Keppel DC REIT is a Singapore-listed real estate investment trust focused on data centre assets. Since its listing on the Singapore Exchange in 2014, it has grown into one of Asia’s leading pure-play data centre REITs, with a portfolio of 25 data centres across 10 countries in Asia Pacific and Europe. Its assets serve customers from sectors such as internet enterprises, IT services, telecommunications and financial services, making the REIT closely linked to the growth of cloud computing, digitalisation and artificial intelligence.

The 2026 AGM was especially meaningful because data centres are becoming increasingly important in the modern digital economy. As demand for data storage, computing power and connectivity continues to rise, Keppel DC REIT is not only benefiting from this trend, but also actively reshaping its portfolio through acquisitions, divestments, capital management and asset optimisation.

Here are eight key takeaways from Keppel DC REIT’s 2026 AGM.

1. Keppel DC REIT is strengthening its Asia Pacific and Japan growth strategy through acquisitions. The REIT had S$6.3 billion in assets under management and 25 data centres across 10 countries, with Asia Pacific making up 84.7% of AUM. Singapore remained the largest market at 62.7%, while Japan contributed 13.6%.

A key highlight was the acquisition of Tokyo Data Centre 3, a hyperscale data centre located in Inzai City, one of Japan’s major data centre hubs. The asset is fully leased to a major global hyperscaler on a 15-year contract with built-in annual rental escalations. This provides Keppel DC REIT with stable and predictable income, while increasing its exposure to hyperscale and cloud-related demand.

Tokyo Data Centre 3 is also strategically located, with strong connectivity and low-latency access to Central Tokyo. The asset is built to Tier III-equivalent standards and modern seismic requirements, including a base isolation system, which improves operational reliability. This strengthens Keppel DC REIT’s position in Japan, a market where demand remains strong but new supply is limited by power and construction constraints.

The REIT also increased its ownership in key Singapore assets such as Keppel DC Singapore 3, 4, 7 and 8. This reinforces its exposure to Singapore, one of the tightest data centre markets globally. These acquisitions are not merely about scale, but about improving portfolio quality in strategic markets.

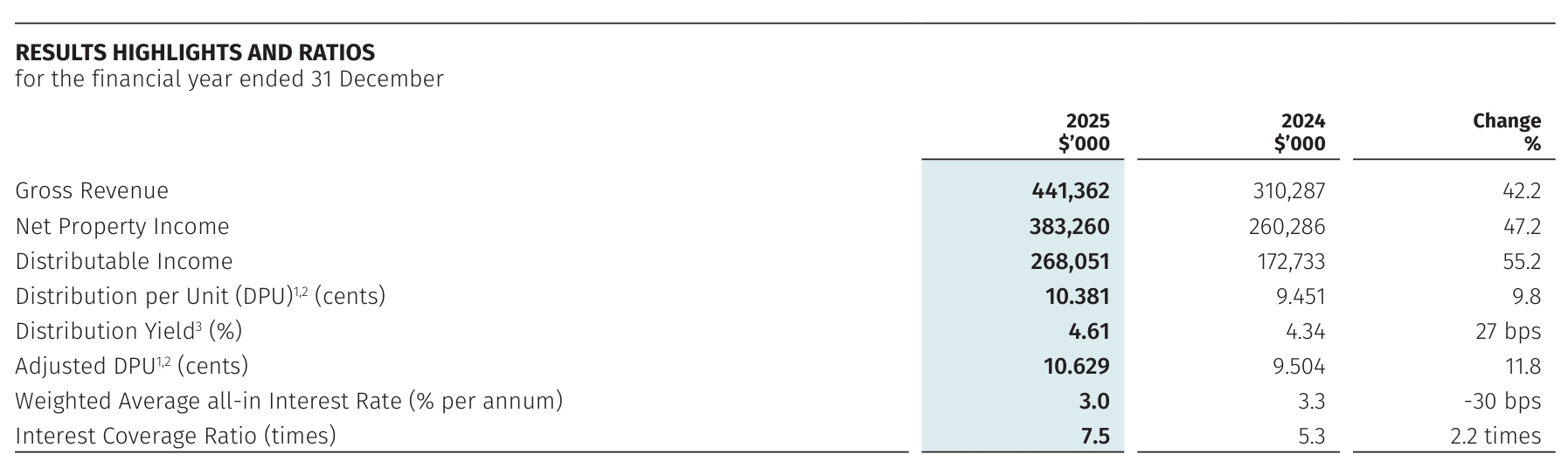

2. Keppel DC REIT delivered strong financial growth in FY2025, supported by higher revenue, stronger rental income and portfolio expansion. Gross revenue increased from S$310.3 million in FY2024 to S$441.4 million in FY2025, representing a 42.2% year-on-year increase. Net property income also rose from S$260.3 million to S$383.3 million, a 47.2% increase.

This growth was driven by several factors, including portfolio expansion, asset optimisation, stronger rental reversions and disciplined capital management. During the year, the REIT made S$1.1 billion of acquisitions, including Tokyo Data Centre 3 and the remaining interests in Keppel DC Singapore 3, 4, 7 and 8. At the same time, it divested non-core assets such as Kelsterbach Data Centre, Basis Bay Data Centre, and NetCo bonds and preference shares.

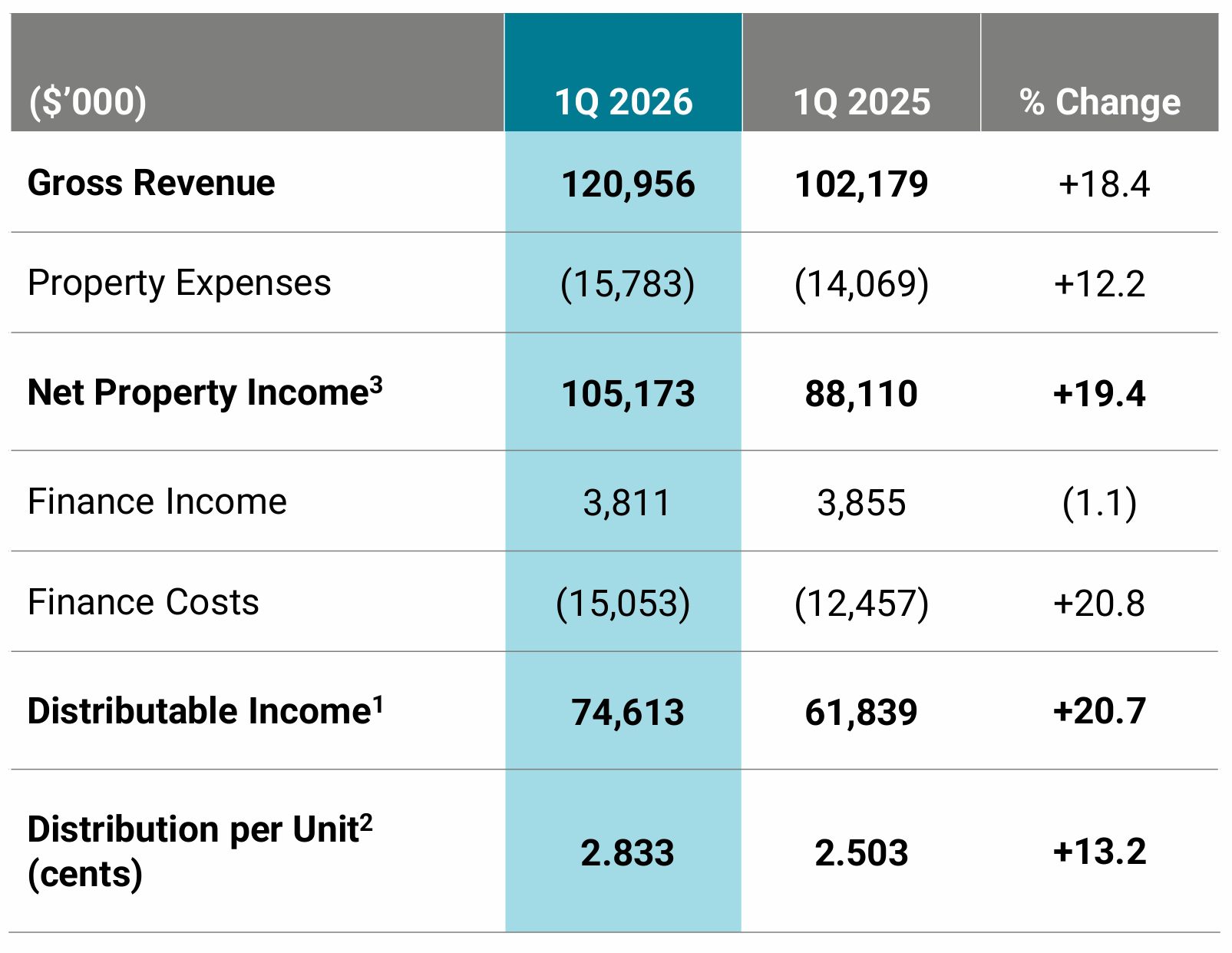

This positive momentum continued into 1Q2026, with gross revenue increasing 18.4% year-on-year to S$121.0 million, while net property income rose 19.4% to S$105.2 million.

3. Keppel DC REIT translated growth into higher DPU for unitholders. In FY2025, distributable income increased from S$172.7 million in FY2024 to S$268.1 million in FY2025, representing a 55.2% year-on-year increase. Distribution per unit also rose from 9.451 cents to 10.381 cents, a 9.8% increase.

The positive trend also continued into 1Q2026, where DPU increased by 13.2% year-on-year, from 2.503 cents to 2.833 cents. This reinforces that Keppel DC REIT’s growth strategy has produced tangible benefits for unitholders, not just a larger asset base.

4. Keppel DC REIT’s portfolio remains strong and resilient. As at 31 March 2026, portfolio occupancy was 95.6%. Its portfolio WALE also remained healthy at 6.5 years, reflecting strong income visibility supported by its long-term lease profile.

What stood out most was the portfolio rent reversion of around 51% in 1Q2026, meaning renewed leases were signed at significantly higher rents compared to the previous expiring leases. This reflects strong demand for data centre space and gives the REIT an opportunity to grow rental income as leases are renewed.

Only around 6% of rental income is due for renewal annually in 2026 and 2027, which helps limit near-term lease expiry risk. At the same time, colocation assets contribute 73.3% of rental income, positioning the REIT to benefit from rental upside in strong markets.

5. Keppel DC REIT has a disciplined debt profile. As at 31 March 2026, its aggregate leverage was 35.1%, below its internal threshold of 40%, giving it around S$550 million of debt headroom for future growth.

Its average cost of debt improved to 2.6% in 1Q2026, while its interest coverage ratio remained healthy at 7.2 times. The REIT also has a stable debt structure, with 84.8% of debt fixed-rate, which reduces exposure to interest rate fluctuations.

6. Geopolitical risk remains a concern, but data centre resilience helps reduce the impact. A unitholder asked how Keppel DC REIT would cope in a less stable global environment, particularly if data centre buildings, cables or key infrastructure were damaged or disrupted.

Management acknowledged that geopolitical instability is not positive for any sector. However, they explained that data centres are designed with redundancy as a core requirement because customers cannot tolerate downtime. This means backup systems and operational safeguards are built into the facilities to improve resilience.

Management also shared that they regularly review their standard operating procedures, supply chain resilience, and emergency preparedness measures. Another key point was the REIT’s contract structure. Power is one of the largest operating costs for data centres, but Keppel DC REIT has structured its leases such that electricity costs are largely passed through to customers. This helps minimise the direct impact of energy price volatility, with net electricity costs accounting for less than 3% of operating expenses.

While geopolitical risk cannot be eliminated, Keppel DC REIT’s data centre design, operational preparedness and lease structures help reduce the direct impact on the REIT.

7. Keppel DC REIT also benefits from strong sponsor support from Keppel. During the Q&A session, management explained that Keppel is actively supporting the REIT through its broader power and digital infrastructure ecosystem. This includes relationships with major technology companies such as Amazon Web Services and Dell Technologies, as well as capabilities in power banking, renewables, power plants, cooling solutions, and subsea cables.

This is important because data centres increasingly require more than just physical buildings; they also need reliable access to power, connectivity, and an integrated infrastructure ecosystem. Keppel’s support therefore strengthens Keppel DC REIT’s ability to plan ahead, develop future-ready assets, and capture long-term demand from cloud and AI customers.

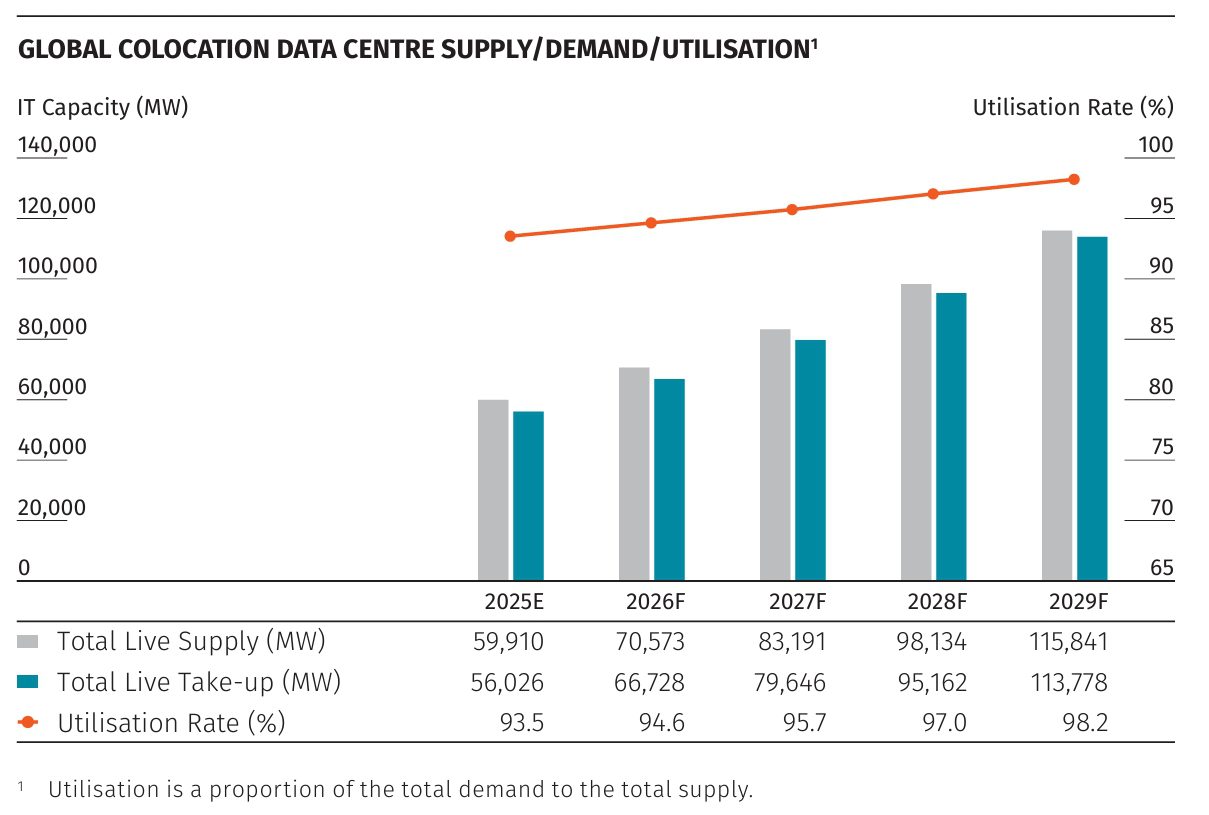

8. Shorter WALE in colocation is partly intentional, not necessarily a weakness. A unitholder asked why Keppel DC REIT’s WALE appeared to be compressing. Management explained that this was partly due to the nature of colocation assets.

For colocation assets, especially in tight markets such as Singapore and Dublin, shorter lease expiries can actually be beneficial because they allow the REIT to capture rental upside when contracts are renewed. This means a shorter WALE is not always negative. While it may increase renewal risk, it can also create pricing opportunities when demand is strong and supply remains limited.

This view is supported by the global colocation data centre supply-demand outlook, which shows utilisation rising from 93.5% in 2025E to 98.2% in 2029F. This suggests that global colocation markets could become increasingly tight over the next few years, potentially supporting stronger rental rates.

WALE should therefore be interpreted in context. In weaker markets, shorter WALE may be a risk. In tight data centre markets, it can give Keppel DC REIT more opportunities to reprice leases at higher rents.

The fifth perspective

Keppel DC REIT’s 2026 AGM highlighted a REIT that continues to demonstrate resilience, disciplined execution, and strategic agility in a fast-evolving data centre market. Despite a volatile macroeconomic environment, the REIT delivered stronger distributable income and DPU growth, supported by high portfolio occupancy, positive rental reversions, and prudent capital management. While challenges remain, including geopolitical uncertainty, refinancing risks, and weaker-performing assets such as Guangdong, management’s proactive portfolio optimisation suggests that the REIT is focused on strengthening asset quality rather than simply expanding in size.

What stood out most was Keppel DC REIT’s positioning for the next phase of digital infrastructure growth. With AI demand shifting from large-scale training towards inference and edge computing, well-located data centres with low latency and strong connectivity are becoming increasingly important. The REIT’s exposure to strategic markets such as Singapore and Japan, its growing hyperscale focus, and its colocation strategy place it in a favourable position to benefit from these trends. Supported by Keppel’s wider ecosystem including relationships with leading technology players, power infrastructure, renewables, and connectivity capabilities, Keppel DC REIT appears well-positioned to capture long-term demand from cloud, AI, and hyperscale customers while maintaining a disciplined approach to growth.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »