision that seemingly contradicts it?

What changed for me

A few years ago, I was a growth investor through and through. My portfolio was packed with high-flying tech names, and dividends were an afterthought. I genuinely believed the path to wealth was betting on innovation and riding the wave.

But over time, the cracks started to show. My net worth swung with every earnings release and Fed announcement. My growth stocks were up on paper, but my actual cash flow was stubbornly negative. I had unrealised gains I could not spend without selling at the worst possible time.

That realisation pushed me towards dividend investing. I began reallocating from high-flyers to dividend payers, building a portfolio that generated real, predictable cash flow. It was one of the best decisions I’ve made.

But here’s the thing. Once I started receiving dividends, I had to make another decision: should I automatically reinvest them using DRIPs (dividend reinvestment plans), or should I collect the cash?

I chose the cash. And I have not looked back.

I want to decide where my next dollar goes

When you turn on a DRIP, your dividends get reinvested back into the same stock at whatever price the market happens to be at. You have no say in when, where, or at what valuation your money gets deployed.

For a broad index fund investor who wants a completely hands-off approach, that makes perfect sense. But I pick individual stocks. And as someone who cares about valuation, a DRIP takes away one of my most powerful tools: the ability to choose where my next dollar goes.

Every quarter, when dividends hit my account, I treat that cash the same way I treat fresh savings. Maybe one of my holdings has pulled back to an attractive valuation while another is trading at all-time highs. A DRIP would automatically buy more of both, regardless of price. By collecting the cash, I get to direct it towards the position that offers the better risk and reward.

Think of it this way. A DRIP is like putting your portfolio on autopilot. That’s great for convenience. But autopilot does not know that one of your stocks just became overvalued, or that another just reported a stellar quarter and is sitting at a bargain price.

You do. And your dividends give you the ammunition to act on it.

It keeps my portfolio in check

Here’s a risk that does not get talked about enough. When you reinvest dividends automatically, the stocks that pay the highest dividends keep getting a larger share of your new capital. Over time, this can quietly skew your portfolio towards your highest yielding positions.

That might not sound like a problem. But high yield stocks sometimes pay high dividends for a reason. Maybe the business is mature and growth has slowed. Maybe the payout ratio is stretched. Maybe the stock price has declined and the yield only looks attractive on paper.

I experienced this firsthand when I was building out my dividend portfolio. It was tempting to let the DRIP do its thing and watch my share count grow. But I realised that I was inadvertently concentrating capital into positions that already had the highest weighting, simply because they paid the most.

By taking dividends as cash, I maintain full control over my portfolio weighting. I decide what deserves more capital and what does not. That discipline matters more than convenience.

Cash flow I can see and feel

I will be honest about another reason. There is something deeply satisfying about watching real cash flow into your account every quarter.

When dividends are automatically reinvested, they disappear into your share count. You might see a fractional share increase here and there, but it does not feel like anything happened. The emotional reward of investing gets muted.

When that same dividend lands in your account as cash, you feel it. You see your income growing. You can track it, chart it, and watch it build. That tangible feedback loop became incredibly important to me once I made the shift to dividend investing. Seeing actual cash hit my account every quarter reminded me that my investments were working, even when prices were flat or down.

Never underestimate the power of staying motivated. The best investment plan is the one you actually stick with.

So what should you do?

1. Know what kind of investor you are. If you invest primarily in index funds and want a completely hands-off approach, a DRIP is a perfectly good strategy. The data supports it, and it removes the temptation to spend your dividends. There is nothing wrong with that.

2. If you pick individual stocks, take the cash. Your dividends are a tool for portfolio management. Use them to rebalance, to average down on quality companies, or to fund new positions. That flexibility is worth more than the convenience of automation.

3. Do not let the data make you feel guilty. Yes, the historical studies show that reinvesting dividends leads to higher total returns. But those studies compare reinvesting versus doing nothing with the cash. If you are actively redeploying your dividends into good opportunities, you are not leaving money on the table. You are making deliberate capital allocation decisions.

4. Track your dividend income. One of the biggest perks of taking cash dividends is being able to see your income grow over time. Use a spreadsheet or an app. Watch the numbers climb. It will keep you motivated and reinforce the long-term habit.

The fifth perspective

Dividend reinvestment plans are a great tool. I am not here to argue that they are bad. For passive index investors, they are arguably the optimal approach. But for those of us who actively manage a portfolio of individual stocks, dividends are not just returns to be recycled. They are fresh capital. They are optionality. They are the cash flow that lets you act when opportunities appear.

The journey from growth investing to dividend investing taught me that real, tangible cash flow matters more than paper gains. And the shift to collecting dividends in cash, rather than reinvesting them automatically, was simply the next step in that same lesson.

The data says reinvest your dividends. I say yes, but collect them, think carefully, and put them to work where they will do the most good.

???? Announcement: Enrolment for Dividend Machines closes this Sunday, 22 March 2026! If you’re looking to learn how to invest in dividend stocks and REITs while building multiple streams of passive income, we highly recommend checking out Dividend Machines before enrolment closes! Once the deadline passes, Dividend Machines won’t reopen until 2027. Start investing for cash flow today!

Thank you for the article. I prefer to be a passive investor because I want to grow for retirement. Actually, when I cash dividends, I would have to pay ordinary income taxes.

Hi Juan,

Thanks for reading! Quick clarification on the tax point. If you’re investing from Singapore or Malaysia, dividends from local listed companies are actually tax exempt for individuals under the one tier (or single tier) corporate tax system. The company has already paid corporate tax, and that tax is final. So whether you take cash or reinvest through a DRIP, you don’t pay any additional income tax either way.

For foreign stocks like US listed shares, withholding tax (e.g. 30% on US dividends) is deducted at source regardless of whether you DRIP or take the cash, so again no difference. The DRIP vs cash decision really comes down to flexibility and where you can deploy the capital best, not tax. Hope that helps!