Founded in 1965, Genting Malaysia celebrates its 60th anniversary in 2025. Some of the well-known integrated resorts owned by the company include Resorts World Genting in Malaysia, Resorts World New York City, Resorts World Catskills, and Resorts World Hudson Valley in the US, as well as Resorts World Bimini in the Bahamas.

The company achieved growth across its businesses worldwide in 2024. However, its share price hit a two-decade low in April 2025. Here are 10 things I learned from the 2025 Genting Malaysia AGM.

1. Revenue increased 7.1% to RM10.9 billion, driven by business volume growth worldwide. While revenue from VIP and mass market segments is typically evenly split, the casino derived 56% of its revenue from VIPs in 2024. However, net profit decreased 42.5% year-on-year to RM251.2 million in 2024. This decline was primarily due to higher sales and services tax in Malaysia, higher operating, payroll, and finance expenses, a one-off fixed asset write-off of RM217 million, and the absence of a significant net gain on disposal totalling RM180 million recorded in 2023. Dividend per share decreased from 15 sen in 2024 to 10 sen in 2025.

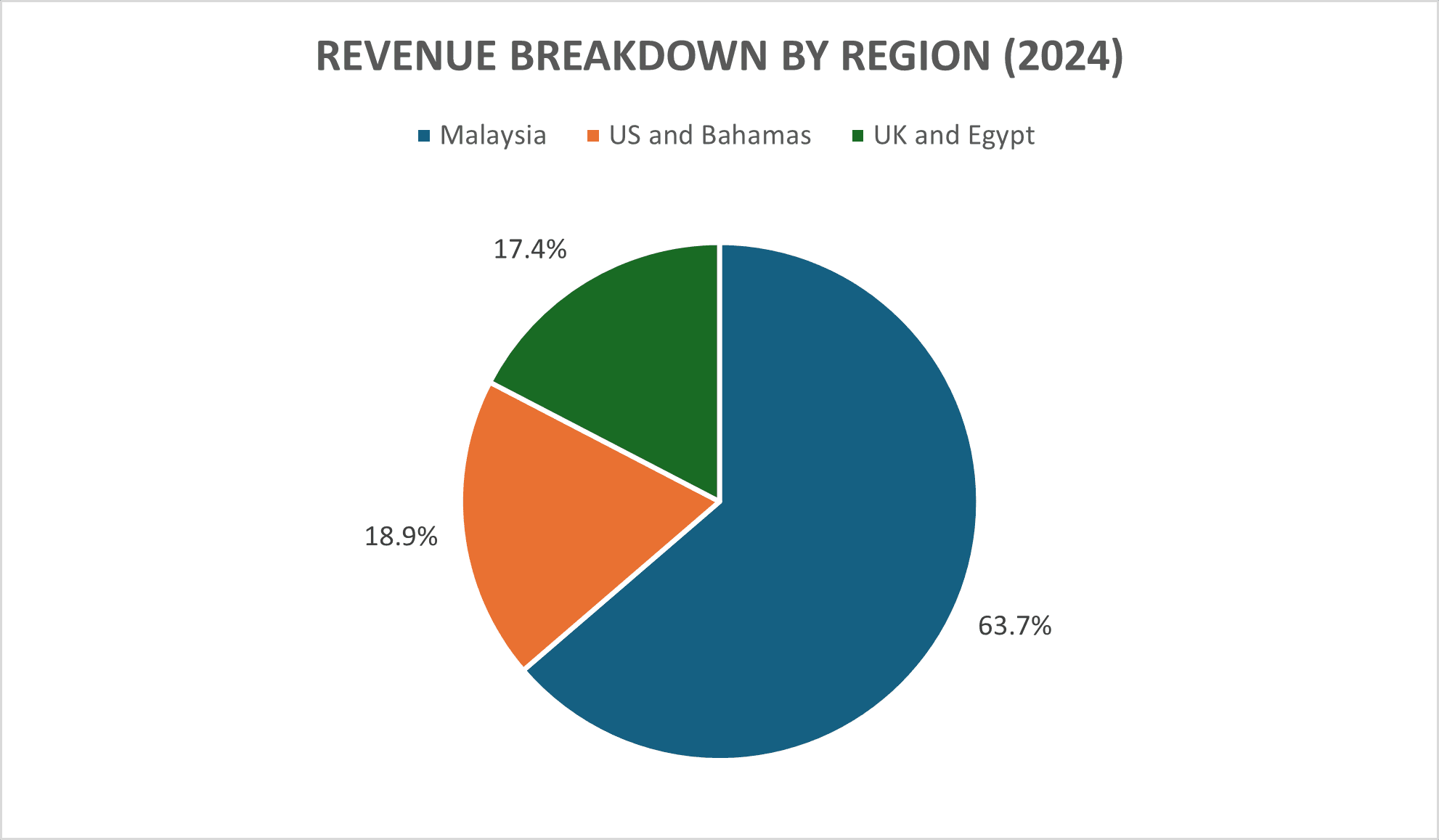

2. In 2024, the company obtained 63.7% of its revenue (RM7.0 billion) from Malaysia alone. A significant portion of this revenue came from Resorts World Genting, which increased 6% year-on-year to RM6.8 billion. The hilltop resort received 28.1 million visitors in 2024, an increase of 3.2 million from 2023. Notably, tourists from China and India dominated the visitor profile. The hotels were almost fully occupied with an occupancy rate of 99% in 2024. Its average room rate improved from RM221 in 2023 to RM232 in 2024. The room inventory of the resort stood at 10,500 in 2024. The resort will be adding more rooms to its five-star Crockfords Hotel to augment its non-gaming revenue.

There are quite a number of future mixed-use developments including Tropicana WindCity and King’s Park along the main road to the hilltop that may affect the demand of its retail, F&B, accommodation offerings. On the flip side, given that hotels at Resorts World Genting were almost fully occupied last year, these new offerings by third parties may also drive further market growth and benefit the company.

3. Although gaming revenue in 2024 constituted 72.1% of the company’s overall revenue, the company continues to position Resorts World Genting as an integrated entertainment destination. The company has renovated part of its casino and is expanding its premium gaming space. It also continues to hold regular events and concerts as well as relies on its indoor and outdoor theme parks, Skytropolis Indoor Theme Park and Genting SkyWorlds Theme Park, to draw footfall to the resort.

The outdoor theme park has been open since 2022. As mentioned by the management, a theme park typically has a long gestation period and needs between eight to 10 years to recoup its initial investment. The outdoor theme park also augments the offerings of the resort to boost its income.

As highlighted by a shareholder, RM182.2 million worth of construction in progress was written off. The management explained the write off was related to the structure and assets of a ride in its outdoor theme park that could not be economically developed after the bankruptcy of a vendor following the COVID-19 pandemic. Deputy chairman and chief executive Tan Sri Lim Kok Thay reassured shareholders that the investment in its outdoor theme park is part of the Genting Integrated Tourism Plan and has been substantially recovered through tax incentives, which have been fully utilised.

Despite the drop in the number of tickets sold for both its indoor and outdoor theme parks from 2.3 million in 2023 to 2.0 million in 2024, the management clarified that overall visitation actually increased. One possible explanation for this discrepancy is that fewer pay-per-ride tickets were sold in 2024. In the first few months of 2025, the theme park actually witnessed at least 20% growth in visitation which is a positive sign.

4. Lim expressed confidence in the future of Resorts World Genting and acknowledged the potential competition arising from regional peers from Singapore and Macau. The company is interested in pursuing the opportunity to develop a casino in Thailand and is closely monitoring the legislative process and changes to the entertainment complex bill. He also mentioned that Genting Malaysia is undervalued. He does not see any governance issues with the company, although it may be portrayed differently by the press.

5. In May 2025, Genting Malaysia acquired the remaining 51% interest in Empire Resorts Inc for US$41 million from its substantial shareholder, Kien Huat Realty III Ltd. This acquisition was viewed as dilutive and ‘value-destroying‘ by some analysts. Empire Resorts has been a loss-making entity for over two decades. Genting Malaysia first invested in the company in 2019, acquiring a 49% stake for US$159.7 million from its substantial shareholder. This stark difference in implied valuation for almost equal stakes in just six years drew eyebrows from the investment community.

Specific and recurring concerns about corporate governance related to the way the substantial shareholder has injected and transferred assets (Empire Resorts) into Genting Malaysia have been raised. These approaches were widely seen as financial aid especially during the pandemic rather than genuine investments. There is no clear path for the company to achieve profitability.

In the past, the strategy of incrementally acquiring stakes and injecting capital into Empire Resorts enabled the company to avoid seeking broader minority shareholder approval at a general meeting, as individual transactions remained below the required thresholds.

The management mentioned that the initial structure was to preserve Empire’s tax losses, and full control was acquired later when this tax issue was resolved. The management did not mention whether all of Empire’s historical non-operating losses could be used to offset future taxable profits (due to regulation limitations). However, by taking full control, they have improved their ability to utilise those non-operating losses within their U.S. consolidated tax group, making them a much more valuable tax asset than they were under the previous ownership structure.

Empire Resorts also owed US$39.7 million to the substantial shareholder. Post acquisition, the inter-company loan was assigned to Genting Malaysia rather than forgone by Kien Huat as phrased by the management and would have been factored into the negotiation of the acquisition.

6. The company is bidding for a full-scale casino licence in Downstate New York. There are at least eight potential contenders including MGM Resorts International. The development is anticipated to be undertaken in phases and funded using readily available USD debt.

The management implied that any cannibalisation will be offset by the overall market growth and synergy benefits, leading to a net positive for the group. A trend was observed in Macau and Singapore where increased supply stimulated demand. The gaming market in the New York state is expected to become one of the largest worldwide after Las Vegas with at least an estimated gross gaming revenue of US$9 billion according to president and chief executive Dato’ Sri Lee Choong Yan. Currently, the company owns 52% and 40% of the gaming market share in Downstate and the entire New York respectively.

It is worth noting that Resorts World Catskills (which offers table games, slot machines, and a mobile sports betting platform) is about one to two hours’ drive from Resorts World Hudson Valley and Resorts World New York City (both of which offer slot machines, video lottery terminals, and electronic table games). It is difficult to achieve zero cannibalisation when these gaming properties are in close geographic proximity. Some degree of internal competition will likely occur, even if the overall market pie grows. Further, the upcoming full-scale casino licences (up to three) in Downstate New York will intensify the competitive pressure. There is also stiff competition from casinos in neighbouring states like Connecticut, New Jersey, and Pennsylvania.

7. The management is comfortable with the company’s overall debt position despite high gearing following the acquisition of the remaining stake in Empire Resorts. Its existing cash and steady cash flow are sufficient to service its debt obligations. It aims to slowly pare down its debt in Malaysia and refinance its debt in the US with better rates (with no debt in the UK). The management can also sell assets, including its land in Miami, to service its debt but is in no hurry to do so, preferring to await the optimal price (potentially above US$1 billion).

8. The management is confident that land-based casinos remain relevant despite competition from online gambling, as evidenced by casino visitation, for instance in the UK. Casinos offer a different experience that cannot be entirely replicated by online gambling.

Despite recording higher revenue and gaming market shares, its UK operations were affected by higher payroll costs after securing a new contract with the labour union. The management is also optimistic about the proposed legislative changes to increase the number of slot machines per facility from 20 to 80. The company also recently acquired Aspers Stratford in London to expand its market share in the region.

9. The management continues to its efforts to turn around operations in the Bahamas by welcoming more cruises to Resorts World Bimini. As more cruise passengers disembark at the resorts, the aim is to reduce losses and achieve profitability in the future. The resort’s LBITDA narrowed from US$21 million in 2023 to US$7 million in 2024. Lee views the lawsuit filed by its joint venture partner as a shareholder dispute, rather than fraud as alleged by the partner.

10. The company has been providing finance and partnering with the Mashpee Wampanoag Tribe to construct a resort casino in Massachusetts. Since January 2025, the tribe has been given the green light to operate 50 slot machines and will be adding more by this year. The business has been providing returns and achieving positive cash flow.

The fifth perspective

Genting Malaysia faces a mixed outlook. Its domestic cornerstone, Resorts World Genting, remains a strong earner due to its monopoly and inelastic demand in Malaysia despite rising regional competition. However, international headwinds, including a weak global economy impacting travel demand, are significant. The persistent losses from overseas operations, particularly Empire Resorts, continue to be a drag on the group’s overall profitability. Despite strategic long-term plays, the success of these international ventures, and their ability to outweigh current financial burdens, remains to be seen.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

Got door gift or not?

No door gifts this year