DBS Group is a leading financial services group in Asia with a presence in 19 markets. Headquartered and listed in Singapore, DBS is in the three key Asian axes of growth: Greater China, Southeast Asia, and South Asia. As of 31 December 2025, DBS has total assets of SGD 897 billion.

The year 2025 marked a pivotal leadership change for DBS, with Tan Su Shan stepping in as Group CEO. As investors approached the AGM, they sought clarity on three key points: whether the bank could maintain its ROE target without the boost from high interest rates, if the capital return program announced the previous year was still on track, and what direction the new CEO would take strategically.

Curious about the bank’s future strategy, I attended its 2026 AGM and here are 10 things I learned:

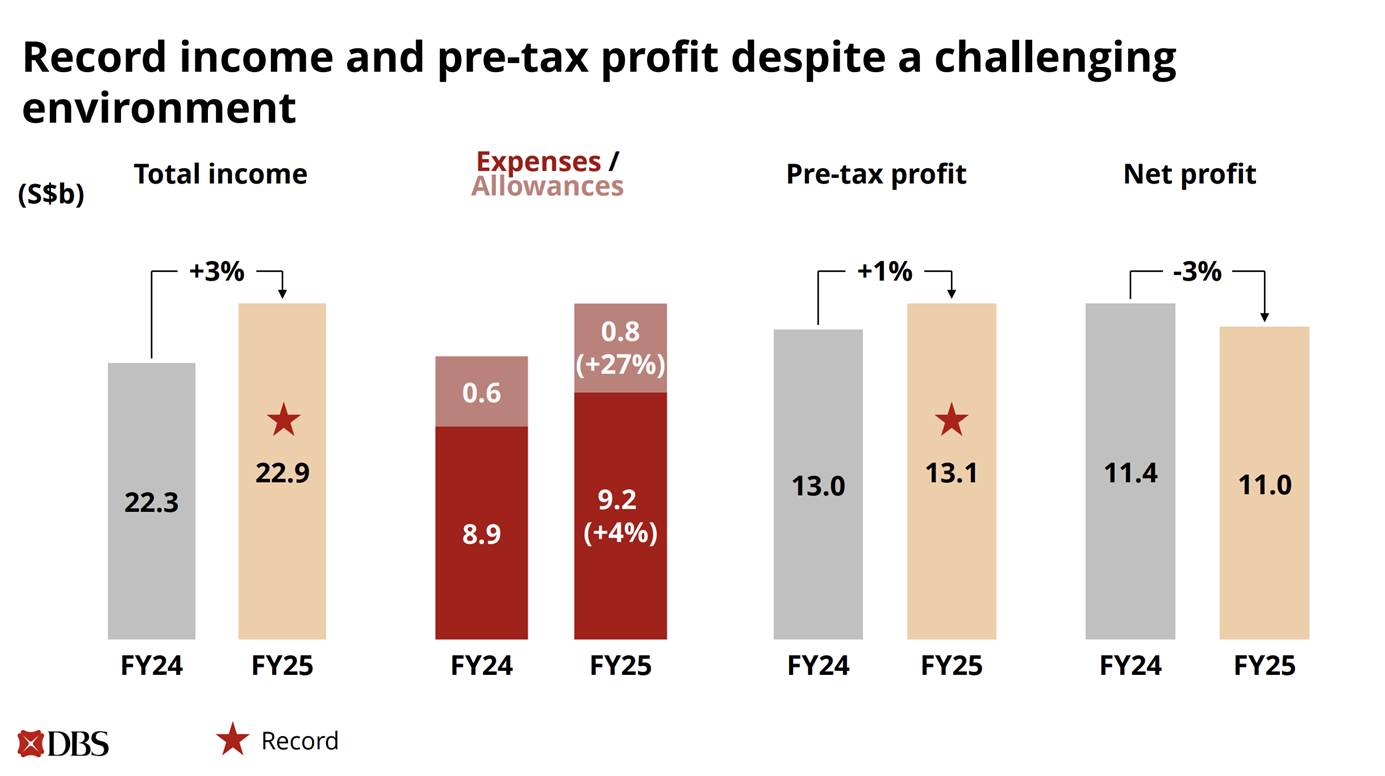

1. DBS posted record total income and profit before tax in 2025, despite one of its toughest operating years. CEO Tan Su Shan opened by acknowledging that 2025 presented one of the most challenging rate environments in recent years.

Despite the tough macroeconomic environment, DBS’s total income rose 3% to a new high of SGD 22.9 billion up from SGD 22.3 billion the year before, and profit before tax climbed 1% to a record SGD 13.1 billion. Net profit came in 3% lower at SGD 11.0 billion but management was direct that this decline had nothing to do with the business itself. It was entirely a function of the newly implemented 15% global minimum tax applied in Singapore from 2025. Stripping that out, the underlying earnings story was one of continued strength. The bank’s market capitalisation reached USD 124 billion (SGD 160 billion) at year-end, placing DBS among the top 25 banks globally.

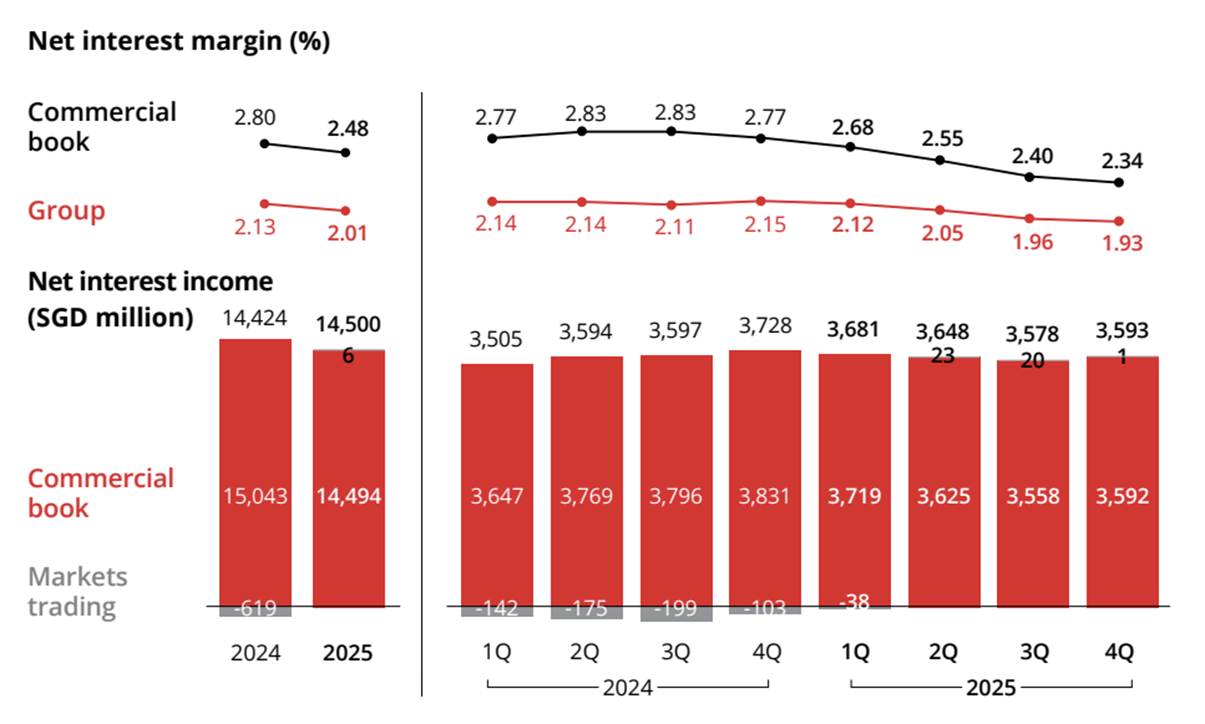

2. DBS’s net interest margin (NIM) decreased to 2.01%, but years of proactive hedging enabled DBS to stay agile and leverage fee income, maintaining its strategic strength. Management stated that over the past three to four years while rates were still high, DBS had systematically increased its fixed-rate asset book by SGD 70 billion to SGD 210 billion, representing roughly one-third of the commercial book.

This included fixed-rate mortgages, interest rate swaps and fixed income securities. The positioning reduced the bank’s sensitivity to rate movements significantly, and the outcome was a NIM decline of only 12 basis points to 2.01% for the full year a smaller compression than local peers. As a result, group net interest income still edged up slightly to a record SGD 14.5 billion despite the sizeable headwind. CEO highlighted that this was a deliberate result of balance sheet discipline executed years in advance.

Fee income and wealth management have become the primary growth engines for DBS With NIM structurally lower, non-interest income carried the income story in 2025, Net fee income rose 18% to a record SGD 4.90 billion from SGD 4.17 billion the year before.

Wealth management fees led the way, surging 29% to SGD 2.81 billion, underpinned by record net new money inflows of SGD 39 billion a higher run rate than in recent years. This drove AUM up 19% in constant-currency terms to SGD 488 billion, double the level of 2019 and with 58% now held in investment products. Treasury customer sales reached a new high of SGD 2.14 billion, while markets trading income rose 49% to SGD 1.37 billion, the highest since 2021.

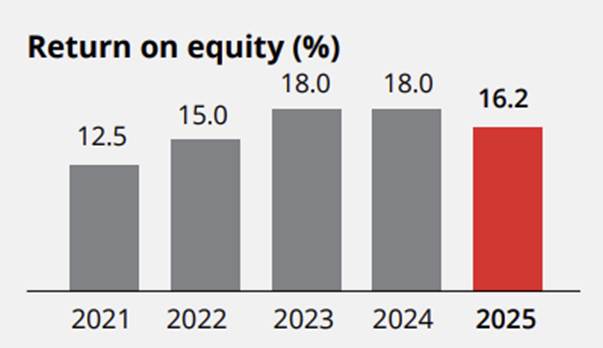

3. ROE of 16.2% held within the 15% to17% target. DBS delivered an ROE of 16.2% squarely within the medium-term guidance range.

Management went further, noting that this ROE was several percentage points above both local peers and most global banks. The structural argument for why this is durable rests on three pillars: proactive balance sheet management, diversified and growing fee income streams, and AI-driven cost discipline all of which are increasingly embedded in the business rather than cyclically dependent on rates.

4. Every major growth market delivered double-digit profit growth, and the Citi Taiwan integration is paying off. Two years on from completing the Citi Taiwan acquisition, management was able to point to tangible results. Taiwan income grew 11% to a record SGD 1.4 billion, driven by broad-based growth across all business lines, with the bank now serving more than three million retail customers and 8,800 business clients in the market.

India was another standout income rose double digits to a record SGD 909 million, with the Institutional Banking franchise sustaining strong momentum particularly from large corporates in GIFT City, which DBS only entered in 2023. Across the wider South and Southeast Asia segment, net profit rose 16% to a record SGD 413 million. For Greater China, net profit rose 46% to SGD 791 million. All of DBS’ key growth markets India, Indonesia, Taiwan and China posted double-digit net profit growth in 2025. DBS also deepened its presence in the Greater Bay Area by raising its stake in Shenzhen Rural Commercial Bank to 19.9%, a market it has been bullish on for several years.

5. A shareholder inquired about the value of the Lakshmi Vilas Bank (LVB) investment and whether DBS is looking to increase their stake in Shenzhen Rural Commercial Bank, to which the CEO responded that the investment in LVB which has integrated under DBS Bank India helped to expand DBS’s presence, particularly in South India, while enhancing corporate banking, SME, and gold loan offerings, driving deposit growth. As a result, this has enabled DBS to become one of the largest foreign banks in India by branches with over 550 branches allowing DBS to strengthen both DBS’s physical and digital footprint, delivering significant value for the bank and its shareholders.

Furthermore, the CEO also highlighted that the acquisition of Shenzhen Rural Commercial Bank (SRCB) has been value accretive to the bank consistently providing steady dividends for both the bank and its shareholders. She also highlighted that the bank has board seats in SRCB and that increasing future stakes would rely on many factors one of which includes regulatory limits.

6. The SGD 8 billion capital return programme is underway, and total dividends rose 38% to SGD 3.06 per share. The capital return programme is being executed through two channels: an SGD 3 billion share buyback programme and SGD 5 billion in Capital Return dividends of SGD 0.15 per share per quarter over three years. In 2025, the bank completed approximately 12% of the buyback notably stepping up repurchases when the share price dipped following Liberation Day and began paying the Capital Return dividend from the first quarter. The full-year total dividend amounted to SGD 3.06 per share, a 38% increase over the prior year, comprising an ordinary dividend of SGD 2.46 and a Capital Return dividend of SGD 0.60 per share. Total shareholder returns for 2025 were 35%, comprising a 29% share price gain and SGD 2.85 per share in dividends paid during the year.

7. The CEO highlighted the impact of AI on the bank’s operations and overall strategy where AI has shifted from a buzzword to a measurable force, generating SGD 1 billion in economic value in 2025. DBS now runs over 2,000 models and 430 AI use cases, with two-thirds of employees using DBS-GPT for daily tasks like research and writing. Data scientists leveraging CodeBuddy have cut coding time by 20%, while the tech team reduced deployment times by 25%. The launch of DBS Joy, a Gen AI-powered corporate banking chatbot, has already attracted over 20,000 users, boosting customer satisfaction by 23%.

CEO also highlighted that DBS’s strong foundation across its digital space allows them to harness the potential of AI across the entire bank leveraging on AI to shape the future of banking. DBS has been recognized as “World’s Best AI Bank” by Global Finance, moving forward the bank aims to be “an AI-enabled bank with a heart,” focusing on genuine improvements in customer outcomes and employee productivity.

8. The One Bank model is translating into real numbers, with wealth AUM doubling since 2019 to SGD 488 billion. A recurring theme throughout the AGM was DBS’ “One Bank” model: the deliberate integration of wealth management, corporate banking, transaction services and markets into a unified client experience rather than siloed product lines. The strategic logic is straightforward. Over 70% of DBS’ high-net-worth wealth clients are also entrepreneurs and business owners, meaning their needs M&A advice, IPO listings, succession planning, wealth booking, trade financing spanning multiple business lines simultaneously. By breaking down inter-departmental silos and connecting data across products and geographies via AI, DBS aims to capture more of each client’s wallet. The evidence that this is working is visible in the numbers: total wealth management income rose 9% to SGD 5.7 billion, DBS now banks about one-third of Singapore’s 2,000-plus single family offices, and AUM has doubled since 2019.

9. Despite one Q4 real estate non-performing loan (NPL), DBS maintained strong asset quality. The CEO highlighted a challenging risk environment in 2025, with US tariff volatility, global real estate challenges, and AI-related asset valuation concerns. However, credit quality remained resilient, with non-performing assets down 4%, the NPL ratio stable at 1.0%, and specific allowances at SGD 854 million, in line with historical averages. Total allowance reserves stood at SGD 6.28 billion, with 130% coverage, or 197% after collateral. The CET1 ratio was 15.0%, well above the target.

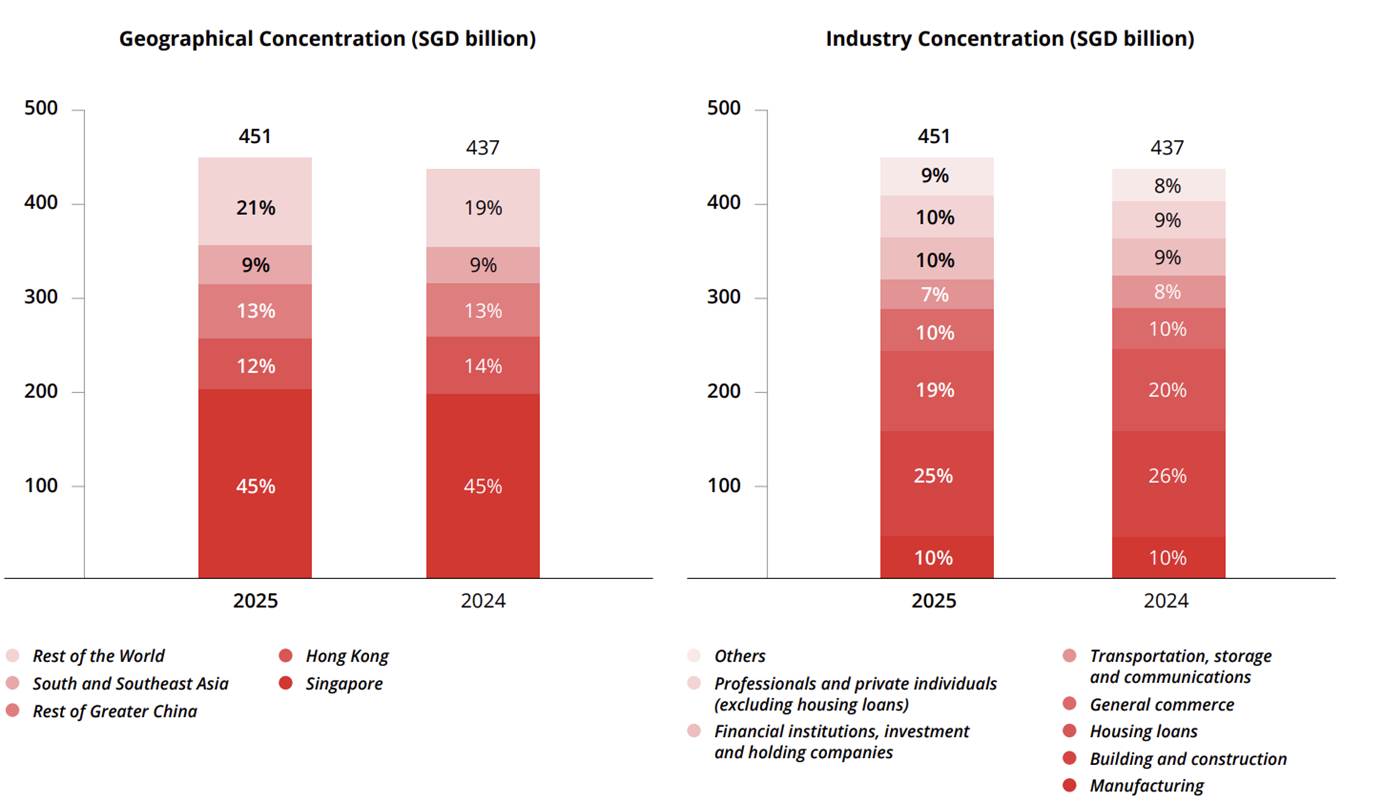

10. Many shareholders expressed concerns about the impact of the war, but CEO reassured them that DBS’s exposure to the region is minimal. She explained that stress tests showed little first-order impact, as DBS’s core market is Asia. Based on disclosures in the annual report, DBS has over 79% of total loans in Asia and is well diversified across various industries with only housing loans and building and construction having a concentration of more than 10%.

However, she highlighted stagflation risks if oil prices stay above US$100 per barrel due to prolonged conflict, with potential second-order effects like inflation, consumer slowdown, and supply chain disruptions. Ms. Tan noted that DBS is closely monitoring sectors such as autos, oil and gas, and shipping, especially if the Strait of Hormuz is closed. She acknowledged concerns over small and medium-sized enterprises but emphasized that government support will help SMEs tide through this challenging times.

The fifth perspective

The 2026 DBS Group AGM demonstrated the bank’s resilience despite external challenges. While the sharp rate declines that investors had been concerned are prevalent, DBS still posted record total income, profit before tax, and a 38% increase in dividends. The transition in leadership from Piyush Gupta to Tan Su Shan was seamless, with strategic continuity around AI investment, capital returns, and the One Bank model.

The bank’s impressive performance marked by record net new money inflows and a doubling of AUM since 2019 suggests a strong and self-reinforcing path ahead. Risks to watch include global uncertainties, particularly stagflation and sector-specific disruptions, but DBS’s diversified and AI-driven strategy positions it to navigate these challenges effectively.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »