The COVID-19 pandemic has certainly hit the global economy hard. In particular, travel restrictions have led many major airlines worldwide to significantly slash their operating capacities. Like many of its peers, SIA’s share price has fallen drastically due to the coronavirus.

Near the end of March this year, Singapore Airlines (SIA) announced that it was cutting 96% of its scheduled capacity. This leaves SIA with almost no revenue for the foreseeable future. Hence, SIA has taken to the capital markets to raise up to S$15 billion. This would serve as a war chest that will see SIA through this economic downturn due to the pandemic.

Briefly, here’s how the S$15 billion would be raised:

- 3-for-2 renounceable rights issue worth S$5.3 billion.

- Rights mandatory convertible bonds (MCBs) worth S$3.5 billion.

- Additional MCBs worth S$6.2 billion to be issued within 15 months of the EGM by way of one or more rights issues, if necessary.

SIA held a virtual EGM to get shareholders’ approval for the fundraising. Almost 100% of shareholders approved SIA’s above fundraising plan. I attended the virtual meeting and here are five things I learned from the SIA 2020 EGM:

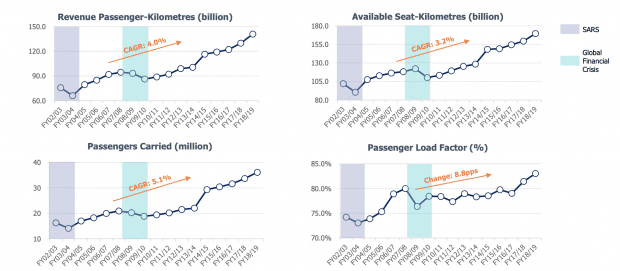

1. SIA recorded a strong performance for the nine months ended 31 December 2019 before COVID-19 struck. SIA increased its revenue, operating and net profit for the period compared to the same period the year before. Likewise, SIA also increased its airline passenger traffic, passenger carrying capacity, passengers carried, and its passenger load factor. However, passenger yield (passenger revenue per passenger per kilometre travelled) remained flat.

Source: Singapore Airlines

2. SIA has recovered from severe economic downturns before. During SARS (2002-2003) and the Global Financial Crisis (2008-2009), SIA’s business took a hit but subsequently recovered. If SIA’s recoveries in the face of past adversities are indicative of what is to come, it’s that SIA has experience bouncing back from its present troubles. However, the virus may be a tougher, more drawn-out challenge as the pandemic has directly impacted air travel globally.

Increase in the above metrics from FY13/14 onward was due to the inclusion of Scoot data. Source: Singapore Airlines rights issue presentation slides

3. The lack of a domestic travel market leaves SIA vulnerable to international border controls. Countries with a large domestic market will see its airlines recovering first as international borders open up more slowly and travellers take a longer time to ease back into international travel. For example, China, with a huge domestic travel market, already started recovering in March. China Eastern Airlines, China’s second largest domestic carrier has plans to resume 70-80% of flights by the end of June. Domestic travel comprised two-thirds of China Eastern’s passenger revenue last year. In contrast, SIA’s resumption of its flights depends on virus containment efforts abroad and easing of international travel restrictions.

4. SIA has taken a slew of measures to mitigate the impact caused by COVID-19 on its operations and financials. CEO Goh Choon Phong said that SIA is working with suppliers and partners (e.g. Boeing) to push for cost reductions and payment rescheduling. SIA has also introduced no-pay leave schemes from 1 April 2020. There will also be a recruitment freeze at SIA and the management team will take 12-30% cuts to their base salaries. The CEO also mentioned how SIA has received strong support from the Singapore government as it recognises the “strategic importance” of SIA to the country’s economy. The government had announced a S$750-million package for the entire aviation sector which includes:

- More than S$400 million to support local wages, through a 75% wage offset for first S$4,600 of monthly wages for every local worker in employment for nine months.

- S$350 million to fund measures like rebates on landing and parking charges, rental relief for airlines, ground handlers and cargo agents.

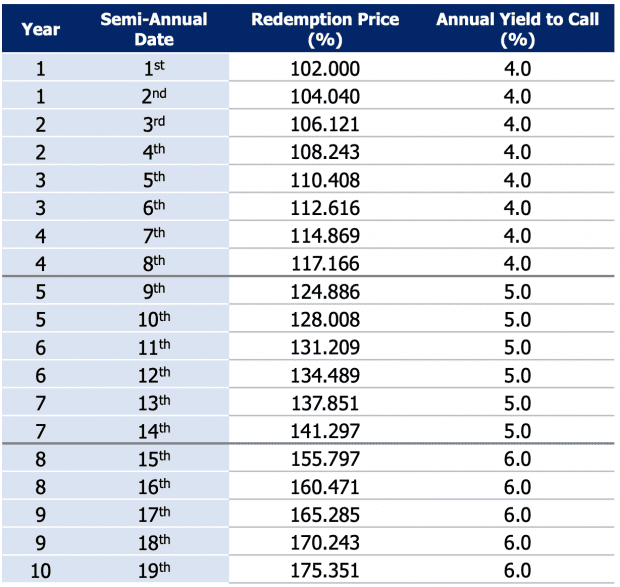

5. SIA’s fundraising ensures sufficient liquidity and a strong balance sheet for the company. SIA’s Senior VP (Finance) Stephen Barnes explained that the MCBs were considered as equity on SIA’s balance sheet, as opposed to debt. This is because SIA need not pay periodic interest payments to MCB holders which relieves SIA of cash flow pressures during this challenging economic time. The MCBs would only be converted upon maturity ten years after its issue date.The MCB’s final accreted principal amount would be $1.80611 for every S1.00 in principal amount of rights MCBs on the maturity data (calculated based on a 6% annual yield to conversion, compounded on a semi-annual basis.) However, SIA can choose to redeem part of the MCBs before its maturity date. The redemption prices are calculated based on (i) the Semi-Annual Date that the Rights MCBs are redeemed and (ii) respective annual yield to call, compounded on a semi-annual basis.

Source: Singapore Airlines rights issue presentation slides

MCBs prevent the immediate further dilution of shareholders who do not subscribe to their pro-rata rights issue. Further, as MCBs are treated as equity, this gives SIA the headroom to raise funds in the debt capital markets in the future.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

After Warren Buffett dump his airline stocks, SIA investors would be wondering whether they should do the same. This write-up is timely for us to make a decision