Ascott Residence Trust (Ascott REIT) is a hospitality REIT that owns a portfolio of 75 serviced residences and rental housing properties in 38 cites and across 14 countries in Asia-Pacific, Europe, and the United States. As of 31 December 2017, the company has a total of 11,861 apartment units valued at $4.9 billion.

Curious about the accommodation segment of the hospitality industry, I decided to attend Ascott Residence Trust’s annual general meeting to find out about the company’s past year performance and its outlook for the year ahead.

Here are six things I learned from the 2018 Ascott Residence Trust AGM:

1. Revenue increased 4% year-on-year from $475.60 to $496.30 million and gross profit rose 2% from $222.40 million to $226.90 million. This was mainly attributed to the acquisition of Ascott Orchard Singapore, Double Tree by Hilton New York, Citadines City Centre Frankfurt, and Citadines Michel Hamburg, and a stronger operating performance from existing properties.

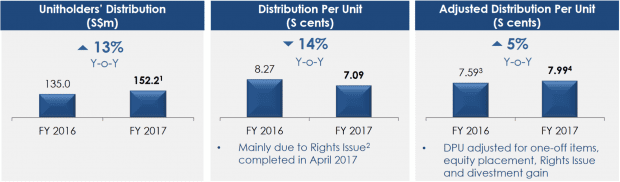

2. Unitholders’ distributable income increased 13% from $135.0 to $152.20 million, but distribution per unit (DPU) decreased 14% from 8.27 cents to 7.09 cents. The large drop in DPU was mainly due to a $442.7 million rights issue to fund the acquisitions Ascott Orchard Singapore and two serviced residences in Germany — Citadines Michel Hamburg and Citadines City Centre Frankfurt. Excluding the rights issue, one-off items, equity placement, and divestment gain, adjusted DPU grew 5% to $7.99 cents in 2017.

Source: Ascott Residence Trust AGM presentation slides

3. Gearing ratio decreased from 39.8% in 2016 to 36.2% in 2017. As at 31 December 2017, 60% of Ascott REIT’s $1.95 billion debt was funded by bank borrowings and the remaining from the debt capital markets. Average debt to maturity is 4.1 years and 13% of borrowings will come due in 2018 and the management plans to refinance this ahead of their maturity dates. Average cost of debt is 2.4% and 81% of the Ascott REIT’s total borrowings are at fixed interest rates.

4. A unitholder wanted to know about the management’s plans to stem the decline in gross rental income for all its four properties in Singapore, which have been gradually declining for 2-5 consecutive years. CEO Beh Siew Kim admitted that the serviced residential market in Singapore is going through a challenging time as a fresh supply of over 3,000 hotel rooms were added in 2017. This new supply comprised around 5% of total rooms in Singapore which indirectly impacted the average daily rate (ADR) and affected the performance of the properties. The CEO expects the outlook for the properties to improve when the supply of new rooms gradually tapers off in 2018 and 2019.

5. A unitholder queried the management on the drop in gross rental income for Ascott Guangzhou, Somerset Heping Shenyang, and Somerset Grand Central Dalian. After divesting Citadines Biyun Shanghai and Citadines Gaoxin Xi’an in 2017, the CEO mentioned that Ascott REIT now has a total of seven properties in China. She added that the performance of its four properties located in China’s first-tier cities have stabilized; Somerset Xu Hui Shanghai saw a double-digit growth in its ADR after the completion of its renovation. Somerset Grand Central Dalian and Somerset Heping Shenyang located in second-tier cities have been affected by the downturn in the shipping and automotive industry respectively.

6. A unitholder was concerned that most of Ascott REIT’s Japanese properties are currently valued below their purchase prices. Citing an example, he pointed out that the value of Somerset Azabu East Tokyo had decreased 49% in 10 years — a drop in value from $79.80 million in 2007 to $43.19 million in 2017. The CEO explained that the drop in value is partly due to the depreciation in of the yen and operational adjustments in terms of numbers over that period of time. However, she said that the Japanese portfolio’s current cap rate of 5% is still in line with the cap rate since acquisition. Chairman Tan Beng Hai added that Japan continues to be an attractive destination and market and Ascott REIT is shifting its focus from acquiring housing units to long-term residential properties. With the cost of borrowing at just around 1%, the management is looking to buy the right assets at the right price. At the end of it, he reminded unitholders to adopt a long-term view when it comes to the company’s developments in Japan.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »