KLCCP Stapled Group is the largest REIT listed on Bursa Malaysia by market capitalisation. The group owns seven prime assets including Petronas Twin Towers, Menara 3 Petronas, Suria KLCC, and Mandarin Oriental, Kuala Lumpur (MOKL) within the KLCC precinct. The property value of its assets totalled RM16.7 billion in 2026.

Here are eight things I learned from the 2026 KLCCP Stapled Group AGM.

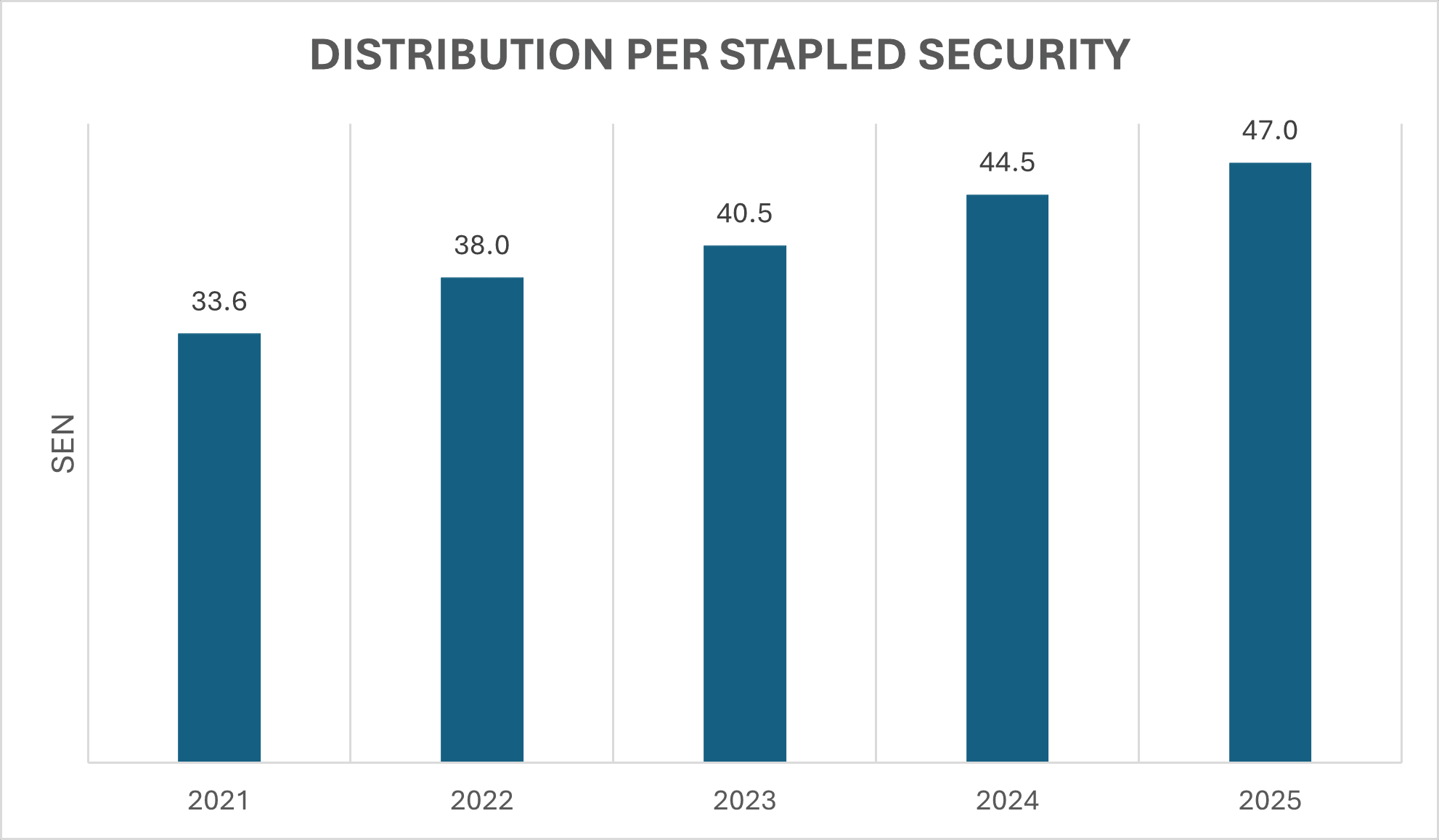

1. Revenue increased 1.7% year-on-year to RM1.7 billion in 2025, driven by full-year contribution from Suria KLCC after the Group acquired the remaining 40% stake in the retail mall. Net profit improved 21.3% year-on-year to RM1.3 billion in 2025 despite higher utility and electricity expenses alongside increased financing costs from the corresponding 2024 Sukuk Wakalah issuance. Distribution per stapled security increased 5.6% year-on-year to 47.0 sen in 2025, which is a five-year high despite the slight drop in dividend payout ratio from 92% in 2024 to 90% in 2025.

2. The office segment is a stable contributor with full occupancy and long-term leases that provides income visibility. The leases are often arranged under a triple-net-lease structure where the tenant bears most property expenses. Majority of the group’s office buildings are leased out to its sponsor Petroliam Nasional Berhad (PETRONAS) with strong credit ratings, which reduces counterparty risk. In 2025, about 32.2% of the group’s revenue came from PETRONAS alone.

| Segment | Occupancy rate | |

| 2024 | 2025 | |

| Office | 100% | 100% |

| Retail | 99% | 98% |

| Hotel | 58% | 59% |

A unitholder pointed out that the Menara Maxis tenant lease is going to expire in 2028. The management replied that as the group only owns 33% stake in the building, the responsibility to negotiate the lease renewal lies with the substantial shareholder. The substantial shareholder is a sister company to Maxis Berhad under their parent company, Usaha Tegas, making it likely that Maxis will renew the lease.

3. The retail segment recorded positive rental reversion rates as footfall improved 9.3% year-on-year to over 50 million visitors in 2025. In Q1 2026, footfall was satisfactory and increased 9% year-on-year amid the ongoing war in the Middle East and the normalisation of revenge spending post-COVID-19. Tenants in the luxury segment accounted for about 20% of its tenant mix. Further, 76% of its shoppers were locals with the remaining being foreign tourists.

The group does not have the rights of first refusal to the recently developed retail mall Ombak KLCC in the vicinity that is owned by its sponsor KLCC (Holdings) Sdn Bhd.

4. Despite the increase in occupancy rate of Menara 3 Petronas retail podium from 88% in 2024 to 97% in 2025, the overall retail revenue only increased 1.2% year-on-year to RM557.9 million in 2025. Management explained that revenue from Menara 3 Petronas retail podium only accounted for about 6% of overall retail revenue. The retail podium was facing softer tenant sales amid ongoing tenant remixing exercise and leasing initiatives. Further, City Point, the retail podium of Kompleks Dayabumi, is expected to be opened in 2027.

5. The ASEAN Summit has boosted the hotel segment revenue by nearly RM10.0 million. It has also renovated its Grand Ballroom to capture further event-related demand. According to management, MOKL outperformed its peers in the vicinity in terms of average revenue per available room.

6. Despite the 11.5% year-on-year growth in revenue from the management services and others segment to RM375.1 million in 2025, its loss before tax widened from RM5.4 million in 2024 to RM18.3 million in 2025. The management explained that the management services segment was profitable, but it also includes general corporate services which incurred higher financing costs.

The segment currently manages over 19,000 parking bays across the Klang Valley. It also provides facilities management services for retail works at Ombak KLCC, Terra, and Destina Putrajaya, which are owned by its sponsor.

7. Management refinanced its term loan into a fixed-rate sukuk at a lower borrowing cost of 3.8% per year. Annual financing cost savings amounting to RM3.2 million is expected. Gearing remained manageable at 30.5% while all of its financing were on fixed rates in 2025.

8. The Ministry of Finance has engaged the group regarding the non-extension of the 10% preferential tax rate on REITs, a policy change that remains out of the Group’s control. This development dampens the overall attractiveness of Malaysian REITs, particularly for foreign investors and high-income local individuals. Management also reassured unitholders that PETRONAS Twin Towers were designed and engineered to withstand seismic activity and the Towers are adequately insured.

The fifth perspective

The Visit Malaysia 2026 tailwind is expected to be dampened by the ongoing conflict in West Asia, which has resulted in flight cancellations and escalating travel costs. Nevertheless, KLCCP Stapled Group’s performance will be bolstered by its resilient office sector, and it remains well-positioned to capture regional tourism outflows.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »