As Singapore’s largest REIT for commercial real estate, CapitaLand Integrated Commercial Trust (CICT) owns a diversified portfolio of high-quality retail and office assets, with a strong focus on Singapore. As of 31 December 2025, its portfolio spans Singapore, Frankfurt, and Sydney, with a total property value exceeding S$27 billion.

I attended CICT’s 2026 annual general meeting (AGM) to better understand its performance over the past year and how management is navigating a more uncertain macroeconomic environment.

Here are 10 key takeaways from the AGM.

1. Development pipeline in Hougang introduces a new growth engine. CICT is expanding into development through the Hougang Central integrated project, with a total development cost of approximately S$1.1 billion and an expected yield on cost of just over 5%. This marks a shift beyond traditional acquisition-led growth, allowing the REIT to generate value through development margins.

The project is strategically located in the heart of Hougang and will be directly integrated with a MRT station and bus interchange, similar to CICT’s existing suburban mall model. This transport connectivity is a key driver of footfall and supports long-term tenant demand. The development will primarily serve a large residential catchment area, reinforcing its positioning as a necessity-driven suburban retail asset.

CICT will own 100% of the commercial component of the development, with an estimated cost of around S$3,600 per square foot. The project is expected to be completed between 2030 and 2031 and will be financed through a combination of internal funds and external borrowings.

From a market perspective, Hougang appears relatively underserved, with only 2.8 square feet of private retail space per capita compared to the national average of 11.4 square feet. This suggests strong potential for demand absorption and long-term income generation once the development is completed.

However, such projects also introduce execution risk and require longer capital commitment cycles, meaning returns will only materialise over a longer horizon.

2. Strategic acquisitions continue to drive portfolio transformation. CICT’s performance in FY2025 was supported not only by operational improvements but also by active capital allocation. The REIT increased its stake in CapitaSpring while recycling capital through the divestment of non-core assets. This was further demonstrated by the announced sale of Asia Square Tower 2 and the acquisition of Paragon, reflecting a broader portfolio reconstitution strategy aimed at enhancing asset quality and long-term returns. These moves indicate that growth is increasingly driven by management’s capital allocation decisions rather than purely organic performance.

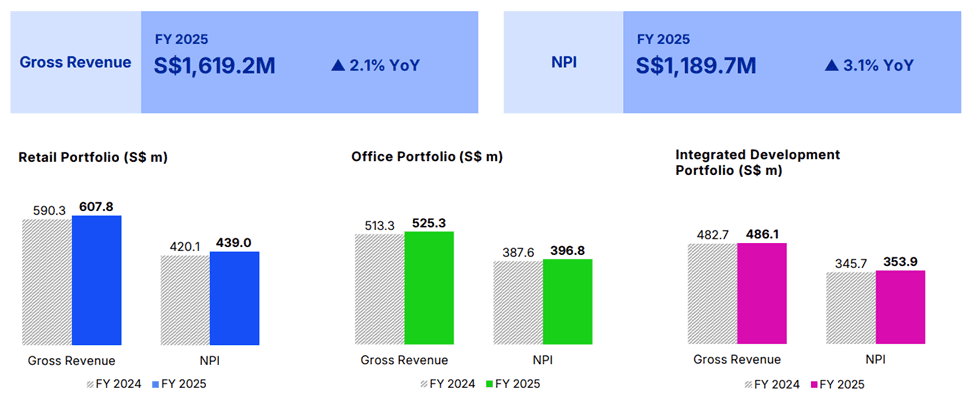

3. Financial growth supported by acquisitions and asset management. CICT delivered a strong set of financial results for FY2025, with growth supported by full-year contributions from ION Orchard, the step-up acquisition of CapitaSpring, and continued asset management initiatives.

Revenue and net property income improved as a result of both higher rental income and the addition of new assets. While acquisitions have been an important driver, underlying operating performance also continues to support earnings growth.

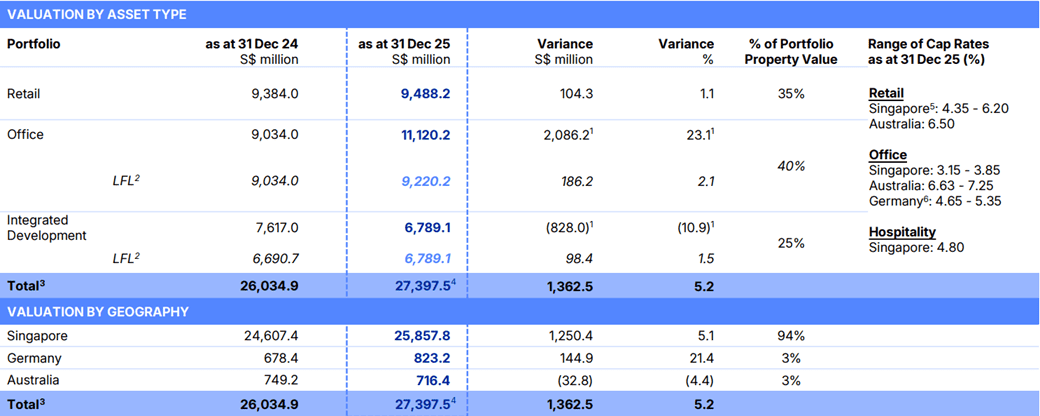

4. Portfolio valuation growth was driven by the strength of CICT’s Singapore-focused portfolio. CICT’s portfolio value increased by 5.2% to approximately S$27.4 billion, driven primarily by the step-up acquisition of CapitaSpring and the continued strength of its Singapore assets. This reinforces its positioning as a proxy for Singapore commercial real estate, with around 94% of the portfolio concentrated domestically.

The strong Singapore weighting provides stability, supported by resilient demand and limited supply in prime locations. However, valuation performance was not uniform across the portfolio. Management acknowledged that some overseas assets have underperformed relative to the domestic portfolio.

Australia has shown signs of recovery and has done well over the year, with resilient occupancy and improving leasing momentum, suggesting that the market may have reached its cyclical bottom. In contrast, Germany remains more challenging, although active asset management has helped to de-risk certain properties, such as securing a long-term lease with the European Central Bank.

This highlights that while overseas diversification provides potential upside, it also introduces greater exposure to market-specific risks and uneven performance across regions.

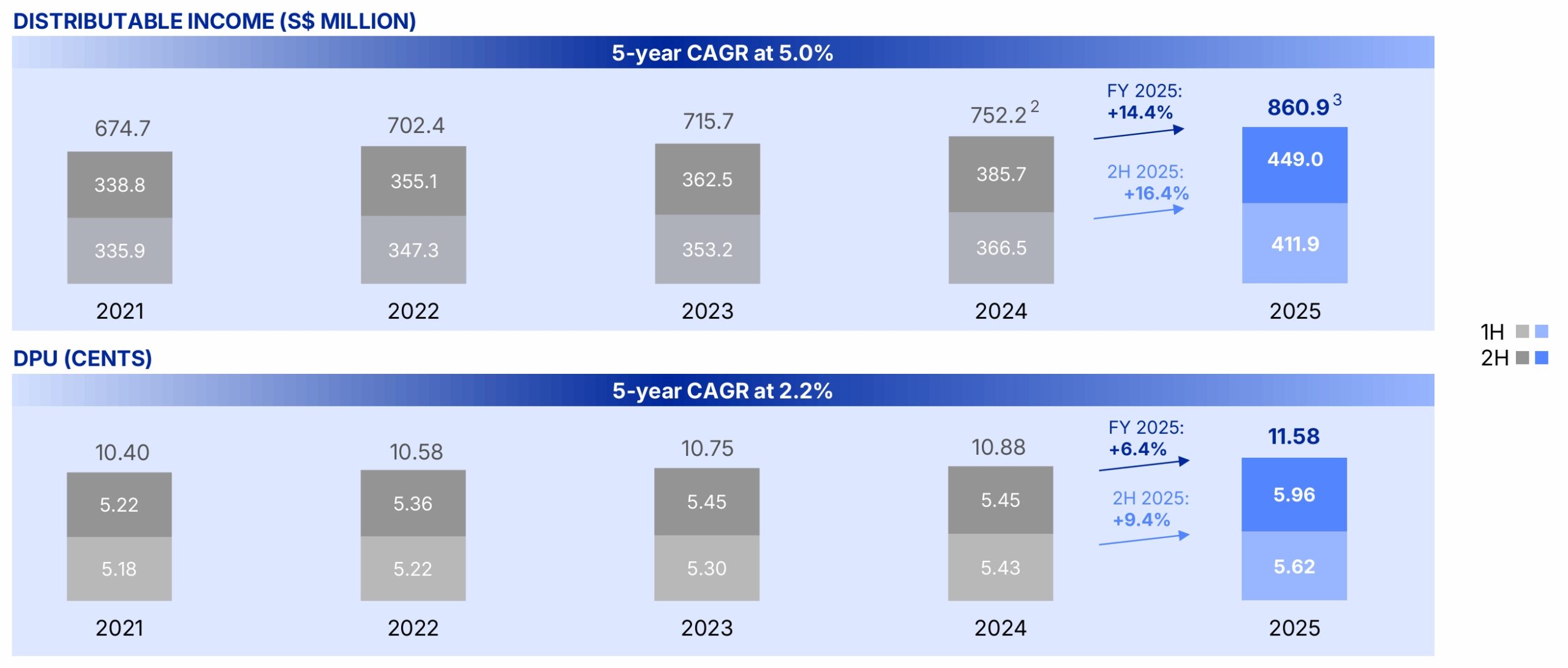

5. Distribution income and DPU show recovery, but long-term growth remains moderate. Distribution per unit (DPU) increased by 6.4% year-on-year to 11.58 cents, reflecting improved income contributions and cost discipline.

However, over a five-year period, DPU growth remains modest at around 2.17% on a compounded basis. While short-term performance has improved, long-term income growth remains gradual, and future growth will increasingly depend on acquisitions and development projects.

6. Capital management remains disciplined, with a well-managed debt profile. CICT continues to maintain a prudent balance sheet, with aggregate leverage at 38.6%, remaining comfortably within regulatory limits. This provides sufficient headroom to pursue acquisitions and development opportunities while maintaining financial stability.

In terms of borrowing strategy, CICT has adopted a conservative approach, with approximately 74% of its debt on fixed interest rates, helping to mitigate exposure to short-term interest rate volatility. The REIT also maintains a well-staggered debt maturity profile and has lowered its average cost of debt to 3.2%, reflecting strong credit standing and access to diversified funding sources.

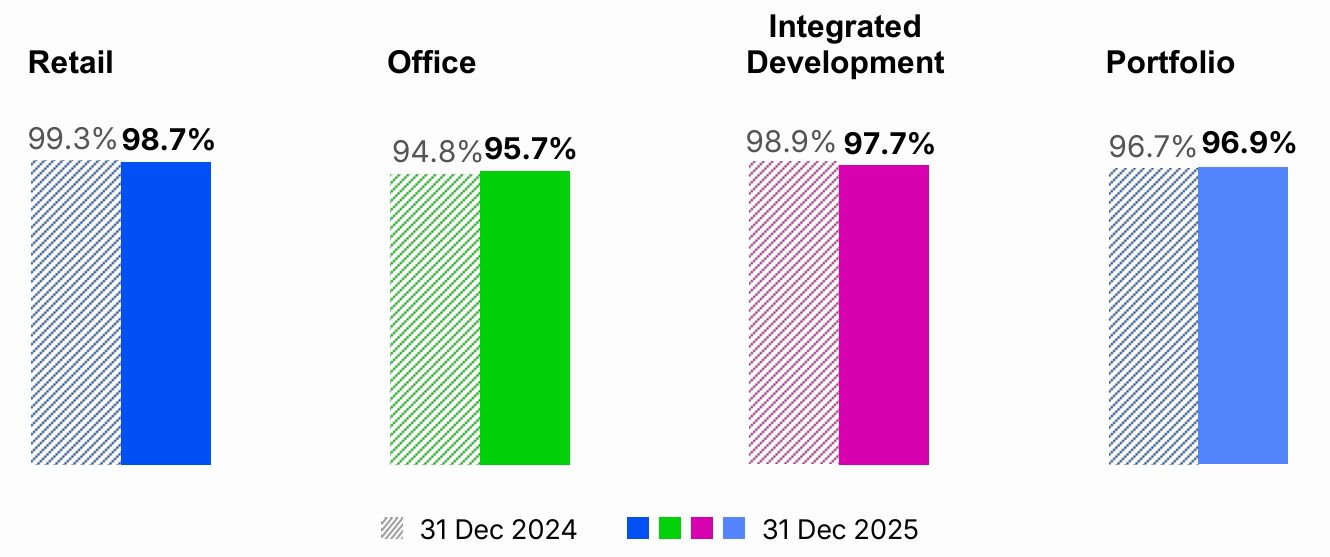

7. Occupancy remains high, but underlying asset-level volatility exists. Portfolio occupancy remained strong at 96.9%, reflecting stable demand across the portfolio. However, performance varies across asset classes, with office properties generally exhibiting lower occupancy levels compared to retail assets.

Retail assets benefit from diversified tenant mixes and strong footfall, particularly in locations integrated with transport nodes, allowing them to attract both local shoppers and tourists. In contrast, office occupancy is more affected by tenant movement and leasing dynamics.

Management highlighted that declines in certain office assets were largely due to tenant relocation or expansion needs, rather than structural weakness in demand. This suggests that while office occupancy may fluctuate in the short term, the overall portfolio remains stable due to the strength of its retail segment.

8. Geopolitical tensions introduce macro risks through inflation and interest rates. Management highlighted concerns surrounding geopolitical tensions, particularly the conflict involving the United States and Iran, and its potential impact on the broader economic environment. The primary transmission channel for these risks is through energy prices, as disruptions in global oil supply have led to higher fuel costs, which in turn feed into inflation.

For REITs such as CICT, this creates a double impact. Higher inflation may lead to persistently elevated interest rates, increasing borrowing costs and placing pressure on distributions. At the same time, higher energy and living costs can reduce consumer spending, which may affect tenant sales and rental sustainability. This highlights that while CICT’s fundamentals remain strong, its performance is still indirectly exposed to global macroeconomic conditions, particularly through interest rate and consumption channels.

9. A shareholder pointed out that rental reversions were around 6.6%, while tenant sales growth was only about 1%, and questioned whether such rental growth is sustainable given the weaker underlying tenant performance. Management acknowledged that rental reversions may not continue at the same elevated levels, explaining that recent strong rental growth was partly due to post-COVID recovery effects and pent-up demand. Going forward, they expect rental reversions to remain positive but moderate to mid-single digits. This highlights a potential mismatch between rental growth and tenant fundamentals, suggesting that future rental reversions may become more constrained if tenant sales do not improve.

10. A shareholder noted that NAV per unit has only increased modestly over several years, while borrowings have risen significantly, and questioned whether this truly represents value creation for unitholders. Management responded by emphasising that performance should be assessed based on total return, which includes both NAV growth and distributions paid to unitholders. They highlighted that, when dividends are taken into account, total returns are around 7%, and that CICT has performed relatively well compared to peers.

The fifth perspective

CICT continues to demonstrate strong operational resilience, supported by a high-quality portfolio, disciplined capital management, and a dominant position in Singapore’s commercial real estate market. However, the nature of its growth is evolving. While past performance was supported by favourable acquisitions and post-COVID recovery, future growth is likely to depend increasingly on larger, lower-yield acquisitions, development projects, and continued capital recycling.

At the same time, risks are becoming more pronounced. Interest rate uncertainty remains a key concern, as higher rates could increase borrowing costs and place pressure on distributions. In addition, the moderation of rental growth and the narrowing spread between acquisition and divestment yields suggest that the scope for value creation may become more constrained.

Overall, CICT remains a stable and well-managed REIT, but investors should pay closer attention to the quality of its growth and the execution of its capital allocation strategy, as these will play a more significant role in determining future returns.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »