Keppel DC REIT (KDC REIT) is a pure-play data centre REIT listed on the Singapore Exchange. The REIT invests in a diversified portfolio of income-producing real estate assets which are used primarily for data centre purposes.

On 23 October 2019, Keppel DC REIT held an EGM seeking unitholders approval to acquire Keppel DC Singapore 4 (KDC SPG 4) and DataCentre One (DC1).

Keppel DC REIT had raised S$478.2 million through a private placement of 135 million units at an issue price of S$1.744 per unit, and a preferential offering of about 142 million units at an issue price of S$1.71 to fund the acquisition of the two data centres. The preferential offering was well received by unitholders with an oversubscription of 9.3 times.

Here are the seven things I learned from the 2019 Keppel Data Centre REIT EGM:

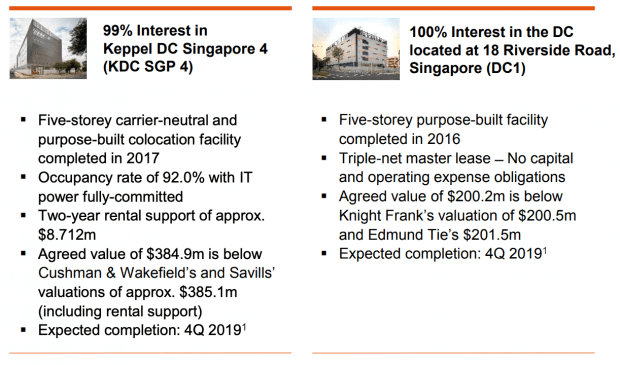

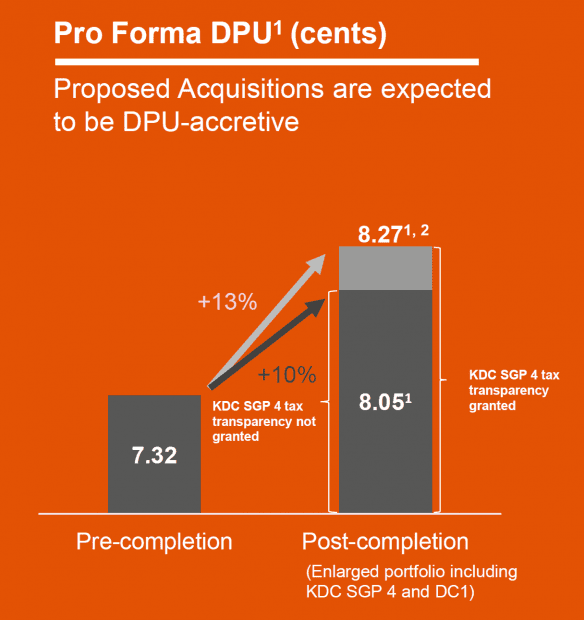

1. The acquisitions for KDC SGP 4 and DC1 — at S$378.9 million and S$201.8 million respectively — are yield accretive. Including tax transparency for KDC SPG 4, the distribution per unit for KDC REIT is projected to increase by 13%.

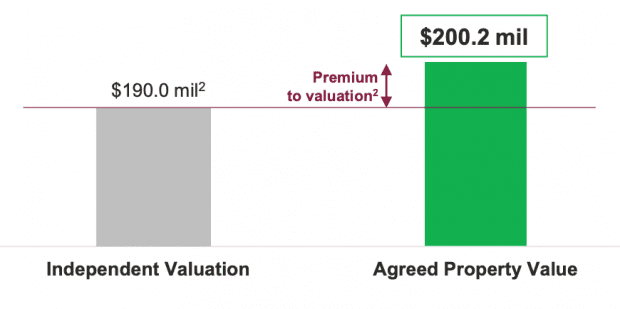

2. Being present at the EGM, it was obvious to me that KDC REIT unitholders were satisfied with the deals as opposed to Keppel Infrastructure Trust (KIT) unitholders who had to sell their 51% interest in DC1. A KIT unitholder was unhappy with selling price of DC1, arguing that it was too low at 15 times earnings, since it still had a stable, long-term lease with Mediacorp for another 17 years. KIT CEO Matthew Pollard replied that the centre was actually being sold at a multiple of 27 (i.e. sale price of S$200.2 million divided by funds from operation of S$7.4 million), which is a 10% premium above the independent valuation price.

3. A KIT unitholder also questioned wondered if the management was selling DC1 at a fair price since it was selling to a sister company. The KIT management explained that the sale of DC1 was done through an open bid and the highest bidder happened to be KDC REIT.

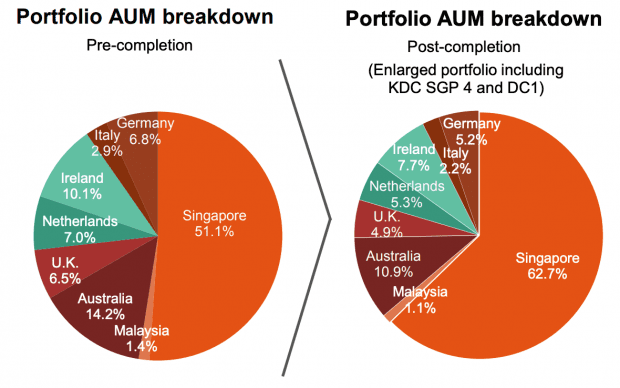

4. The acquisitions will grow KDC REIT’s portfolio concentration of data centres in Singapore from 51.1% to 62.7%. KDC wants to take advantage of the demand for data centres in Singapore — which is estimated to grow at a CAGR of 9.4% between 2018 and 2022 — and expects the supply of data centres to tighten in 2019.

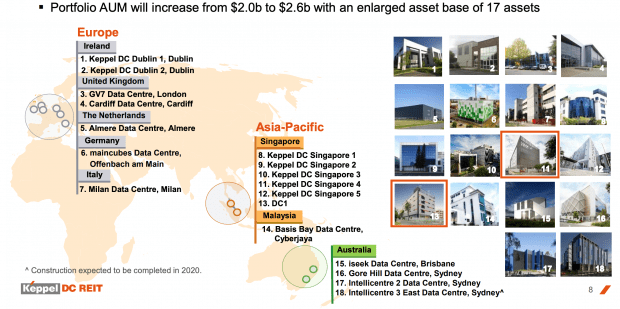

After the inclusion of the SGP 4 and DC1, KDC REIT’s portfolio value will be boosted from S$2.0 billion to S$2.6 billion, comprising a total of 17 assets in Europe, Asia-Pacific, and Australia.

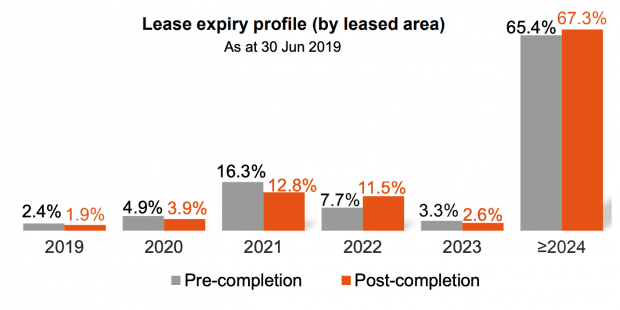

5. Portfolio weighted average lease expiry will increase from 7.8 years to 8.9 years and the portfolio occupancy rate will increase from 93.2% to 94.1%. With an enlarged asset base of S$2.6 billion, the KDC REIT will also have a higher debt headroom to make larger acquisitions, signified by the decrease in aggregate leverage from 31.9% to 30.3% after the acquisition.

6. A unitholder wanted more color on the durability of cashflow from SGP 4 after its two-year rental support ends. CEO Chua Hsien Yang said that the tenant is fully committed to the asset. Based on the contract, the property yield is expected to be around 7.5%, which is higher than the rental support of 7.0%.

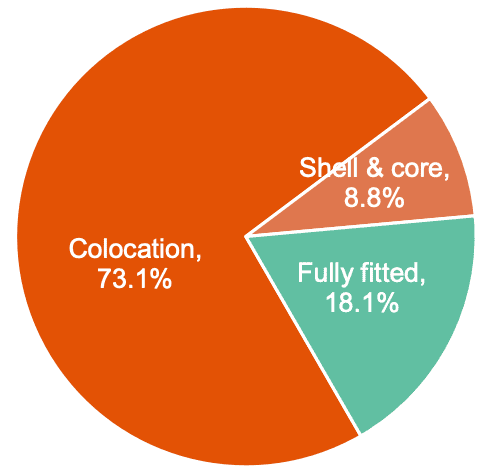

7. A unitholder asked if KDC REIT had any strategies in place to balance its mix of leases in order to minimize colocation risk. The CEO said that he does not have any specific mix of leases for KDC and a high concentration of colocation leases is not necessarily risky. Data centre tenants tend to be sticky and, in a rising market, will give unitholders more income through rental reversions. This is advantageous in Singapore where there is a growing demand in a supply-limited market.

Unlike data centres overseas, KDC’s Singapore portfolio comprises mostly colocation data centres because KDC has a team in place to operate the data centres for customers. This is also the reason why colocation assets generate a higher yield compared to shell & core and fully-fitted data centres. He expects data centres in Singapore to continue being under colocation leases, and data centres acquired outside of the country to be under master leases.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

Hello Kenny,

How did you derive the Per-Completion DPU as being 7.32c ? From my personal spreadsheet, the dpu for Q1 was 1.92c, for Q2 was 1.93c and the recent Q3 Advanced dpu announced for the period 1.7.19 till 24.9.19 was 1.89c.

Are you estimating the final dpu payout for FY19, hence, for the period 25.9.19 till 31.12.19 to be at a mere 1.58c ONLY ?

Hi CK,

The DPU of 7.32 cents was derived from KDC’s 2018 Annual Report. The Manager declared distributions of 3.62 cents per Unit for 1H 2018. For 2H 2018, eligible Unitholders received a distribution of 3.70 cents per Unit.

Good evening Kenny,

Thank you for your reply.

I see that you have used FY18’s numbers for comparison, but if you look at my workings in the above, I have actually used FY19’s actual numbers PLUS an estimation of this quarters payout for comparison. Hence, the difference in our numbers.

Wouldn’t it be more useful if we use FY19’s numbers to extrapolate our dpu growth from these two acquisitions since these acq’s would be completed by this year-end ?

Hmm,… again, from my spreadsheets, for FY18 :-

1) 1H 2018 is right, 3.62 cts from 1Q(1.80c) + 2Q Adv(0.97c) + 2Q Remainder(0.85c).

2) But I captured 2H 2018 as 3.64c only, from 3Q(1.85c) and 4Q(1.79c).

Tks again.

Hey CK,

I get where you are coming from, but I’d rather not make projections based on my own estimated figures. Using actual financial figures will give me a better before-and-after picture of the acquisition, assess the historical performance of the assets and project from 2018 onwards.

I’ve taken the DPU directly from the KDC REIT EGM presentation slides. You probably made some adjustments to yours for your own keeping.

I hope I have answered your questions. If not, feel free to leave another comment and I’ll get back to you as soon as I can.

Hi Kenny,

Appreciated your effort in replying again,..

No worries, it’s not complicated to me. Frankly, everytime I update my spreadsheets and I do these calculations, I feel that I am ‘keeping in touch’ with my investments and having an eyeball on them.

I guessed this is my investing tactic.

You’re most welcome, CK.

That’s definitely a good strategy to keep up to date with your investments.