In 2025, Wilmar paid US$709 million for a mistake made in 2021.

That’s not a typo.

Indonesia’s Supreme Court found five Wilmar subsidiaries guilty of corruption, specifically, of profiting illegally from cooking oil export permits during a national supply crisis four years ago. The compensation and fines amounted to IDR 11.9 trillion. At the time, that figure was roughly equivalent to 60% of Wilmar’s entire annual net profit. Headlines were brutal and a major broker slapped a ‘sell’ rating with a S$2.50 target price.

At the annual general meeting held last week however, the mood in the auditorium wasn’t one of crisis. It was one of quiet confidence.

Here’s what I took away from the 2026 Wilmar International AGM.

1. The fine is provisioned; the reputational question isn’t. Management’s position at the AGM was clear: The Indonesia fine has been paid and reflected in the financials. Now, it’s time to move on. CFO Charles Loo confirmed the payment was embedded in operating cash flows.

Lead Independent Director Lim Siong Guan also reiterated that Wilmar has a ‘clear and unwavering commitment’ to compliance and ‘does not tolerate any corrupt or illegal practices’.

That said, what was notably absent was any frank explanation of how it happened in the first place. Will it happen again? Or if there are any measures taken to close the gap?

For investors, this matters. The corruption case stemmed from actions taken during Indonesia’s 2021 cooking oil shortage. It’s possible to argue that what happened was a localised lapse rather than a systemic cultural failure. But without management addressing that distinction directly, we’re left filling in the blanks.

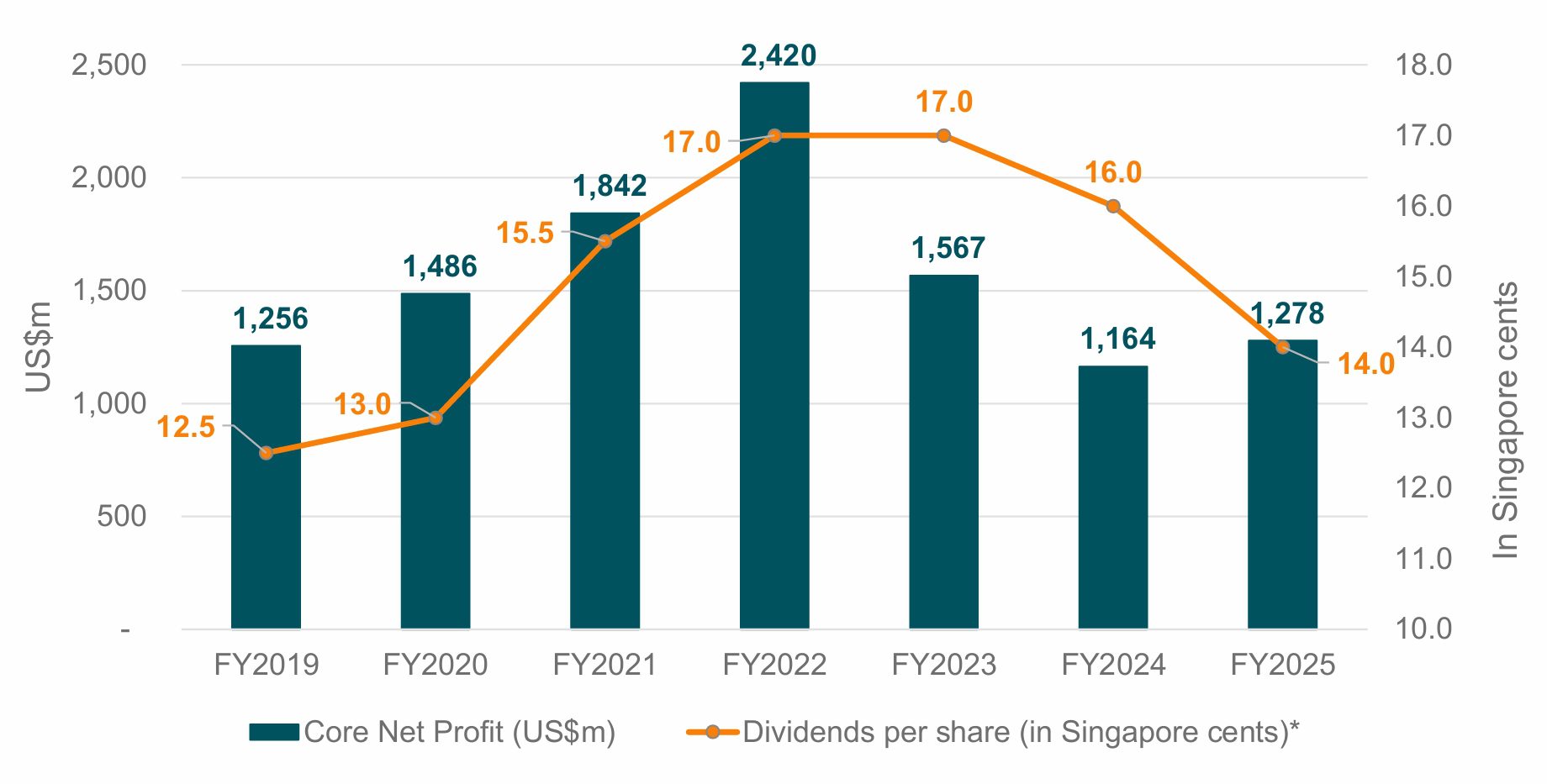

That said, the financial hit is firmly in the rear view mirror. FY2025 core net profit, stripping out all one-off charges, came in at US$1.28 billion, up 10% year-on-year. The underlying business didn’t skip a beat. That’s genuinely impressive for a company that just absorbed a US$709 million legal blow.

2. The dividend: Defensive, not structural. FY2025 total dividend came in at S$0.14 per share, down from S$0.16 the prior year. The chairman’s explanation is that the company had to pay a significant fine last year. The global uncertainty also remains elevated and they needed to stay on the safe side. With free cash flow potentially sitting at US$1.3 billion annually as capex normalises, the capacity to restore and even grow the dividend is clearly there. The cut looks defensive, not structural.

3. The US$20 billion debt and what it actually is. Wilmar’s balance sheet carries US$19.7 billion in net debt. At face value, that puts the net debt-to-equity ratio at 0.91 times. That number alone triggers alarm bells.

But CFO Charles Loo was clear at the AGM: ‘Our debts are predominantly for working capital purposes.’

Wilmar’s debt isn’t financing losses or speculative expansion. It’s financing commodity inventory. When you are one of the world’s largest traders and processors of palm oil, soybeans, wheat, and sugar, you need enormous working capital to purchase raw materials, process them, and hold them through the supply chain before selling. That inventory is liquid by nature. If Wilmar stopped buying commodities tomorrow, a substantial portion of that debt would wash off the balance sheet within weeks as inventory converts to receivables and cash.

The more meaningful number is adjusted net debt-to-equity, which excludes working capital-related debt. At the AGM, the CFO confirmed this stands at just 0.34 times, a conservative figure for a business of this scale.

4. Capex is falling and that’s an important signal. Capex is falling — down 31% to US$1.08 billion. This line alone deserves more attention in Wilmar’s FY2025 results. This isn’t cost-cutting. It’s telling us that the heavy construction phase is over.

Wilmar has spent the better part of a decade building out food parks in China, soybean crushing plants in Vietnam, refining capacity in Africa, and distribution infrastructure across India. The CFO was direct at the AGM: ‘We are now focusing more on extracting benefits from past expansions.’

With operating cash flow of US$2.36 billion, minus the capex of US$1.08 billion, this puts Wilmar’s free cash flow at approximately US$1.3 billion annually. Wilmar is transiting from a high-capex mode to ‘harvest’ mode. When a capital-intensive business successfully crosses this threshold where existing assets generate returns rather than consume capital, free cash flow tends to inflect upward meaningfully.

5. India is the next decade. The most strategically significant development discussed at the AGM wasn’t in the main presentation. It was buried in the Q&A segment: Wilmar’s consolidation of AWL Agri Business in India.

AWL (formerly known as Adani Wilmar), was a 50:50 joint venture between Wilmar and the Adani Group, dating back to 1999. In late 2024 and through 2025, Adani moved to fully exit the partnership, selling some of its stake to Wilmar in two tranches for approximately $2 billion.

The company now holds approximately 57% of India’s largest food FMCG company, with a 20% market share in edible oils under the Fortune brand, reach into 1.6 million retail outlets, and distribution to over 123 million households. This also means that all legacy shareholder agreements with Adani, including board representation rights negotiated since 1999, have been formally terminated. Wilmar now controls its own destiny in India.

The Chairman’s long-term vision was bullish at the AGM: “India could be maybe as big as China, or close to it. But maybe 15 to 20 years down.”

The structural logic mirrors exactly what Wilmar did in China over 26 years: Build commodity processing infrastructure first, then layer branded consumer products on top, and capture the margin uplift as incomes rise.

It seems that they are executing the same playbook in India, from a position of early-mover dominance without the governance overhang of a troubled partner. Near-term earnings dilution from AWL integration is real. But the strategic clarity gained is worth considerably more.

6. Indonesia’s B50 biodiesel mandate is a tailwind. A shareholder asked about Indonesia’s planned B50 biodiesel programme, requiring 50% palm oil content in diesel fuel blends that’s set for implementation from July 2026. The chairman replied that Wilmar will increase palm oil prices and improve utilisation of its processing plants.

Wilmar operates over 230,000 hectares of oil palm plantations, two-thirds of which are in Indonesia. A policy mandate that structurally increases domestic palm oil consumption tightens exportable supply, which supports global pricing. For Wilmar, higher palm oil prices benefit the plantation segment directly while improving throughput utilisation in processing.

7. China & central kitchens: The margin pressure zone. China remains Wilmar’s dominant market via its A-share subsidiary, Yihai Kerry Arawana (YKA). Wilmar bold vision for central kitchens are industrialized hubs designed to standardize Chinese cuisine at scale. The chairman compared the model to McDonald’s: Food is prepared centrally and delivered to outlets where staff need minimal training to serve a consistent product. Wilmar is scaling this aggressively: Three new food parks launched in FY2025, bringing the total to nine nationwide.

However, investors should note that management was noticeably evasive on occupancy and utilization, offering only that success remains ‘a long way off’. While candid, this also raises an important point investors should watch closely: with nine parks still in their gestation phase, elevated fixed costs are likely to weigh on the Food Products segment’s margins over the next 12 to 24 months.

8. Wilmar is quietly growing – if you look close enough. Another shareholder asked why Wilmar doesn’t expand into developed markets like the US or Europe.

The chairman’s answer was revealing. He invoked the old idiom about a one-eyed man in a kingdom of the blind, explaining that Wilmar would be a second-tier player competing against entrenched giants on their home turf. But in China, India, Vietnam, Indonesia, Nigeria, and across Africa, Wilmar has the financial strength, operational infrastructure, political relationships, and decades of institutional knowledge that Western competitors cannot match.

This is the real frame for understanding what Wilmar is. It is not just a Singapore commodity company. It is a global emerging markets consumer staples conglomerate in disguise. Because while it’s commodity processing backbone gets all the attention, Wilmar’s branded consumer products business is where the long-term margin story lives.

The fifth perspective

Late in the meeting, a shareholder raised succession planning. The chairman’s response landed with quiet confidence: ‘I’m still probably the best person in the world to achieve this.’

I’ve long admired Mr Kuok, he was one of the first people I looked up to when I began my investing journey. He is always candid and confident in his answers to all shareholders. Then again, he’s 77, and the succession risk is real.

Mr Kuok has built something extraordinary, and part of Wilmar’s success is a bet on him specifically, not just the institution. That concentration of human capital doesn’t show up in any financial ratio but it’s a risk worth acknowledging.

Wilmar is not an easy company to frame neatly. It is operationally formidable, geographically irreplaceable in its core markets, and entering what looks like a meaningful free cash flow harvest phase.

For patient investors who can hold through the noise, Wilmar is a business worth understanding deeply. The storm of 2025 is largely behind it. What comes next may be the most interesting chapter in its 30-year history.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »