Listed in 2014, Keppel DC REIT is the first pure-play data centre REIT listed in Asia and on the Singapore Exchange. As of December 2020, it owns 19 data centres in eight countries across Asia Pacific and Europe with the entire portfolio valued at $3.0 billion.

The REIT is one of the companies that actually benefited from the COVID-19 pandemic and delivered a better year-on-year performance in 2020. The pandemic has spurred the digital transformation in our everyday lives ranging from remote working to video streaming. The corresponding surge in internet traffic further reinforces the strong demand for data centres.

Here are eight things I learned from the 2021 Keppel DC REIT AGM.

1. Gross revenue increased by 36.3% year-on-year to S$265.6 million in 2020 while distribution per unit (DPU) grew 20.5% from 7.61 cents in 2019 to 9.17 cents in 2020. The good results were due mainly to full-year contributions from Keppel DC Singapore 4 and DC1 that had been acquired in 2019, as well as new acquisitions in Europe in 2020. DPU-accretive acquisitions have been and will remain a key growth driver of the REIT.

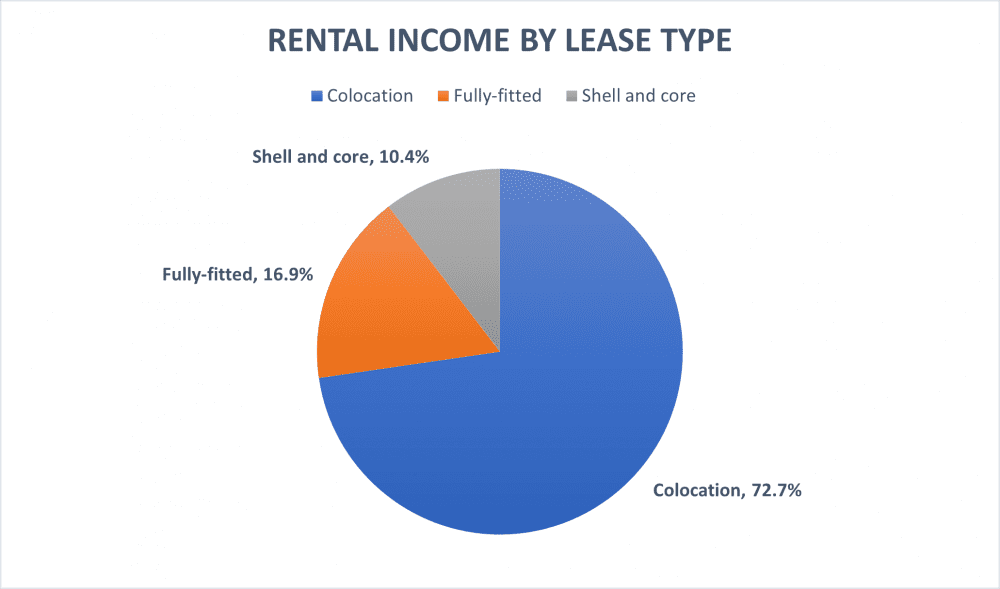

Its gearing ratio increased from 30.7% in 2019 to 36.2% in 2020 because additional bank loans were borrowed to fund the acquisitions. The figure is still below its internal gearing cap of 40%. Around three quarters of the REIT’s revenue in 2020 came from colocation data centres. The majority of the colocation data centres are located in Singapore.

2. The management undertook a number of asset enhancement initiatives (AEIs) in 2020 to further increase the REIT’s DPU. These AEIs include the fit-out works at Keppel DC Singapore 5, and energy efficiency and power capacity works at Keppel DC Dublin 1. This increased their occupancy rates for Keppel DC Singapore 5 and Keppel DC Dublin 1 from 84.2% and 65.7% in 2019 to 100% and 81.2% in 2020 respectively.

In Q1 2021, fit-out works at DC1 were also completed while some unutilised space at Keppel DC Dublin 2 was converted into a data hall for a client. DC1 is fully leased to 1-Net Singapore via a triple-net lease. The REIT’s portfolio occupancy stood at 97.8% in 2020 while its long weighted average lease expiry of 6.8 years gives unitholders strong income stability.

3. The leases of Keppel DC Singapore 1, Keppel DC Singapore 2, and Keppel DC Singapore 3 will expire by 2025, 2021, and 2022 respectively. The REIT has the right to renew all the leases by another 30 years by paying approximately S$15 million as the total land premium to JTC Corporation. It has exercised its option to renew the leases of the latter two assets.

4. In Australia, the development of Intellicentre 3 East Data Centre in Sydney is ongoing and will be completed in 1H 2021. Together with Intellicentre 2 Data Centre, this data centre will be leased to Macquarie Data Centres via a 20-year triple-net lease upon completion.

5. A unitholder pointed out that the occupancy rate of Basis Bay Data Centre in Cyberjaya, Malaysia stood at 63.1% in 2020; in fact, its occupancy rate has been low since 2017. The management answered that the data centre only comprised 0.8% of the REIT’s total assets under management. The utilisation rate of data centres in Cyberjaya averaged at 79% in 2020 because of recent political changes and competition from neighbouring countries. While the management strives to secure new tenants for the data centre, they are open to evaluating any potential divestment opportunities.

6. The Singapore government’s moratorium on new data centres in the country bodes well for the REIT’s existing data centres. Facebook also announced its recent partnership with Keppel, Telin, and XL Axiata to build two new subsea cables, namely Echo and Bifrost.The REIT stands to benefit from the enhanced connectivity and low latency from Singapore to the west coast of North America once the cables are completed. The cables also give the REIT a competitive edge compared to its regional peers.

7. As at March 2021, 6.9% of the leases by attributable lettable area will be due for renewal by the end of the year. The management is confident at getting them renewed as customer retention rates tend to be high for data centres because of the mission critical nature of the business. Competition is building up in the data centre market especially in the shell and core segments which do not require an operational track record. Together with its sponsor, Keppel Telecommunications & Transportation and related companies, the Keppel Group has years of expertise and experience in developing and operating data centres which will help the REIT fend off new entrants.

8. The management is not too worried about the fluctuations in the REIT’s earnings post-pandemic. They believe the pandemic has accelerated the adoption of technology and changed the way we learn, work, and shop. They expect the end-user global demand for data centres to maintain post-pandemic. On the other hand, they are proactively engaging with banks to refinance approximately one-tenth of its total debt that will be due by the end of 2021.

The fifth perspective

Keppel DC REIT enjoys industry tailwinds which will bolster its growth for the foreseeable future. The pandemic has accelerated the adoption of digital habits and the Southeast Asia data centre market is projected to grow 12.9% annually until 2024.

Due to the optimism surrounding the data centre industry, Keppel DC REIT trades at a premium. Based on its FY2020 DPU, its distribution yield is currently at 3.5%. Investors seeking a higher yield may prefer to wait for a better opportunity. At the same time, investors can also reasonably expect the REIT’s DPU to increase and improve their yield-on-cost over the long run.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

This company has been one of my best investments in the past 5 years. However, despite all the good news and great investment returns there’s some things bugging me. As time goes by, servers and data centre technology seems likely to improve significantly. More efficient technology may reduce demand for space in data centres? I’m wondering if there may be over-investment in data-centres, and that there’ll a lot of excess capacity in 5 to 7 years time? Of course, it’s also possible that demand growth will offset growth in capacity. Other than that I’m very happy with my investment (CAGR of 27.98% over just under 4.5 years).

Incidentally, I can thank the Fifth Person for teaching me how to evaluate REITs systematically. It’s one of the reasons I invested in Keppel DC REIT in the first place.

Hey Jonathan,

Congratulation! Always glad to know that you benefited from our sharing and you deserve the fantastic return since you did the research and took action after the course.

With regard to KDC, I think their leases are quite sticky, especially for tenants who’ve done the fit-out themselves. If there is an oversupply in the long run, the rent difference must be super attractive for the switch. For now, I don’t see a problem with oversupply.