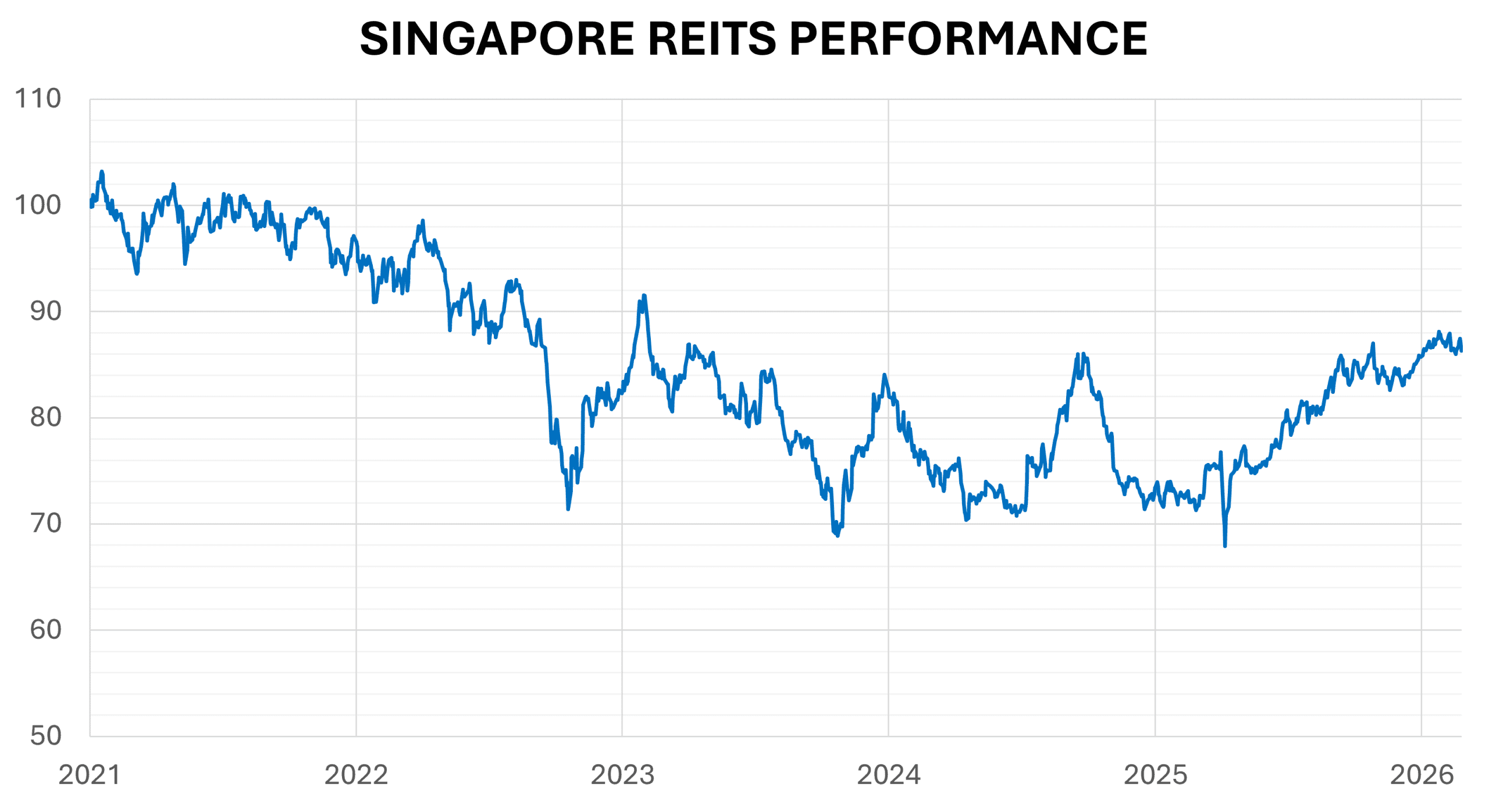

The S-REIT sector saw a genuine recovery in 2025, moving past the false starts of 2024. While the Trump administration pushed for deeper cuts, the Fed’s 1.5% reduction in 2025 brought US rates down to 3.6% from their 5.3% high. For S-REITs, the real victory was in the domestic market: the SORA plummeted from 3.7% to 1.2% over the year. As SORA is the primary benchmark for Singapore commercial loans, this shift significantly lowered borrowing costs and stabilized distributions, turning 2025 into a year of sustained growth rather than a temporary rebound.

Over the past two years, several S-REITs, most notably ARA US Hospitality Trust, Manulife US REIT, and Lippo Malls Indonesia Retail Trust, struggled to maintain the regulatory Interest Coverage Ratio (ICR) of 2.5x. This squeeze was driven by the ‘double whammy’ of declining rental income and surging borrowing costs. The market fallout has been severe: The latter two witnessed share price collapses of over 90%, while ARA US Hospitality (now known as Acrophyte Hospitality Trust) has seen its valuation erode by more than 70% since the pandemic began six years ago.

The Monetary Authority of Singapore (MAS) intervened in late 2024 by streamlining the regulatory framework. By removing the two-tier system, MAS effectively raised the aggregate leverage limit to a universal 50% (up from 45%) and lowered the minimum ICR floor to 1.5x (down from 2.5x). While this provided much-needed breathing room for the broader sector, it could not save the most distressed players.

EC World REIT became the sector’s primary ‘cautionary tale’ in 2025. Despite the more lenient regulatory ceiling, its leverage ratio skyrocketed past 70% following massive write-downs in property valuations. The REIT’s revenue collapsed as its Sponsor (who also served as the main anchor tenant) faced bankruptcy proceedings in China. Consequently, EC World defaulted on its loan covenants and has suspended all distributions since 2024. Even as the wider S-REIT sector capitalizes on falling SORA rates, EC World remains a ‘zombie REIT’: suspended from trading, crippled by illegal mortgages on its Chinese assets, and serving as a stark reminder of the inherent risks of weak Sponsor backing.

Truth be told, several of these troubled REITs were offering double-digit yields in recent years — a classic yield trap that we always warn our Dividend Machines members to steer clear of. Such high yields often prove unsustainable and can lead to significant capital losses for investors, alongside dividend cuts. Our focus should instead be on high-quality REITs capable of delivering both sustainable income and long-term capital appreciation. Based on our years of tracking REIT performance, the Singapore REIT market has thankfully demonstrated a strong track record, with more winners than losers.

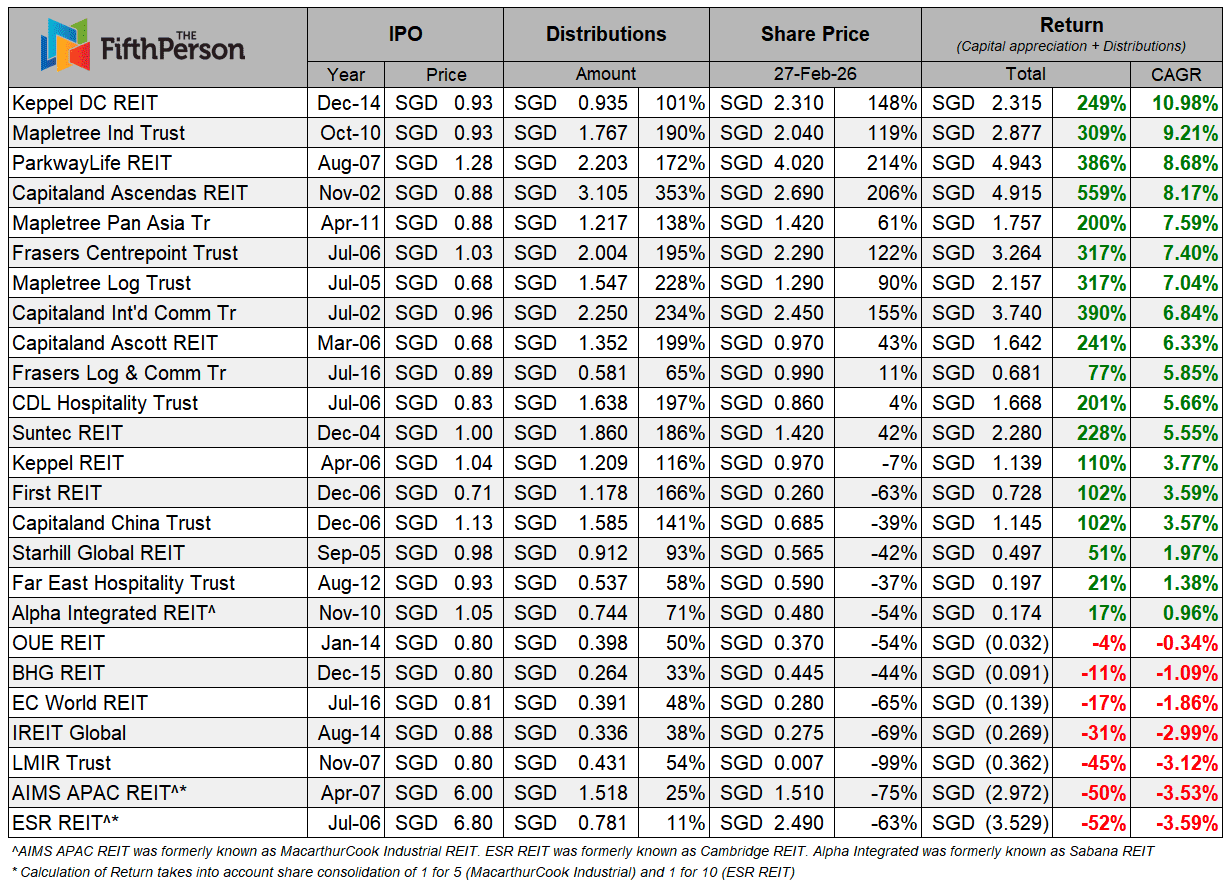

We first wrote about the performance of S-REITs ten years ago, and this time around we revisit their performance by taking into account the latest share prices as of end-February 2026 and the distributions paid to unitholders up to the same period. As before, a REIT needs to have at least 10 years of listing history for us to properly assess its underlying performance. I also make adjustments for factors such as unit consolidations and pre-consolidation distributions to present a more accurate picture of their long-term performance.

This year’s new entries are EC World REIT and Frasers Logistics Trust, which merged with Frasers Commercial Trust to form a new entity called Frasers Logistics & Commercial Trust. Both REITs were listed in 2016.

Once again, we assume that John (a fictional character) invests $1,000 equally in each of these REITs from the day they were listed. Since John is a hard-core income investor who wants to keep all his cash, he chooses not to fork out any additional money to subscribe to rights issuances (if any) and is prepared to accept any resulting dilution. Let’s also assume that John forgets to sell his nil-paid rights, from which he could otherwise have made a profit.

For example, if John had invested in Mapletree Logistics Trust (MLT) during its IPO, his initial investment of $1,000 would have grown to $1,900 (+90% in capital gains) as of 27 February 2026. On top of that, he would have collected total dividends of $2,280 (+228% in distributions).

From the table above, John would have made a nice return in MLT. His initial investment of $1,000 would have grown to $4,170 (+317% in total return), including the dividends received over the years. If John had invested $10,000, his investment would have grown to $41,700. Similarly, $100,000 would have turned into $417,000. In short, the more money he invests, the more he stands to gain. And the longer he holds, the more dividends he will receive. Overall, his annualised return from MLT alone is 7.04% from July 2005 to February 2026.

After investing for more than 10 years, here are the 10 best-performing REITs for John, ranked by annualised return from lowest to highest.

Note: We’ve excluded brokerage costs, currency exchange gains/losses and taxes that might be applicable to foreign investors.

10. Frasers Logistics & Commercial Trust (Annualised return: +5.85%)

Since 2016, every $1,000 invested in FLCT would have grown to $1,110. Including dividends, every $1,000 would cumulatively have grown to $1,770.

9. CapitaLand Ascott Trust (Annualised return: +6.33%)

Since 2006, every $1,000 investment in CLAS would have grown to $1,430. Including dividends, every $1,000 would cumulatively have grown to $3,410.

8. CapitaLand Integrated Commercial Trust (Annualised return: +6.84%)

Since 2002, every $1,000 investment in CICT would have grown to $2,550. Including dividends, every $1,000 would cumulatively have grown to $4,900.

7. Mapletree Logistics Trust (Annualised return: +7.04%)

Since 2005, every $1,000 investment in MLT would have grown to $1,900. Including dividends, every $1,000 would cumulatively have grown to $4,170.

6. Frasers Centrepoint Trust (Annualised return: +7.40%)

Since 2006, every $1,000 investment in FCT would have grown to $2,200. Including dividends, every $1,000 would cumulatively have grown to $4,170.

5. Mapletree Pan Asia Commercial Trust (Annualised return: +7.59%)

Since 2011, every $1,000 investment in MPACT would have grown to $1,610. Including dividends, every $1,000 would cumulatively have grown to $3,000.

4. CapitaLand Ascendas REIT (Annualised return: +8.64%)

Since 2002, every $1,000 investment in CLAR would’ve turned into $3,060. Including dividends, every $1,000 would cumulatively have grown to $6,590.

3. Parkway Life REIT (Annualised return: +8.68%)

Since 2007, every $1,000 investment in PLIFE REIT would have grown to $3,140. Including dividends, every $1,000 would cumulatively have grown to $4,860.

2. Mapletree Industrial Trust (Annualised return: +9.21%)

Since 2010, every $1,000 investment in MIT would have grown to $2,190. Including dividends, every $1,000 would cumulatively have grown to $4,090.

1. Keppel DC REIT (Annualised return: +10.98%)

Since 2014, every $1,000 investment in KDC REIT would have grown to $2,480. Including dividends, every $1,000 would cumulatively have grown to $3,490.

In summary, here is John’s overall performance:

The most impressive REIT in John’s portfolio, in terms of absolute return, is CapitaLand Ascendas REIT, one of the longest-listed REITs in Singapore. Every $1,000 invested in CLAR would have grown to $6,590. His net gain from CLAR alone is more than enough to offset losses from the bottom seven REITs.

John remains highly profitable without having to commit any additional capital to subscribe to rights issues. However, if he had subscribed to them (including excess rights), he would likely have made even more money, since rights are usually offered at a significant discount. Compared to last year, the overall performance of REITs has improved significantly as interest rates continue to fall.

More importantly, John’s REITs continue to pay regular dividends year after year. In fact, dividends accounted for 86.3% of the total return. At the end of the day, John continues to receive steady dividends from his S-REITs in both good times and bad times.

As you can see, Singapore REITs remain an excellent vehicle for building a steady and consistent stream of passive income. However, it is vital to remember that past performance is not a guarantee of future results. The total loss of capital in Eagle Hospitality Trust (which went bankrupt just two years after listing), the ongoing distress in EC World REIT, and the struggles of several US office REITs serve as powerful reminders that not all REITs are created equal.

While a falling interest rate environment generally provides a tailwind—often leading to higher distributions per unit (DPU) across the sector—we cannot afford to be complacent. To succeed, investors need a rigorous investment process to separate quality from noise.

📢 Announcement: 2026 Enrolment for Dividend Machines is Now Open! If you’re looking to learn how to invest in dividend stocks and REITs while building multiple streams of passive income, we highly recommend checking out Dividend Machines before enrolment closes! Once the deadline passes, Dividend Machines won’t reopen until 2027. Start investing for cash flow today!

It will be interesting to also have a column that shows the annulalsed returns of the last 5 years.