Mapletree North Asia Commercial Trust (MNACT) is an SGX-listed REIT with retail and office properties in prime locations in China, Hong Kong, and Japan. On the back of sound fundamentals, MNACT seemed poised for further growth until its once-crown jewel Festival Walk mall got badly damaged by Hong Kong protestors in November 2019. (Festival Walk contributed to about 60% of MANCT’s revenue in FY19/20).

As Festival Walk was restored and poised to open its doors again in the new year, COVID-19 struck soon after. Coupled with the pandemic that originated in China, MNACT’s market performance has thus been bleak.

I wanted to find out how MNACT intends to deal with these challenges, so I attended its 2020 virtual AGM. Unfortunately (or otherwise), the AGM left me with more questions than answers. So here are seven things I learned from Mapletree North Asia Commercial Trust’s 2020 AGM:

1. MNACT’s financials were disappointing in FY19/20. Gross revenue and net property income (NPI) fell by 13.3% and 15.7% respectively in FY19/20. MNACT’s distributable income and distribution per unit (DPU) also decreased by 5.3% and 7.4% respectively in FY19/20. This was due to the extensive damage caused at Festival Walk by protestors in Hong Kong on 12 November 2019.

Hence, Festival Walk had to close from 13 November 2019 to 15 January 2020 for repairs. Unfortunately, just as the mall reopened, COVID-19 hit and the mall was forced to close again. Due to these unfortunate events, MNACT granted rental reliefs of up to S$17.8 million to Festive Walk tenants. The fall in income was partially offset by a full year’s contribution from the six office properties in Japan which MNACT acquired on 25 May 2018.

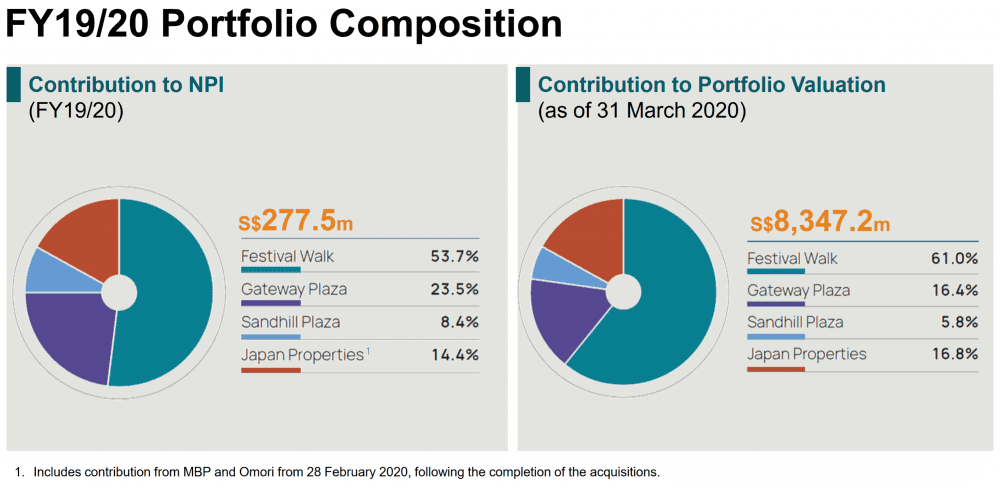

2. MNACT has made efforts to diversify its revenue streams in geographic terms. In FY18/19, MNACT derived 62.0% of its NPI from its only Hong Kong property, Festival Walk. However, the social unrest that erupted in Hong Kong has shown that deriving the bulk of one’s revenue from a single geographic location is not the best idea.

Hence, MNACT has sought to diversify its revenue streams by acquiring two Japanese properties in Q1 2020. The first property acquired is a 26-storey office building, mBay Point Makuhari Building, in Chiba city. The second property acquired is a 13-storey office building, Omori Prime Building, located in Tokyo’s Shinagawa. Since the acquisitions, MNACT derived 14.4% of its FY19/20 NPI from Japan, up from 11.6%. Consequently, Festival Walk’s percentage contribution to MNACT’s NPI fell to 53.7%.

3. Due to the protests and restrictive measures introduced due to COVID-19, Festival Walk has seen a 18.7% and 18.1% y-o-y decrease in footfall and retail sales respectively. However, MNACT implemented distribution top-ups of S$32.9 million for Q3 and Q4 2020 for unitholders, while the REIT received insurance payouts for the loss of income when Festival Walk was closed.

Due to the fluid COVID-19 situation, further rental reliefs might be extended in the future. This puts into limbo the size of future dividends paid to unitholders by MNACT. Although the loss of retail and office revenue during Festival Walk’s closure and property damage sustained are insured, any proceeds received for property damage is capital in nature and will not be distributed.

4. The outlook of Festival Walk remains uncertain. Festival Walk is situated in the residential catchment of Kowloon Tong and is mainly supported by local residents within the catchment area. The protests and the restrictive measures introduced to combat COVID-19 have impacted the businesses of Festival Walk’s retail tenants in FY19/20.

Although there was an improvement in the footfall of the mall due to the relaxation of the social distancing measures from 8 May 2020, an imminent third wave of Covid-19 infections have threatened to derail the recovery. Hong Kong has once again tightened some social distancing measures including limiting the number of patrons allowed at a table in F&B outlets to four and banning dine-in service from 6 p.m. to 5 a.m.

The operating environment for retailers and F&B operators remains difficult. The management expects the socio-economic uncertainties to result in a lower average renewal rental rate for the mall and its performance for FY20/21 to be lower than FY19/20.

5. Gateway Plaza, MNACT’s Beijing office property, is expected to be affected by the weak office market in the capital. Due to persistent U.S.-Sino trade tensions and the pandemic, occupancy rates will be under pressure and rental rates might decrease. Like Festival Walk, Gateway Plaza’s rental renewal rate for FY20/21 is expected to be lower than FY19/20. Although Beijing saw a recent surge in COVID-19 infected cases, it has been largely under control, and as of 24 June 2020, close to 70% of the tenant population at Gateway Plaza is back at work.

However, COVID-19 might prompt a structural shift in the physical office as work-from-home arrangements during the pandemic have made companies realise that telecommuting works as well. Will demand for a physical office diminish down the road? Andwill offices reshape themselves to accommodate more co-working spaces? If so, how will the office market be impacted? With the paradigm shifts happening in the future of work, the office property market is an interesting area to watch out for in the years to come.

6. Sandhill Plaza, MANCT’s Shanghai business park, is expected to remain resilient despite the challenging economic conditions. In Shanghai, measures to stem the spread of COVID-19 have been relaxed and all tenants at Sandhill Plaza have returned to work as of end-June 2020. Sandhill Plaza’s occupancy rate and average rental reversion are expected to remain resilient, as the technology, media, and telecommunications tenants are relatively less affected by the challenging business conditions. Unlike Festival Walk and Gateway Plaza, Sandhill Plaza’s renewal rental rate for FY20/21 is expected to be slightly higher than the expiring rental rate.

7. MANCT’s Japan properties are unlikely to be as affected as its China and Hong Kong properties. As the state of emergency in Tokyo was lifted at the end of May 2020, most tenants have returned to work. However, the COVID-19 situation looks to be worsening again and leasing momentum in Japan’s office sector is still slow. Like Sandhill Plaza, the renewal rental rate of MNACT’s Japan properties is expected to be slightly higher than the expiring rental rate.

MNACT is seeking to reduce its portfolio concentration of Festival Walk by acquiring more Japan retail and commercial office properties in the years ahead. However, this takes time, so in the medium term Festival Walk will continue to be MNACT’s largest asset.

The fifth perspective

MNACT’s dividend yield is currently at 8.1% based its FY19/20 distribution and closing share price as at 7 August 2020. Despite the attractive yield, investors need to account the current risks as the pandemic situation remains highly fluid in China, Hong Kong, and Japan.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »