Every AGM has two versions.

The first is the official version: slides, speeches, resolutions, dividend declarations.

The second is the version investors should care about: “What management is really signalling about the next few years…”

I attended OCBC’s 89th AGM, where management discussed its FY2025 results, shareholder returns, risk conditions, and a refreshed three-year strategy called Next Frontier.

On the surface, it looked like a routine update. But beneath it, it felt like OCBC telling investors something more important: The easy phase of banking profits may be over, and the bank is quietly preparing for what comes next.

Here is what I took away from the 2026 OCBC annual general meeting.

1. Peak-rate earnings are likely over. Over the past few years, banks around the world enjoyed a rare tailwind: rising interest rates. When rates rise, banks earn more on loans faster than they pay out on deposits. That lifted profitability across Singapore’s banking sector. But that phase is now fading.

OCBC reported FY2025 net profit of S$7.42 billion, down 2% year-on-year. Net interest income fell 6% as rates eased, and the management is further expecting one more rate cut this year. The period where rising rates did the heavy lifting is behind us. Future earnings growth will need to come from somewhere else.

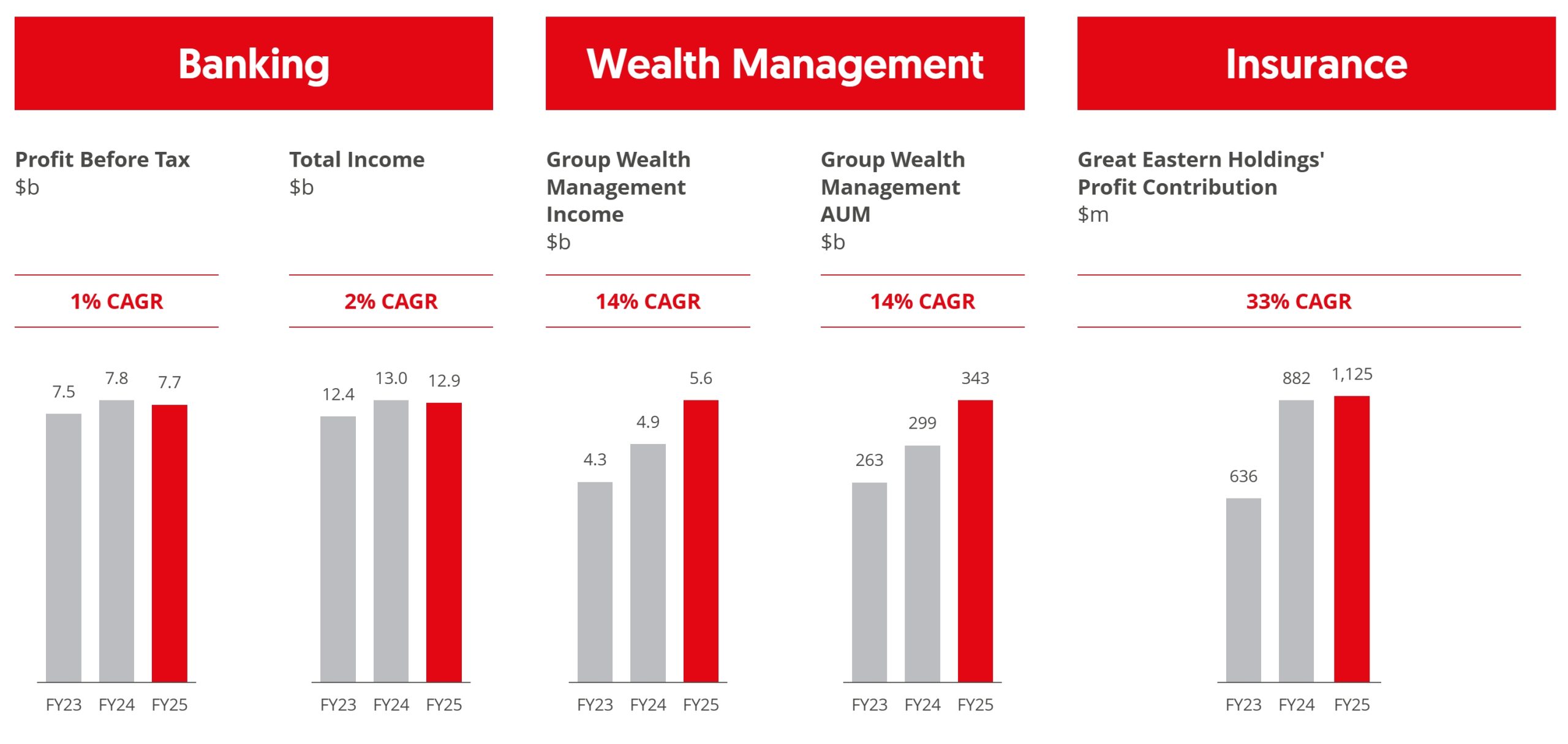

2. Non-interest income is quietly becoming the real story. Despite lower net interest income, OCBC still delivered a record profit before tax. Non-interest income reached a new high of S$5.46 billion, driven by fees, trading, wealth management, and insurance.

Insurance profit grew 28% to S$1.12 billion. Wealth AUM expanded 15% to S$343 billion, with net new money inflows of S$27 billion. It’s a meaningful signal that OCBC is attracting assets even through an uncertain environment. The cost-to-income ratio held around 40%.

While the management didn’t frame it explicitly, the performance showed that the bank is gradually becoming less dependent on rate-sensitive income, and more anchored in fee and insurance earnings that don’t move as dramatically with the cycle.

That transition is still early. Lending income remains the majority, but the direction is becoming clearer. Management signaled that while interest rate cuts are a headwind and the Group is focused on defending its ROE by shifting the mix toward wealth management and insurance. These are structurally higher-margin, capital-light businesses that provide a ‘cushion’ against falling lending margins, allowing the bank to maintain a resilient return profile across the cycle.

3. Wealth and Great Eastern must carry the next phase. As a strategic shift, OCBC is pushing towards integrated wealth management. Management calls it the “Whole of Wealth” strategy or WOW.

This aligns OCBC’s private banking arm, Bank of Singapore, and its insurance provider, Great Eastern Holdings, under a unified strategy. Great Eastern posted profits of approximately S$1.2 billion in FY2025, of which OCBC captures close to 93.7%.

And in answering one of the shareholder’s questions, the management made it clear that there will be no re-listing, no third chance for minority shareholders who missed the privatization. Great Eastern is now fully integrated into this strategy and staying there.

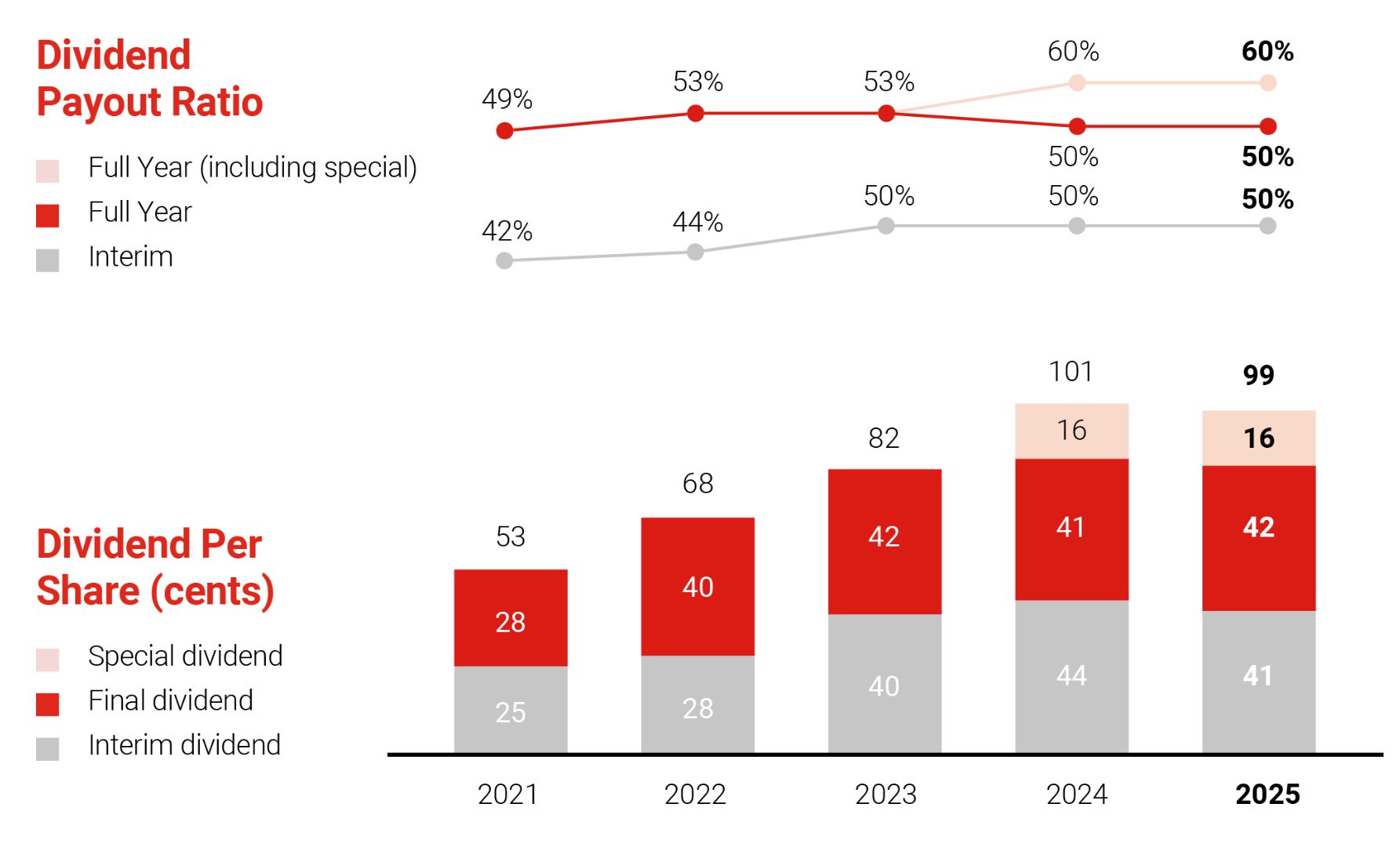

4. S$800 million in dividends may still come. The board proposed a final ordinary dividend of 42 cents and a special dividend of 16 cents, bringing total FY2025 dividends to 99 cents per share, representing 60% of net profit.

This sits within OCBC’s previously announced S$2.5 billion capital return plan: S$1.5 billion through special dividends, S$1.0 billion through share buybacks. Of the buyback portion, only around 20% has been executed, with approximately S$800 million remains.

Management made it clear that this capital return plan will be completed by FY2026. If share buybacks are not executed by then, the remainder will be paid out as special dividends, working out to about 18 cents per share.

5. Indonesia is a long-term commitment, not a short-term trade. Several shareholders raised concerns about Indonesia and the management’s response was quite unambiguous: Indonesia stays.

The numbers give context. Indonesia accounts for roughly 40% of ASEAN GDP. OCBC has operated there for 80 years, and has grown its Indonesian franchise from #12 to the #8 bank in the market. Indonesia is not a peripheral bet. It is central to OCBC’s ASEAN growth thesis.

6. The ADD strategy: AI is not actually at the center. In presenting the Next Frontier strategy, management introduced an acronym: ADD, standing for AI, Digital, and Data. But they were deliberate about the ordering and emphasis.

They explicitly chose not to put AI at the centre of the strategy, even while acknowledging its importance. Instead, Data sits at the foundation, Digital enables the customer and employee journey, and AI gets plugged in when it becomes fit for purpose and cost-effective.

The reasoning is pragmatic. AI is a fast-moving and still-expensive field. The better your data infrastructure, the easier it is to adopt new AI tools as they mature and become economical. So OCBC is building to be AI-ready, not AI-dependent.

In an environment where many institutions are rushing to brand everything as AI-driven, I found this strategic discipline refreshing. It suggests management is more interested in sustainable productivity gains than in narrative-driven technology spending.

7. The cautious tone was the real message and the Asian energy crisis is the reason. The sharpest concern for management wasn’t tariffs or recession, it was energy.

Management described the Middle East conflict in striking terms: an Asian energy crisis. Roughly 20% of the world’s oil, gas, and related chemicals flow through the Strait of Hormuz, most of it destined for Asia. The disruption doesn’t just affect fuel prices, it ripples through fertilisers, industrial chemicals, semiconductor gases, and shipping costs.

They walked through their stress-testing framework in unusual detail. First-order exposures to Middle East counterparties are limited, around 2-3% of lending. Second-order risks run through affected industries and supply chains. But it is the third-order scenario — sustained energy disruption combining with slowing growth to produce stagflation, that management identified as their most serious concern. Stagflation, as the chairman noted, took a decade to cure the last time it appeared in the 1970s.

NPL ratio remains stable at 0.9%. Credit costs were lower at 70 basis points. The balance sheet, by the numbers, still looks clean. But the language around it was that OCBC knows credit cycles eventually turn, and is managing as if one might be closer than the market currently prices in.

8. This is a cycle management story, not a compounder story. Banks are cyclical. Their earnings rise with rate cycles, expand with credit growth, and contract when the cycle turns. On a long enough timeline, quality banks trend upward. But they don’t compound in the way a great business with pricing power and reinvestment optionality does. The mechanics are different.

Reading between the lines of three years of quiet decisions: a S$5 billion redevelopment deferred, Great Eastern privatized and integrated, S$2.5 billion returned to shareholders rather than deployed, and a strong emphasis that OCBC will be celebrating its 100th year in the next six years suggest the conservative nature of the bank.

For OCBC, it is not operating under a compounder thesis, but of survivorship and stability. And in banking, over a full cycle, that discipline is often what separates the institutions that merely survive from those that genuinely build long-term shareholder value.

The fifth perspective

OCBC’s AGM did not feel like a bank celebrating peak profits. It felt like a bank that has seen enough cycles to know what preparation looks like. It is quietly making sure its shareholders understand why the decisions of the last three years were made.

The sailing ship they keep referencing is not racing toward a destination. It is being rigged for a storm that may or may not arrive, while still making forward progress.

For investors with the patience to think across a full cycle, OCBC appears to be doing the right things at the right time, even if the market doesn’t always price that in immediately.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »