Mapletree Industrial Trust (MIT) is an SGX-listed REIT with a diversified portfolio of 141 properties including 85 based in Singapore and 56 in North America. As of 31 March 2023, MIT’s total assets under management (AUM) remained stagnant at S$8.8 billion as compared to the year before.

Having reviewed MIT’s 2022 performance, I was curious to see how the REIT has performed thus far, and its plans to overcome current macro headwinds. To learn more, I attended MIT’s recent annual general meeting.

Here are eight things that I’ve learned from the 2023 Mapletree Industrial Trust AGM.

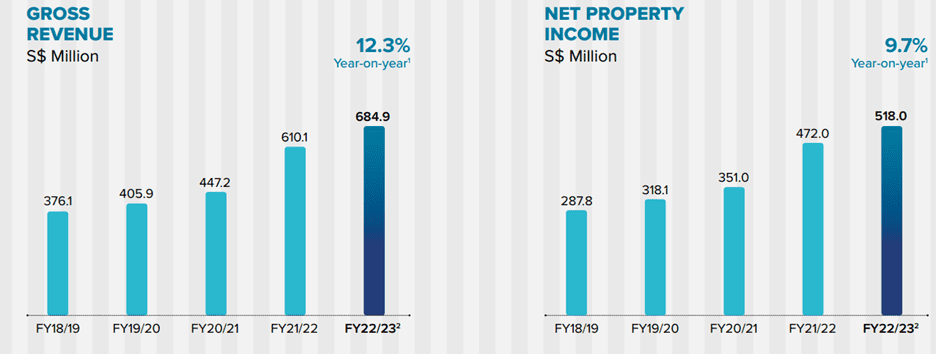

1. Gross revenue increased 12.3% year-on-year (y-o-y) to S$684.9 million and net property income grew 9.7% y-o-y to S$518.0 million. The main factor behind the growth was from the full-year contributions of the 29 data centers in the United States which were acquired in July 2021. Additionally, the growth in revenue from lease renewals, new leases, and augmented service charges within the Singapore portfolio also contributed to the overall increase.

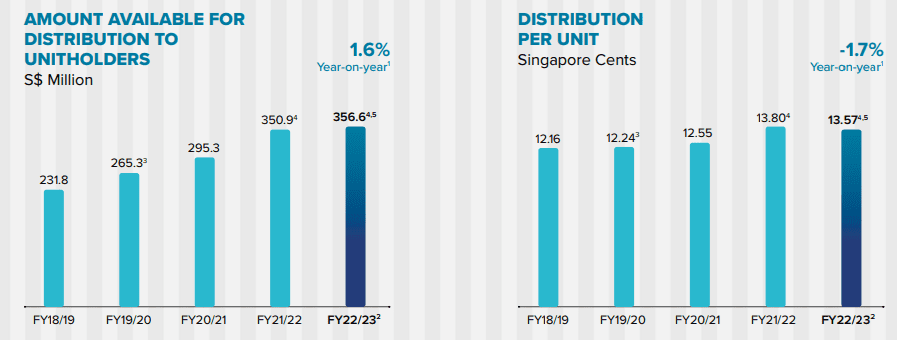

2. Distributable income to unitholders grew 1.6% y-o-y to S$356.6 million while distribution per unit declined 1.7% y-o-y to 13.57 cents. The slight growth in distributable income was due to increases in net property income that was partially offset by higher borrowing costs and management fees. On the other hand, negative DPU growth was attributed to the enlarged unit base with additional units issued under MIT’s distribution reinvestment plan.

Since MIT’s listing on 21 October 2010, unitholders would have gained a capital appreciation of 154.8% and distribution yield of 150.6%. This amounts to a total return of 305.4% despite the slow start in 2023.

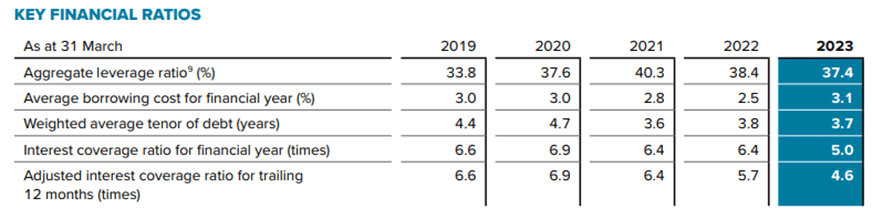

3. Aggregate leverage ratio fell from 38.4% in 2022 to 37.4% in 2023. MIT has a healthy interest coverage ratio of 4.6 times. As stated by the management, the REIT has a debt headroom of about S$685.5 million and S$1,140.9 million to the leverage ratios of 45% and 50% respectively.

4. Overall portfolio occupancy increased from 93.9% in FY21/22 to 95.5% in FY22/23. MIT hit an all-time high for its Singapore portfolio occupancy rate that rose from 93.8% in FY21/22 to 96.2% in FY22/23. This growth was attributed to higher occupancy levels at most property segments except for Hi-Tech buildings. MIT has also secured a higher passing rental rate for its Singapore portfolio that was driven by positive rental revision for renewal and new leases.

However, the average North American Portfolio occupancy rate fell from 94.2% in FY21/22 to 93.8% in FY22/23. The 0.4% decline was due to non-renewal of a lease at 2 Christie Heights Street, Leonia, New Jersey.

5. A unitholder expressed his concerns regarding MIT’s increasing concentration towards data centers and was curious about the risks involved as government regulation adjusts. Currently, MIT holds a 53.7% stake in data centers. That said, the management mentioned that it foresees an increase in allocation to around 65% in the near term. This is due to the attractiveness of the asset class and the opportunities available now. Management stated an upper bound of 75% allocation but did not mention the expected timeframe. However, despite MIT’s heavy allocation in data centers, it does not classify itself as a data center REIT. As a long-term goal, MIT strives towards greater diversification in other sectors and geographies.

While government regulations on data centers have gained more attention, the management views that regulation is expected, even for other asset classes. That said, the management recognises the increasing attention on data centers, perhaps due to the large energy output it generates, and reassures unitholders that greater diversification will reduce the risk stated.

6. A unitholder was curious about MIT’s BBB+ Fitch rating and whether it will improve moving forward. Since inception, MIT’s rating has remained consistent. When compared to other REITs, MIT has a similar rating, with some outliers with slightly better ratings. The management has mentioned that its Fitch rating is only useful when tapping into the bond market where fund managers from insurance companies have certain requirements.

Through engagements with Fitch Ratings, the management has mentioned that greater diversification in terms of asset class and geography will improve its rating. That said, it is not MIT’s top priority as it is still currently able to get loans at attractive rates.

7. Another unitholder expressed her concerns regarding a tenant (that contributes 3.2% of MIT’s gross rental income) that filed for bankruptcy, and the status of payments. The management gave an update that the tenant filed for bankruptcy in early June and the payment outstanding is still unpaid.

8. MIT remains bullish on the outlook of data centers in United States. From 2017 to 2022, the North American data center sector has experienced consistent expansion, maintaining an average annual growth rate of 12.3%. This expansion can be attributed to increasing demand from cloud service providers, the robust social media sector, and businesses in the midst of digital conversion. Moving forward, MIT believes that the growing prevalence of the Internet of Things (IoTs) among both consumers and enterprises will drive future growth of data centers in the United States. As such, there is a growing need for data centers to be situated closer to end users so as to ensure minimal latency.

The fifth perspective

Data centers will remain a core asset of MIT’s overall portfolio with the management aiming to increase investments in this asset class in the short-term future. With growing demand for such facilities and adoption of technological solutions by companies, I believe such a move will greatly benefit MIT for future growth. Given the stability and stickiness of data centers, consistent cash flows and high occupancy levels can be expected. That said, due to the current high interest rate environment, unitholders should expect slower growth and acquisitions by MIT.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

Nice summary. Looks like those key financial ratios are heading in the wrong direction. This company has been a great investment in the past it’s a bit disappointing to see that the adjusted interest coverage ratio has fallen below 5.0. It’s obviously critical they resolve the issue with the bankrupt tenant else I can see the share price taking a nasty hit along with our distributions.