Nestlé (Malaysia) Berhad is the largest fast-moving consumer goods company in Malaysia, exporting its products to over 50 countries. Within the Nestlé group, its Malaysian operations serve as the largest halal manufacturing and export hub.

In recent years, the company has faced several business headwinds, including weaker consumer sentiment driven by the ongoing Hamas-Israel conflict and inflationary pressures. Its share price fell to a decade low of RM62.24 in March 2025. I had expected an annual general meeting filled with disgruntled shareholders. Instead, the management earned their trust by reaffirming the company’s ability to perform well and maintain strong customer loyalty.

Here are seven things I learned from the 2025 Nestlé Malaysia AGM.

1. Revenue declined by 11.7% year-on-year to RM6.2 billion in 2024, largely due to a 15.7% drop in domestic sales. In Malaysia, weaker consumer sentiment, impacted by the Hamas-Israel conflict and inflationary pressures, led some consumers to switch to more affordable alternatives offered by Nestlé Malaysia’s competitors. On a positive note, the export segment performed well, recording a 4.9% year-on-year increase in revenue in 2024. CEO Juan Aranols explained to the Minority Shareholder Watch Group that exports typically contribute around one-fifth of the company’s total revenue, with ASEAN and Oceanian countries being the key markets.

2. Net profit declined 37.0% year-on-year to RM415.6 million in 2024. The decline was due to lower revenue and higher raw material prices as the company did not pass on the surging prices of cocoa and coffee beans fully to consumers. To diversify its supply chain and reduce its exposure to foreign currency risk, the company sources more raw materials like cocoa locally from Malaysia. Its diverse product portfolio also helps cushion the impact when the costs of several of its key ingredients increase significantly. The company continues to improve its operational efficiency and agility to reduce administrative costs with the use of digitalisation and analytics. Dividend per share dropped from RM2.68 in 2023 to RM1.79 in 2024.

3. Overall, Nestlé Malaysia’s business remains resilient despite the impacts of COVID-19 and the recent consumer boycott, achieving its third-highest annual sales in 2024, behind only 2023 and 2022. Management remains highly optimistic and confident that the company is on track for a full recovery in 2025 and beyond. Their focus continues to be on long-term growth rather than short-term quarterly fluctuations.

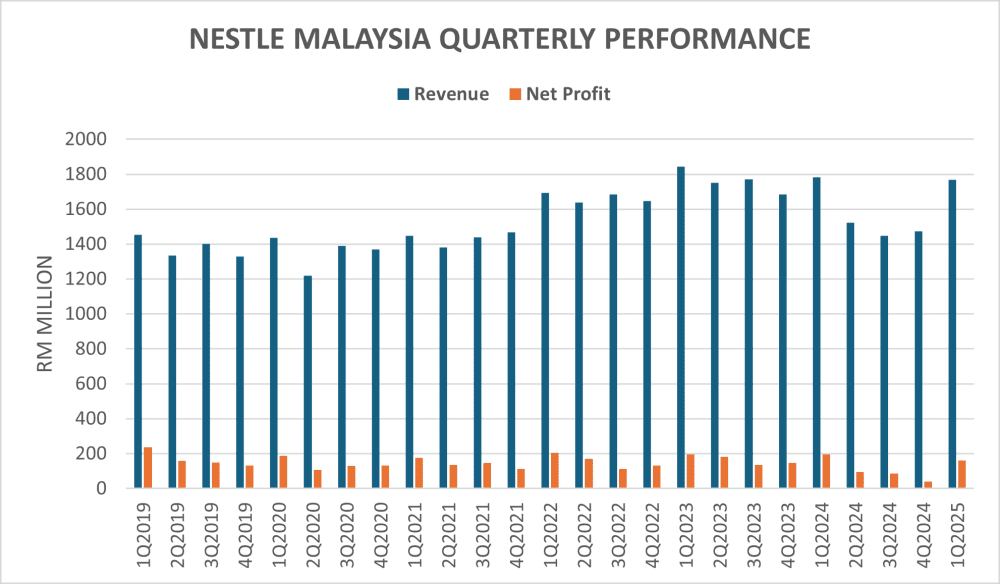

Based on the chart above, Nestlé Malaysia is traditionally stronger in the first quarter. Its quarterly performance in the latest quarter may not be the strongest overall in the past six years but it has certainly rebounded significantly from the dismal Q4 2024 performance. In Q1 2025, revenue and net profit declined 0.8% and 17.5% year-on-year to RM1.8 billion and RM161.3 million respectively as the company increased its marketing expenditure to engage with consumers, regulators, and the community. The previous corresponding quarter was largely shielded from the impact of high raw material prices. Total debt has also reduced from RM1.1 billion in Q4 2024 to RM851.6 million in Q1 2025.

4. The company is committed to investing in Malaysia’s growth for the long term. Capital expenditure amounted to RM1.5 billion in the past five years and stood at RM280.0 million in 2024. Specific returns on investments were not shared but they were well above the cost of capitals according to the CEO.

The company is building a logistics hub in Port Klang at RM250 million. The hub will be ready for commercial uses by Q1 2026. The location of the hub is ideal of import and export as well as allows the company to save transportation costs and time.

5. The company’s products continue to be popular among domestic consumers. MILO, NESCAFE, and MAGGI were the leading brands in their respective FMCG categories while KITKAT came in second despite market pressure. Nestlé ice-cream and NESTLÉ OMEGA PLUS co-led their respective top spots with competitors. Aranols believes that the company’s market share has been improving in the recent months including products of Wyeth Nutrition Malaysia and is confident that the company can further increase and reinforce their leadership in the industry.

6. Impairment loss on property, plant, and equipment dropped from RM90.6 million in 2023 to RM36.3 million in 2024. Aranols explained that the impairment was part of the company’s annual routine exercise to make provisions for inefficient equipment related to the plant-based business. The company’s plant-based business did not pick up as fast as it was expected. The management decided to focus on their resources on other businesses with more growth potential instead.

7. The recent pipeline explosion in Putra Heights did not impact the company’s manufacturing operations. The plant was undergoing scheduled maintenance at the time of the incident. Swift action was taken to ensure continued production by temporarily transitioning to diesel-powered boilers, allowing factory facilities to operate without disruption.

Nestlé Malaysia is also not impacted much by the sugar tax in Malaysia as the sugar levels of many of its products are below the taxable threshold.

The fifth perspective

Looking ahead to 2025, the company expresses confidence in its ability to return to healthy growth by the first half through effective marketing strategies and targeted product innovations, underpinned by a strong understanding of local consumer sentiment and market dynamics.

While acknowledging the challenging and complex business landscape, the management continues to exercise their prudent financial management and leverage on centralized procurement model to manage their operations. The management is also aware of potential business risks like the indirect impacts from US tariffs as they could affect the supply chain as well as weaken the macroeconomic environment and consumer sentiment.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »