United Overseas Bank (UOB) is one of Singapore’s major banking groups, with a strong regional presence across ASEAN. The bank provides a wide range of financial services, including retail banking, wealth management, wholesale banking, trade finance, treasury services, payments, and cash management. Its scale is reflected in its enlarged customer base of around 8.5 million customers across ASEAN.

We attended UOB’s 2026 annual general meeting to gain deeper insights into the bank’s performance, strategic direction, and key areas of focus. Here are eight key takeaways from the AGM.

1. ASEAN remains central to United Overseas Bank’s long-term strategy. CEO Wee Ee Cheong stated that despite a more volatile and uncertain global environment, ASEAN continues to be one of the world’s most resilient regions. The region is also becoming increasingly interconnected through trade, investment, and cross-border growth, which aligns closely with UOB’s regional banking model.

UOB’s ASEAN-4 markets (Malaysia, Thailand, Indonesia, and Vietnam) recorded 5% year-on-year income growth, outperforming the overall Group, whose income declined by 2%. This highlights the strength of UOB’s regional banking model and its long-standing relationships with businesses and individuals across ASEAN. Management also emphasised that UOB already has the scale, customer trust, and brand recognition across the region, and that its next priority is to extract greater value from the platform it has built.

2. UOB’s acquisition of Citigroup’s consumer banking portfolios in the ASEAN-4 markets was presented as an important strategic move. During the Q&A session, the CEO shared that the acquisition required significant time and effort to integrate across the four countries. He viewed the integration as successful, as it enabled UOB to double its customer base.

The acquisition supports UOB’s broader ASEAN strategy by significantly expanding its regional retail customer base. Management stated that UOB will continue investing in infrastructure and capabilities to capture greater value from this enlarged customer base. As such, the acquisition was not positioned as a one-off expansion, but rather as a platform for building deeper customer relationships, strengthening regional connectivity, and driving future revenue growth.

3. UOB delivered a resilient financial performance in 2025 despite a challenging operating environment. The CEO reported full-year operating profit of S$7.7 billion, supported by UOB’s diversified business model, which helped the bank remain resilient even as margins moderated in a declining interest rate environment.

Fee income and customer-related treasury income reached record highs, helping to offset pressure from lower margins. In retail banking, UOB’s enlarged customer base grew to 8.5 million customers across ASEAN. Card billings increased 8% year-on-year, supported by UOB’s lifestyle and rewards ecosystem spanning travel, dining, and entertainment.

Wholesale banking also contributed meaningfully to growth. The CEO shared that trade loans grew 26% year-on-year, supported by UOB’s integrated payments, trade, and cash management platforms, as well as its regional connectivity across ASEAN. In addition, UOB continues to focus on high-growth sectors such as technology, sustainable energy, electric vehicles, consumer goods, and infrastructure.

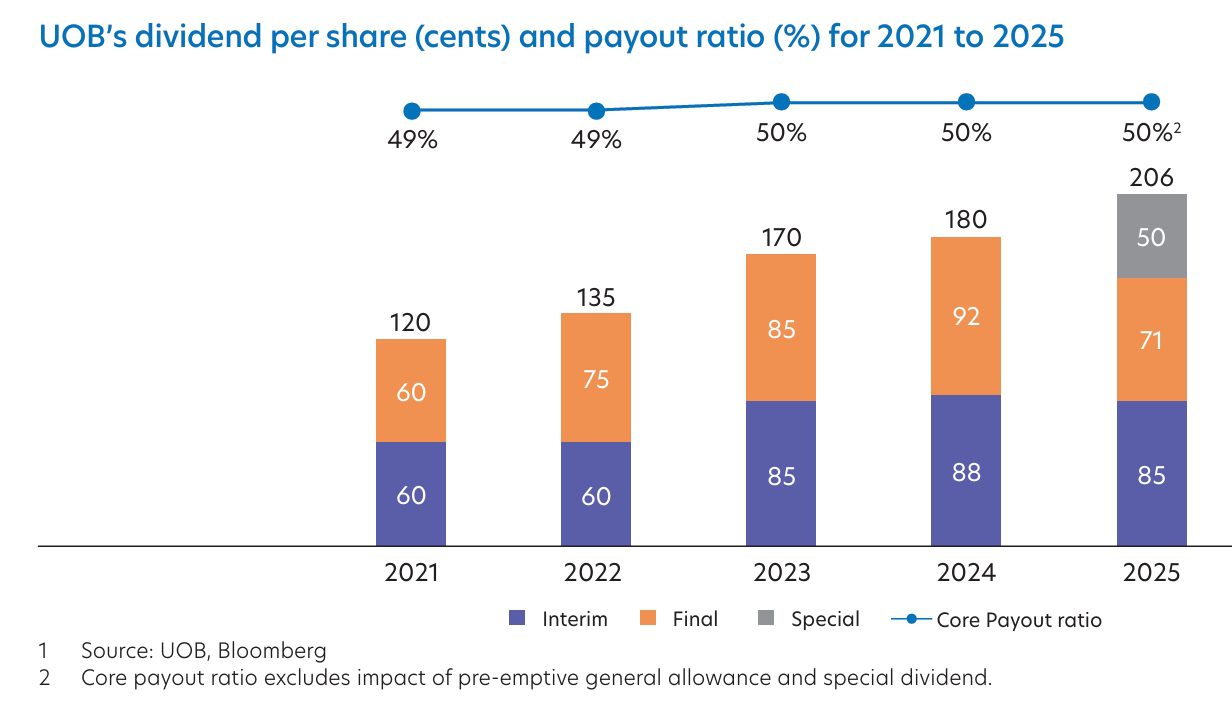

4. Shareholder returns remained an important theme at United Overseas Bank’s AGM. The CEO stated that 2025 required prudence and discipline, but emphasised that the bank’s pre-emptive provisions did not affect its final dividend payout.

The board recommended a final dividend of 71 cents per share, bringing UOB’s full-year dividend to S$2.06 per share, including special dividends. This represented a payout ratio of 50%, reflecting the bank’s continued commitment to delivering consistent returns to shareholders while maintaining financial resilience.

UOB also remains committed to returning S$3 billion of surplus capital to shareholders between 2025 and 2027. Management explained that this reflects confidence in the bank’s balance sheet strength, liquidity position, and long-term strategy.

5. UOB highlighted wealth management as a major long-term growth opportunity. The CEO stated that wealth management penetration remains below its potential, and that UOB aims to double its wealth management business by 2030.

Management positioned Singapore as one of the world’s leading wealth centres and noted that UOB has a strong foundation to grow in this segment due to its heritage, extensive ASEAN footprint, SME relationships, and connections with entrepreneurs across ASEAN and Greater China. UOB plans to scale the business organically through its One Bank programmes across wholesale and retail banking, higher investor penetration, more personalised solutions, and improved pricing strategies.

UOB also intends to continue investing in talent by expanding its private banking team and strengthening its digital wealth capabilities across ASEAN, Greater China, North Asia, and Europe. As a result, management views wealth management as an increasingly important fee-income growth engine for the bank.

6. Geopolitical risk was also raised during the Q&A session, particularly in relation to the ongoing Middle East conflict. A shareholder asked about the potential secondary impact on SMEs, especially businesses affected by logistics disruptions, supply chain challenges, and trade links to the Middle East.

The CEO responded that the situation remains fluid and that UOB is monitoring developments closely. He noted that if the conflict continues to drag on, unintended consequences could become more severe. Management has conducted stress tests and believes the bank is in a position to manage the situation prudently.

The CEO also emphasised that UOB is paying close attention to how it can support customers, particularly SMEs, which employ a significant portion of the workforce across the region. When asked whether the bank may need to make additional provisions, he responded that he hoped this would not be necessary. He added that UOB’s strong customer relationships and balance sheet provide the bank with the ability to support customers if needed, and that the bank has a broader social responsibility to help customers through difficult periods.

7. Sustainable development was also discussed in response to a shareholder question on energy price shocks, supply chain disruptions, renewable energy, electric vehicles, and cleaner supply chains. The shareholder asked how UOB is helping retail customers, SMEs, and wholesale clients transition towards cleaner energy solutions.

The CEO responded that ASEAN countries are at different stages of development, meaning that solutions need to be tailored to the specific circumstances of each market. Chief Sustainability Officer Eric Lim added that UOB identified this trend several years ago and has since built solutions to help individuals, SMEs, and large corporations adopt cleaner energy technologies. These solutions range from basic solar installations for homes and businesses to more advanced battery management systems. UOB also provides financing and support for electric vehicle adoption and is focused on helping clients participate in new economy value chains, including critical minerals and the broader energy transition.

8. A shareholder also asked about the sharp increase in allowances for credit and other losses. CFO Leong Yung Chee explained that these figures were linked to asset quality issues encountered during the year. UOB conducted a detailed review of its portfolio against a backdrop of heightened macroeconomic uncertainty, particularly in the U.S. and Hong Kong commercial real estate market. Collateral values had softened, while the recovery outlook remained uneven. As a result, the management, with the board’s endorsement, decided to set aside a proactive pre-emptive provision of S$615 million.

The CFO added that this general provision buffer helped maintain the bank’s general provision ratio at around 1% and improved unsecured coverage of non-performing assets to 254%. The provision also provides UOB with greater flexibility in managing future recoveries, reducing the need to dispose of or recover non-performing assets at distressed prices.

The fifth perspective

United Overseas Bank’s 2026 AGM demonstrated a strategy centred on regional growth, disciplined risk management, and long-term value creation. ASEAN remains UOB’s core growth platform, supported by the integration of Citigroup’s consumer banking portfolios and continued investments in technology and infrastructure. Financial performance remained resilient, driven by strong fee income, growth in card billings, and continued momentum in trade loans. At the same time, management maintained a prudent approach through proactive provisioning and disciplined capital management.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »