LPI Capital Bhd is involved in the general insurance business ranging from fire and motor to marine and property insurance. LPI operates across Malaysia, Singapore, and Cambodia. The majority of its revenue (94.4%) was derived from Malaysia in 2019.

Tan Sri Dato’ Sri Dr. Teh Hong Piow, one of Malaysia’s richest men, is the largest shareholder of both LPI and Public Bank Berhad. LPI relies on its agency salesforce that targets mainly corporate customers and relationship with Public Bank for its bancassurance business that serves as a wide distribution network to reach its customers.

LPI continues to grow in tandem with Public Bank but faces headwinds like profit margin erosion from competition ever since the phased liberalisation of motor and fire insurance tariffs.

Here are seven things I learned from the LPI Capital’s 2020 AGM:

1. Revenue increased 5.9% to RM1.6 billion year-on-year in 2019. Likewise, net profit grew 2.6% to RM322.4 million year-on-year over the same period despite rising claim costs and ongoing liberalisation of the general insurance industry in Malaysia.

Profit margins are likely to be compressed in the future as a result of competition and entry of large players into the market. The management is aware of these issues and attempts to increase its market share to offset lower margins.

Source: 2019 LPI Capital annual report

In 2016, LPI recognised a one-off RM150.4 million gain from the disposal of its equity investments, causing a spike in its net profit.

2. LPI is Malaysia’s third largest general insurer with an 8.4% market share. It is also a leader in the fire insurance segment in Malaysia with a market share of 18.8% in 2019. This segment was the single largest contributor of gross written premium in 2019.

LPI has faced fierce price competition since tariffs on premiums have had been removed from motor and fire insurance in phases since 2016. Insurers are given some flexibility to determine their premiums of fire insurance. In 2019, LPI’s gross written premium (GWP) improved 3.7% year-on-year to RM1.5 billion while the general insurance industry suffered a 0.8% decline in GWP over the same period.

Source: 2019 LPI Capital annual report

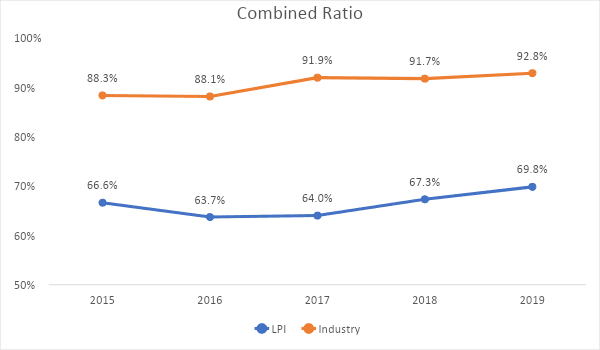

3. In the past five years, LPI’s combined ratio averaged at 66.3%, which is commendable compared to the industrial average of 90.6%. Its 2019 ROE stood at 16.3%, below its five-year return on equity average of 17.9%.

Source: 2020 LPI Capital AGM presentation slides

4. LPI has paid a consistent dividend over the past 10 years. Its average dividend payout was also sustainable at 79.6%. Based on LPI’s share price of RM13.50 (as at 3 July 2020), its current dividend yield is 5.19%.

Source: 2019 LPI Capital annual report

5. Minority Shareholder Watch Group (MSWG) and a number of shareholders wanted to understand more about the impact of COVID-19 on LPI. Executive director Tan Kok Guan shared that the impact was difficult to estimate. LPI’s financial results in the second and third quarters of 2020 will be negatively affected as insurance may not be prioritised. Tan foresees that revenue from fire and motor insurance will be maintained as these would likely be renewed by some owners who seek coverage.

Business activities are expected to return to normalcy only by the fourth quarter and, likewise, the demand for insurance. At this difficult time, LPI provides its clients with flexible payment options and will neither retrench nor cut the salary of its employees. Insurance claims arising from COVID-19 are anticipated to be manageable.

6. MSWG highlighted the six-fold increase in the firm’s unit trust investments to RM235.5 million in 2019. Tan explained that the increased investment was made in view of the existing low interest rate environment. The unit trust funds comprise underlying fixed income assets which provides an expected dividend yield of 3.6% which is higher than that of fixed deposits.

Tan also reassured shareholders that LPI was not too worried about the recent market sell-down including shares of Public Bank that LPI owns as the company intends to hold them for dividends over the long-run.

7. Tan does not view Takaful providers as a direct competitor of LPI and the company does not intend to venture into the Takaful businesses. LPI also seeks to grow organically (without any merger or acquisitions) by developing innovative insurance products that are competitively priced.

LPI has also digitised some of its standard product purchases to cater to different customer needs while keeping brokers to sell more customised products.

The fifth perspective

Despite the economic lockdown that COVID-19 has caused, LPI Capital looks well-equipped to sail through the crisis. Its insurance business doesn’t look to be severely impacted by the pandemic and demand is expected to return to normal in Q4 2020.

LPI’s dividend yield of 5.19% is decent seeing that the company has paid a relatively steady dividend at a sustainable payout ratio of 70-80% over the last 10 years.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »