As one of Asia’s largest listed healthcare REITs by asset size, Parkway Life REIT (PLIFE REIT) owns a portfolio of 74 properties spanning Singapore, Japan, and France, with a total appraised value of approximately S$2.57 billion as at 31 December 2025. Its portfolio is anchored by 3 world-class private hospitals in Singapore and complemented by 60 nursing homes across Japan and 11 in France.

I attended PLIFE REIT’s 2026 AGM to better understand how management is navigating a more complex operating environment and what their plans are for the next phase of growth. Here are eight things I learned from the AGM.

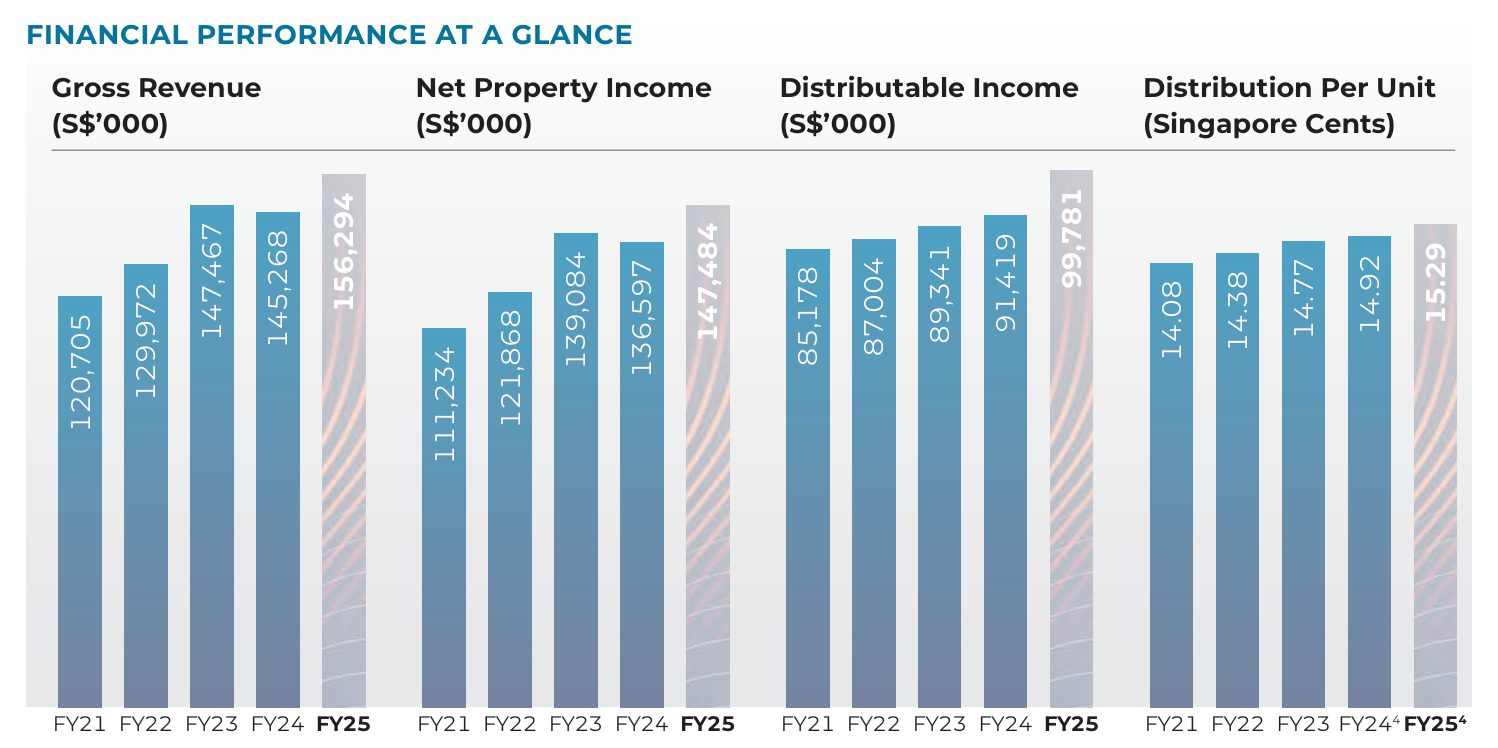

1. In FY2025, PLIFE REIT posted gross revenue of S$156.3 million for FY2025, a 7.6% increase year-on-year, with second-half revenue reaching S$78.0 million, up 7.1%. The growth was primarily driven by the full-year contribution from nursing homes acquired in Japan and France in 2024, though this was partially offset by the depreciation of the Japanese yen against the Singapore dollar.

Net of currency headwinds, the underlying operational performance was solid. Management also secured tax exemption on foreign-sourced income from the Inland Revenue Authority of Singapore and Ministry of Finance, which meaningfully improved distributable income saving S$1.7 million in tax savings. In aggregate, distributable income rose 9.1% year-on-year to S$99.8 million, net property income also rose 8% to S$147.5 million reflecting the management’s effective asset management initiatives and cost prudence across the portfolio.

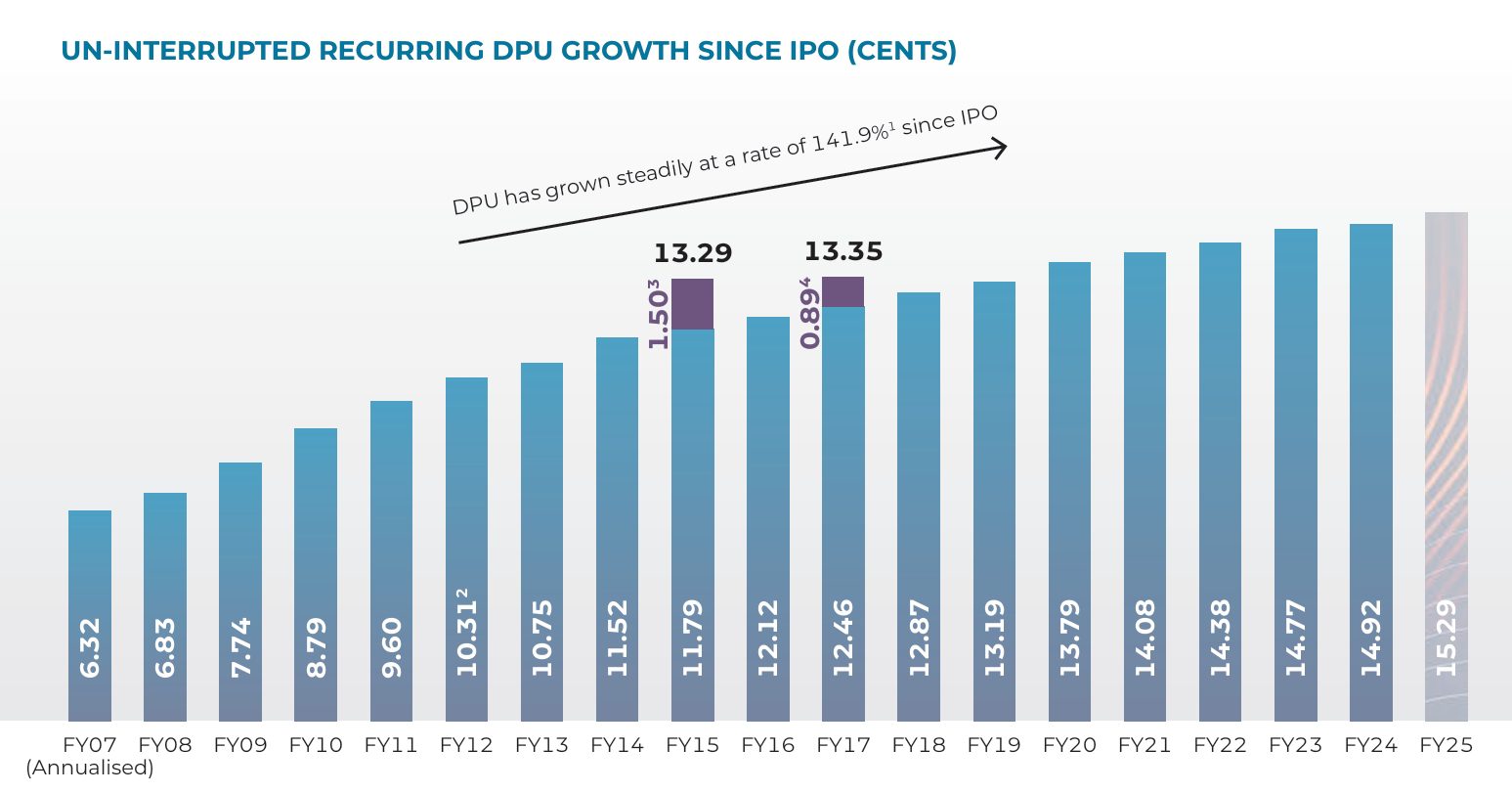

2. PLIFE REIT delivered a full year distribution per unit (DPU) of 15.29 cents for FY2025 representing a 2.5% year-on-year increase. This continues an unbroken streak of DPU growth since the REIT listed in August 2007, with cumulative growth of 141.9% since IPO from 6.32 cents to 15.29 cents.

However, the headline DPU figure deserves closer scrutiny. While distributable income grew at a stronger rate of 9.1% year-on-year, the per-unit figure rose by only 2.5% because the REIT completed an equity fund raising in November 2024, issuing approximately 47.4 million new units. The expanded unit base naturally dilutes DPU growth, meaning unitholders received proportionally less despite strong underlying income performance.

As PLIFE REIT continues to pursue acquisitions requiring fresh equity, unitholders should assess whether DPU growth net of dilution adequately compensates for the capital deployed.

3. PLIFE REIT’s balance sheet is conservatively managed with significant debt headroom. The REIT maintained a gearing ratio of 33.4% as at 31 December 2025, well below the regulatory ceiling of 50% for Singapore REITs. At this gearing level, the REIT has approximately S$557.6 million in debt headroom before reaching the 45% threshold, and S$878.5 million before reaching 50%.

The REIT’s cost of debt remains remarkably low at 1.59% per annum, reflecting the substantial portion of its debt denominated in Japanese yen where interest rates remain low and its disciplined use of the JPY bond market. As at 31 December 2025, approximately 93% of interest rate exposure is hedged, providing significant protection against rate volatility. The interest coverage ratio stands at a robust 8.6 times, giving PLIFE REIT considerable financial flexibility.

The debt maturity profile is well-staggered, with no more than 27% of total debt maturing in any single year through 2036 and no long-term debt refinancing needs until October 2026. This conservative posture supports PLIFE REIT’s ability to pursue acquisitions without being constrained by near-term refinancing pressures.

4. Singapore hospitals continue to be an engine of stable growth with 2026 marking a step change in rent. PLIFE REIT’s Singapore portfolio collective valued at S$1.74 billion contributes 60.8% of gross revenue. The properties are currently master leased to Parkway Hospital Singapore which is a wholly owned subsidiary of IHH Healthcare under a long-term triple net lease structure. This provides strong income certainty and 100% committed occupancy.

From 2026 onwards, following the transition from a fixed annual step-up structure to a new annual rent review formula, Parkway Hospitals will pay the higher of: (i) base rent plus a variable rent component equivalent to 3.8% of adjusted hospital revenue, or (ii) the preceding year’s rent escalated by Singapore CPI plus 1%. This revised structure raises the income floor for the Singapore assets and contributed to the S$135.7 million valuation gain recorded in FY2025. As hospital revenues continue to grow over time, the variable rent component also provides additional upside for the REIT.

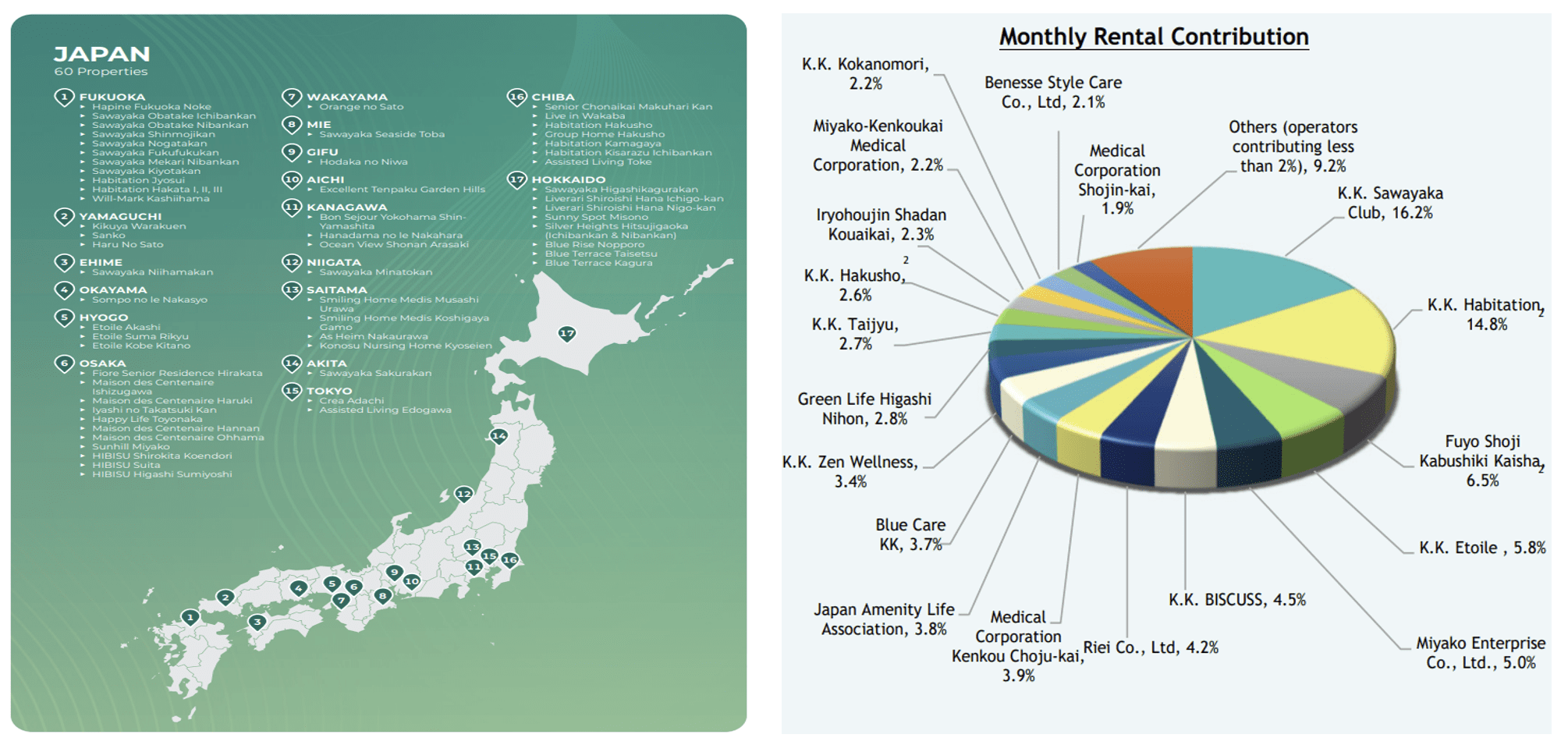

5. PLIFE REIT’s Japan portfolio remains its largest overseas portfolio, benefiting from structural tailwinds and lease protections making it an attractive protection to risks. Japan accounts for 30.4% of PLife REIT’s gross revenue and represents 25.3% of its portfolio by asset value.

The REIT has 60 nursing homes spread across 17 prefectures with a combined appraised value of approximately S$650 million. The Japanese nursing home portfolio benefits from strong structural demand, given that Japan’s elderly population represents approximately 30% of total population, far exceeding the global average of 10%.

What makes the Japan portfolio particularly attractive from a risk management perspective is its lease structure. Approximately 96% of Japan revenue is downside-protected, with most properties featuring “up-only” rent review provisions. This means that rents can be revised upwards but not downward providing revenue protection for the REIT. Furthermore, security deposits covering an average of four months’ gross rental are held for all properties, and back-up operator arrangements are in place for most assets, reducing the risk of income disruption if a lessee encounters financial difficulties.

Committed occupancy in the Japan portfolio stood at 97.7% as at 31 December 2025. The tenant base is diversified across 29 lessees, with a weighted average lease term to expiry of 10.48 years and no single tenant contributing more than 20% of Japan portfolio revenue. K.K. Sawayaka Club is the largest contributor at 16.2%, followed by K.K. Habitation at 14.8%.

6. PLIFE REIT’s entry into France in December 2024 marked its first foray into Europe, with the acquisition of 11 freehold nursing homes for approximately S$177.8 million (€117.5 million). The properties are leased entirely to DomusVi Group, the second-largest nursing home operator in France and the third largest in Europe, under a 12-year sale-and-leaseback structure with indexed rent escalations. All 11 properties carry 100% committed occupancy.

CEO Yong Yean Chau mentioned that the rationale for the France entry mirrors the Japan thesis. France’s elderly population represents approximately 22% of total population, again well above the global average. The European eldercare market is fragmented and capital-intensive, with operators increasingly seeking sale-and-leaseback arrangements to free up capital for operational expansion. The choice of DomusVi as a counterparty matters considerably. With over 40 years of operating history, 600-plus nursing and senior residential homes across seven countries, and a bed count that has grown consistently from 49,700 in 2021 to 52,300 in 2024, DomusVi is not a marginal operator taking on a lease it cannot sustain. The lessee quality reduces the counterparty risk that would otherwise accompany a first-time entry into an unfamiliar regulatory environment.

France remains an early-stage growth story. Revenue contribution in FY2025 was partially offset by broader currency headwinds, while management also acknowledged that sustainability integration and climate risk assessments for the French portfolio are still ongoing. As such, investors should view France as a medium-term growth opportunity rather than an immediate earnings catalyst. That said, the underlying foundation appears well-constructed and provides a platform for longer-term expansion.

7. During the AGM, the CEO highlighted that Parkway Life REIT has fully exited the Malaysian market following the successful divestment of its strata units and carpark lots at MOB Specialist Clinics in Kuala Lumpur. The portfolio was sold for RM20.1 million (S$6.1 million) to Pantai Medical Centre Sdn. Bhd., a subsidiary of IHH Healthcare Berhad.

The transaction highlights a strong exit valuation, with the sale price representing a 25.6% premium over the original purchase price and a 4.6% premium over the average of recent valuations. Although Malaysia accounted for only 0.2% of the REIT’s total portfolio value, this move aligns with management’s broader strategy of portfolio optimization and value unlocking. By divesting these non-core assets, the REIT strengthens its balance sheet and sharpens its focus on core markets, enhancing financial flexibility to pursue higher-growth opportunities that deliver greater long-term value to unitholders.

8. A unitholder asked how management actively mitigates foreign exchange risks, given the REIT’s expanding international footprint. In response, management emphasized that while currency risk is actively managed, it remains a structural feature of the portfolio.

With 60% of gross revenue anchored in Singapore, the remainder is drawn from Japan (30.4%) and France (8.8%), leaving the REIT inherently exposed to foreign exchange fluctuations. To mitigate this volatility, management has deployed a hedging strategy designed to shield both capital values and distributable income.

For the Japan portfolio, capital exposure is mitigated through a deliberate structural approach. CFO Mr. Loo Hock Leong highlighted management’s preference for natural hedges, noting that matching foreign assets with local currency debt is the most efficient way to reduce balance sheet volatility. Accordingly, PLIFE REIT’s JPY-denominated acquisitions are fully financed with JPY-denominated borrowings. As a result, any decline in the yen’s asset value is largely offset by a corresponding reduction in liability value, helping to protect the REIT’s net asset value without relying heavily on costly derivative hedging instruments

For the France portfolio, the CFO explained that the REIT had effectively locked in the exchange rate for its principal investment from the outset. This was achieved through a cross-currency swap, which converted the Singapore dollar proceeds raised from the equity fund-raising exercise directly into euros. As a result, the capital value of the French assets is largely protected from fluctuations between the SGD and EUR, reducing foreign exchange risk at the balance sheet level.

The fifth perspective

Parkway Life REIT’s investment philosophy is built on two key principles: forming long-term partnerships with quality operators, and building scale within existing markets to improve operational efficiency and tax advantages. This disciplined approach has helped the REIT avoid overpaying for assets while creating sustainable income streams.

CEO Yong outlined a three-pillar growth strategy focused on strengthening existing markets like Japan, building a third core market beyond France, and deepening strategic partnerships. PLife REIT benefits from a first-mover advantage in Japan, a strong Singapore base, and an expanding European platform through DomusVi.

That said, healthcare real estate remains a specialised and competitive sector, with increasing competition from private equity and sovereign wealth funds. As such, the REIT’s ability to leverage relationships with sponsors like IHH Healthcare and DomusVi for proprietary deal flow will be key to sustaining acquisition growth without pursuing dilutive deals at compressed yields.

Overall, Parkway Life REIT’s combination of stable Singapore hospital assets, expanding exposure to high-demand nursing home markets in Japan and France, and disciplined capital management continues to support its positioning as a resilient and defensive REIT for long-term unitholders.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »