Mapletree Industrial Trust (MIT) is an SGX-listed REIT with a diversified portfolio of 141 properties including 83 based in Singapore, 56 in North America and 2 based in Japan. As of 31 March 2025, MIT’s total assets under management (AUM) stands at S$9.1 billion with more than 2,000 tenants and 25.1 million square feet in net lettable area.

I was curious to see how MIT had performed over the past financial year and its plans to overcome current macroeconomic headwinds. To learn more, I attended MIT’s recent annual general meeting. Here are 10 things that I’ve learned from the 2025 Mapletree Industrial Trust AGM.

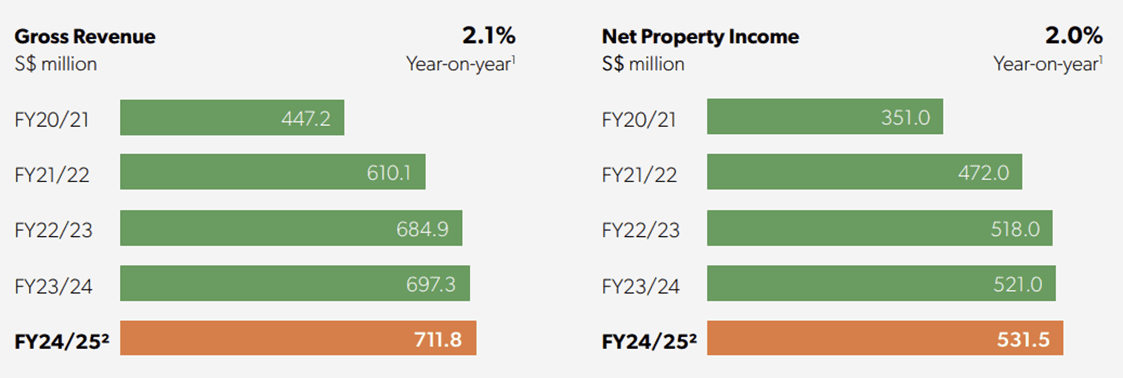

1. MIT posted stable top-line and bottom-line growth. Gross revenue rose 2.1% year-on-year to S$711.8 million, and net property income increased 2.0% to S$531.5 million, driven by contributions from the Osaka and Tokyo data centres and new leases across Singapore properties.

This growth came despite headwinds such as the divestment of the Tanglin Halt Cluster and lease expirations in the North American portfolio. Management attributed the steady results to disciplined execution and a focus on high-quality tenants in resilient sectors like data centres.

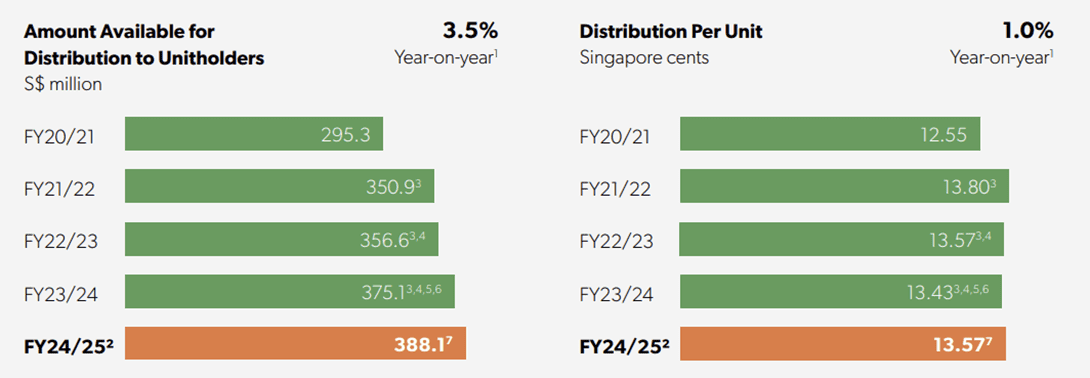

2. MIT’s distribution income and distribution per unit (DPU) rose compared to last financial year. MIT’s amount available for distribution to unit holders increased 3.5% to S$388.1 million, while DPU rose 1.0% to 13.57 cents maintaining payout levels despite a rising interest rate environment. Since MIT’s listing on 21 October 2010, unitholders would have gained a capital appreciation of 125.8% and distribution yield of 179.6%. This amounts to a total return of 305.4%. MIT’s distribution yield stands at 6.5% as of 31 March 2025 which is higher than the FTSE ST REITs Index at 5.2%.

This included the distribution of S$13.4 million in net divestment gains and S$1.9 million in net compensation from a redevelopment project. The REIT’s DRP (Distribution Reinvestment Plan) which allows unitholders to receive distributions in the form of new units instead of cash also helped preserve cash, reinforcing its balance sheet for future growth.

3. MIT’s gearing ratio increased slightly, but the REIT still maintains healthy leverage. Its aggregate leverage rose to 40.1% from 38.7% the previous year, remaining comfortably below the 50% regulatory ceiling and leaving ample debt headroom. However, the REIT’s weighted average debt tenor shortened from 3.8 years to 3.2 years as of 31 March 2025, meaning a larger portion of borrowings will need to be refinanced sooner. This could expose MIT to refinancing risks or higher interest costs if market conditions stay tight. As such, MIT will need to carefully manage its refinancing strategy to preserve cost efficiency and financial flexibility.

MIT’s interest coverage ratio held steady at 4.3 times, reflecting healthy earnings despite an elevated interest rate environment. Average borrowing cost declined marginally to 3.1%, aided by debt repayment from divestment proceeds and forex hedging strategies. By maintaining a prudent capital structure, MIT is able to balance growth initiatives with financial stability, even in a higher interest rate environment allowing the REIT to capitalise on any opportunities in the market.

4. MIT has been leveraging strategic divestments and acquisitions to optimise portfolio. MIT divested a data centre in Georgia at an 18.6% premium to market valuation, and three properties in Singapore at a 22.1% premium to original cost. These capital recycling moves help MIT unlock value, streamline its portfolio, and free up cash for reinvestment in higher-yielding opportunities. Notably, these divestments also helped fund debt repayment and support the REIT’s disciplined capital structure.

In Japan, MIT completed the final phase of fitting-out works for the Osaka Data Centre, which is now 100% occupied with a WALE of 17.6 years. It also acquired a freehold mixed-use facility in Tokyo fully leased to a top-tier Japanese conglomerate with redevelopment potential. These long-term, stable assets add to the REIT’s geographic diversification and strengthen its recurring income base.

5. MIT’s portfolio occupancy dipped slightly in 2025, but rental reversion remained strong. Overall occupancy declined to 92.1% from 92.6% a year earlier, mainly due to non-renewals in its North American data centre portfolio. While this modest drop reflects softer leasing activity in certain U.S. submarkets, management has proactively backfilled part of the space and remains confident in the region’s long-term fundamentals.

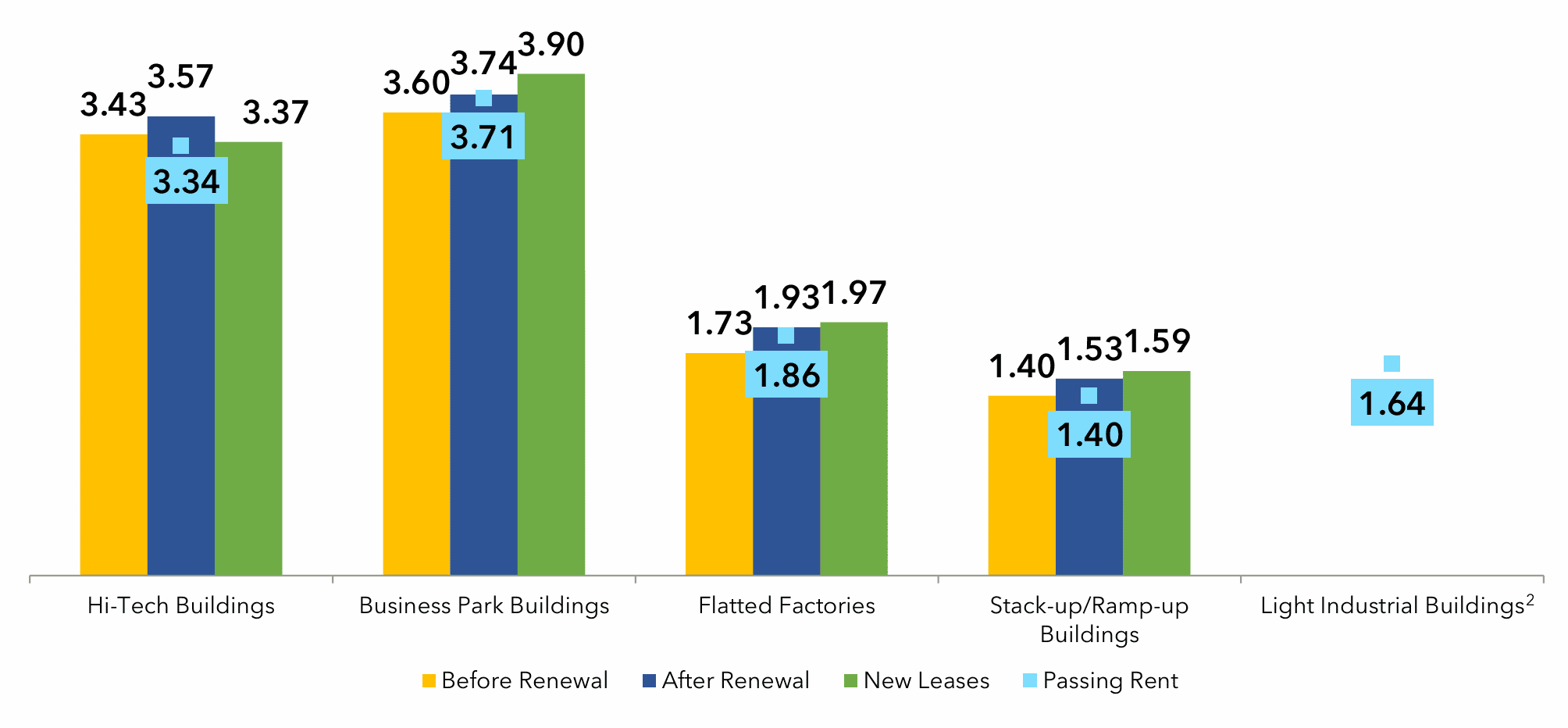

On the other hand, the Singapore portfolio continued to deliver strong performance, with occupancy holding firm at 93.2% and a healthy weighted average rental reversion of 9.2%, up from 6.7% in the previous year. This uplift was driven by renewed demand for high-specification industrial space, underpinned by Singapore’s position as a key logistics and tech hub in Asia.

All property segments in Singapore achieved positive rental reversions between 3.9% and 26.1%. This highlights the REIT’s ability to capture upside through active lease management and strong tenant retention in a supply-constrained market.

6. MIT continues to strengthen its portfolio through proactive lease management and strategic asset optimisation across all markets. As of 31 March 2025, the REIT maintained a stable overall WALE (weighted average lease expiry) of 4.4 years, with improvements seen in North America (from 5.5 to 6.3 years), while Singapore and Japan portfolios held steady at 2.7 and 14.5 years, respectively. The well-spread lease expiry profile ensures that no more than 20.2% of gross rental income is due for renewal in any given year, reducing income volatility and enhancing predictability of cash flows.

8. During the AGM, a unitholder raised a question about how MIT plans to meet the increasing power and infrastructure demands driven by AI technologies. Management responded that it has been proactively conducting power feasibility studies across its existing data centre portfolio to assess capacity and future-proof its assets. These studies help identify opportunities to upgrade or enhance facilities to support the intensifying power density requirements of AI workloads.

9. Another unitholder asked about expanding beyond Singapore data centres into the United States. The management highlighted that expanding into the U.S. offers diversification benefits and access to established, high-demand hyperscale markets. Unitholders also expressed strong interest in MIT entering the hyperscale data centre space, which continues to see rapid global growth. Management acknowledged this and pointed to the Osaka hyperscale data centre as a concrete example of its strategy to pursue such opportunities.

10. The management reaffirmed its confidence in the data centre sector, noting that as of March 2025, data centres made up 55.6% of MIT’s total portfolio value, up from 53.7% the year before. This includes data centers in North America (45.6%), Japan (6.8%), and Singapore (3.2%), positioning MIT as one of the most data centre-focused REITs in the region.

With sustained demand from cloud service providers, hyperscalers, and the broader digital economy, MIT remains strategically committed to growing this asset class while maintaining a disciplined and diversified investment approach.

The fifth perspective

Mapletree Industrial Trust’s 2025 AGM showcased a REIT that is not standing still. Despite global headwinds and a volatile interest rate environment, MIT continues to demonstrate strength through disciplined capital management, strategic divestments, and a clear focus on quality tenants and resilient asset classes. Its active lease management and prudent reinvestment strategy reflect a management team that is proactive in enhancing the value of the REIT through its active acquisitions and divestment strategies.

The growing emphasis on data centres, supported by geographical diversification into Japan and North America, signals MIT’s readiness to meet the demands of a rapidly digitalising world riding on the growing trend of AI and hyperscalers. At the same time, its measured approach to expansion, tenant retention, and portfolio recycling positions the REIT for consistent performance. With a solid financial foundation and long-term vision, MIT positions itself a as a REIT that can deliver stable distributions and capital appreciation.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

Jacob, Please check Fifthperson SREIT listing has NTT DC REIT missing 😉