In my previous article, I shared three easy ways to find investment ideas fast. One of the ways to find new investment ideas is through the day-to-day observation of the things around you —which was how I came across Padini Holdings Berhad (Bursa: 7052) on a business trip to Malaysia.

I was walking around Mid Valley Megamall observing the retail stores and I realized that certain stores had more shopper traffic compared to the rest; Padini was one of them. As is my habit, I Googled to find out if Padini was public-listed (it was!) and I dug in to find out more.

And so, here are six things I found out about Padini Holdings:

1. Padini is a fashion company that owns multiple fashion brands

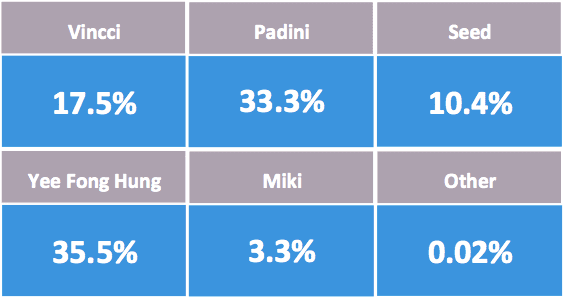

Padini is one of the most successful homegrown Malaysian fashion companies. It owns the fashion brands Padini, Vincci, Tizio, PDI, Seed, Brand Outlet and P&Co.

From the table above, the highest revenue contributor for Padini is Yee Fong Hung which holds the Brand Outlet and P&Co brands. The next highest contributors are Padini and Vincci which account 33.3% and 17.5% of total revenue respectively.

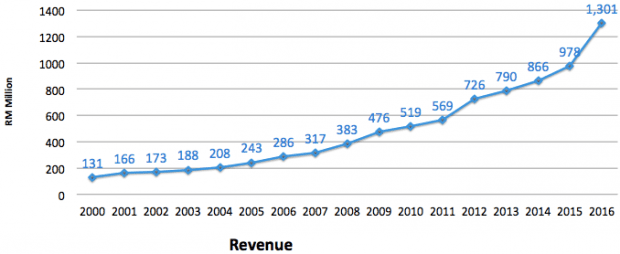

2. Consistent growth in revenue

Padini’s revenue has been growing consistently for the past 16 years despite new entrants like Uniqlo and H&M in Malaysia. This track record speaks for itself on how the management has done a great job in fighting off competition.

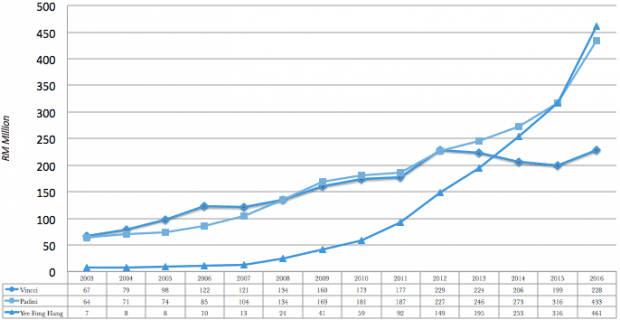

3. Growth is coming from Padini and Brand Outlet

Vincci used to be the company’s largest revenue contributor but it has since been overtaken by Padini and Brand Outlet which has been a hit with Malaysian consumers. In 2016, Brand Outlet become the company’s largest revenue contributor for the for the first time. Moving forward, we should see more growth from the Padini and Brand Outlet brands.

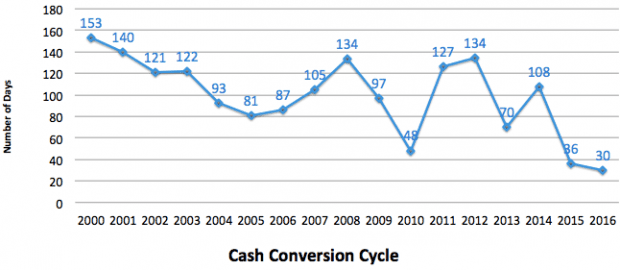

4. Falling cash conversion cycle

Cash conversion cycle (CCC) indicates how fast the company turns their inventory into cash. A decreasing CCC is a good sign; Padini now just takes 30 days to turn their inventory to cash compared to 153 days in 2000. Padini was able to reduce its CCC significantly when management introduced an IT system to manage inventory and track customer buying behaviour.

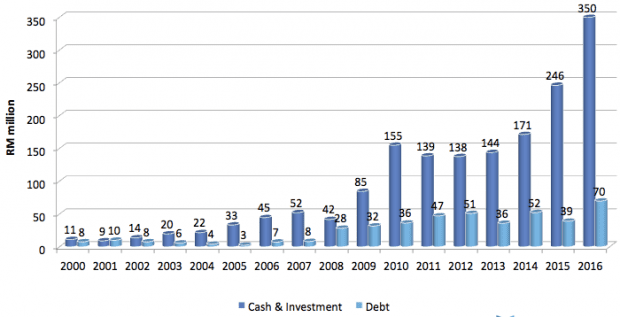

5. Cash rich and low debt

A company that is cash rich is always an investor favorite. For the past 16 years, Padini has always been in a net cash position. The most recent six years has seen the company’s cash position increasing tremendously while debt level remains low.

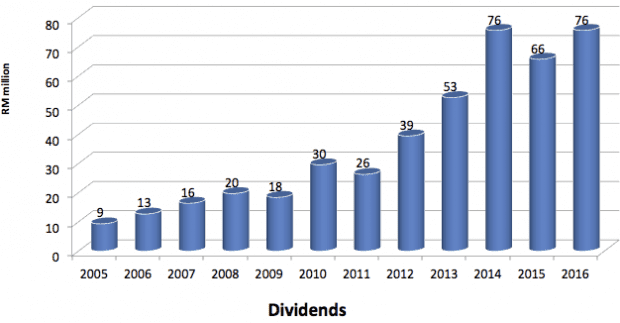

6. Growing dividends

Padini has been paying increasing dividends the past 16 years. Even during tough periods like the 2008/09 subprime crisis and the 2011 euro debt crisis, Padini was still able to pay a dividend to shareholders. The way Padini is able to grow its revenue during a crisis and pay a dividend speaks volumes about the company’s financial strength and market positioning.

I fully agree that Padini code 7052 is a good investment share to invest. The current price is RM 2.80 per share and its 52 week high/low is RM 3.08/1.54, Dy= 4.1%. the other plus point is that its gearing is low. Those new investors who are groping especially for good returns can buy this share. This email is not a recommendation to you to buy. You should study this share.

Hi Abraham,

While I do agree that Padini is a good company, it is still important to focus on the intrinsic value of the business instead of its stock price. Price doesn’t matter when there is no intrinsic value to back it up with.

My opinion is that valuing the company using dividend yield alone may not be complete. You may want to use other valuation methods to gain a fuller picture of Padini’s intrinsic value 🙂

“Price is what you pay, value is what you get” – Warren Buffett