Most investors who followed Centurion Corp last year checked one box and moved on.

The CAREIT IPO happened. The stock rallied nearly 50%.

The special dividends were declared.

Story over.

The market watched a company monetise its assets and assumed it had seen everything. But here’s the more important question:

“What does Centurion become after the assets leave the balance sheet?”

The answer is something the market isn’t pricing at all.

The supply-choked foundation

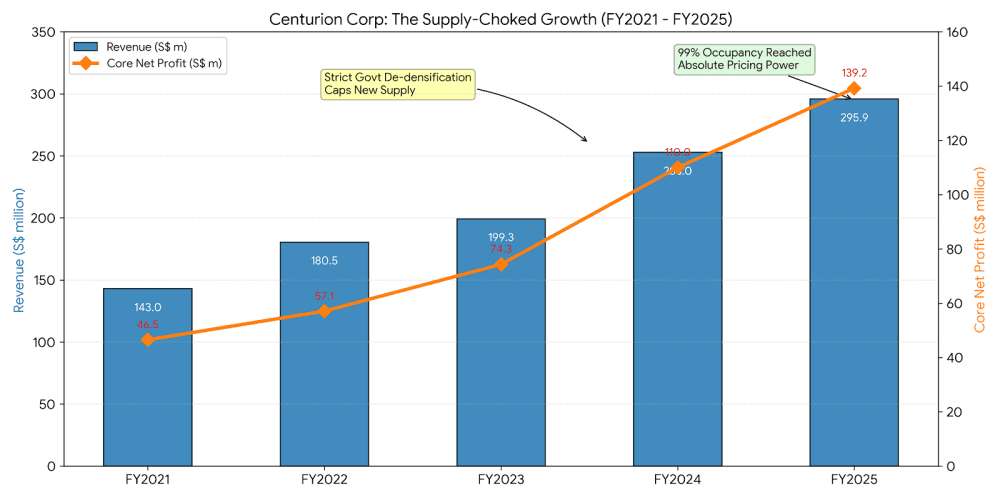

To understand why Centurion has such absolute pricing power, you only need one number: 99%.

That is the occupancy rate of its Singapore worker dormitories. When the Singapore government introduced post-pandemic de-densification regulations to improve living standards for migrant workers, the unintended consequence was a hard ceiling on compliant bed supply, arriving precisely as the marine and construction sectors entered a multi-year upcycle.

When you own an essential asset at 99% occupancy in a supply-constrained market, rental revisions stop being negotiations. They become notifications.

This dynamic drove Centurion’s FY2025 revenue to a record S$295.9 million, up 17% year-on-year. Core net profit rose 26% to S$139.2 million, stripping out one-off IPO costs and fair value adjustments. These aren’t cyclical numbers. They are the output of a market where supply cannot respond to demand.

What the market saw, and what it missed

The CAREIT IPO in September 2025 was one of the largest public offerings of the year. Centurion raised S$1.8 billion in cash and units. And while everyone was focusing on that number, some missed the contracts Centurion kept.

When the heavy real estate transferred to the REIT, Centurion retained the property management agreements. It went from landlord to operator. In other words, the company didn’t exit its assets, it transformed its relationship with them. It went from capital-heavy rent collector to fee-income machine.

The distinction matters enormously. A landlord needs to deploy S$100 million to grow. An operator however, only needs the REIT to acquire the next asset, then clips a highly lucrative management ticket on everything that follows.

In Q4 2025 alone, the property management fees Centurion collected from CAReit carried an estimated net profit margin of nearly 49%. The quality of their earnings has permanently shifted.

The gap between what it is and how it’s priced

Stock screeners still classify Centurion alongside traditional real estate developers and assign it a conservative low double-digit P/E multiple. That classification made sense when Centurion owned dormitories and collected rent. That said, it no longer reflects what the business actually does.

Asset managers and franchise operators — businesses whose growth doesn’t require large debt tranches, trade at meaningfully higher multiples. As Centurion’s high-margin fee income becomes the dominant line in its P&L through FY2026 and beyond, the market will eventually be forced to apply a different lens to the stock.

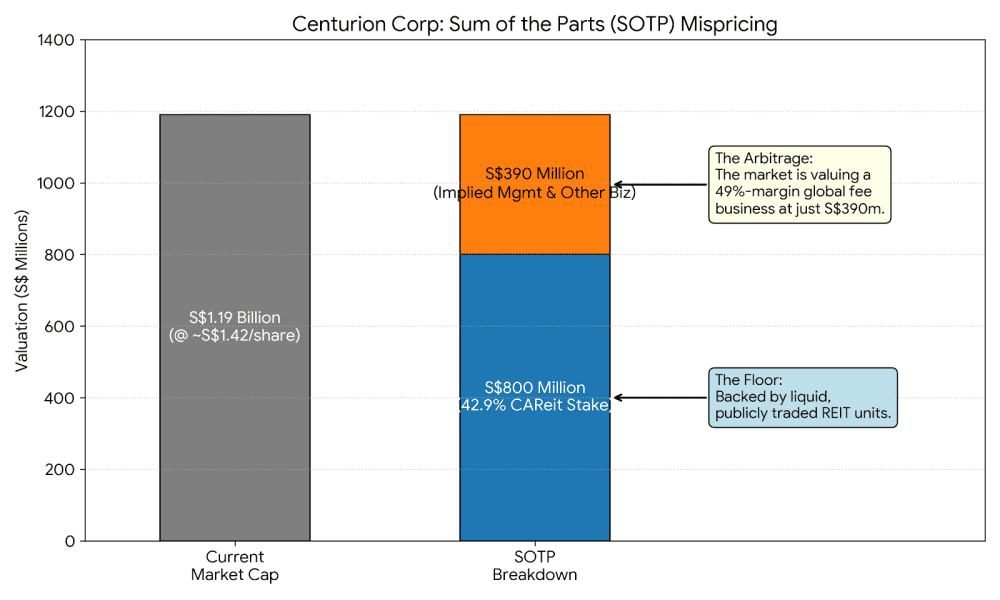

The sum-of-parts math makes the mispricing concrete.

Centurion’s current market capitalisation sits at approximately S$1.19 billion, trading around S$1.42 per share. Centurion retained a 42.9% stake in CAREIT after the IPO. Those liquid, yield-paying units are worth approximately S$800 million on the open market today.

Subtract S$800 million from S$1.19 billion and you get roughly S$390 million, which is what the market is currently charging you for everything else. That includes a global property management business generating nearly 49% net profit margins, plus all of Centurion’s non-REIT international assets.

For S$390 million, you are buying a business that, if listed as a standalone asset management entity, would command a meaningfully higher multiple than what is implied today.

The perpetual motion machine

Now here comes the million dollar question, if Singapore is supply-constrained, where does growth come from?

In early 2026, management explicitly signalled their first move into the Middle East, targeting joint ventures rather than outright land purchases. Choosing this capital-efficient entry reflects just how differently Centurion thinks about expansion now compared to three years ago.

The structure behind this is what makes it sustainable. Centurion identifies assets in new markets, does the operational heavy lifting to stabilise them under its Westlite operating template, and eventually injects them into CAREIT to recycle capital.

In short, the REIT buys the asset. Centurion manages it. Fees flow back. Capital frees up for the next market.

They haven’t just executed a value unlock.

They’ve built the infrastructure for a repeating one.

The Fifth Perspective

When companies execute major transactions, the real test is whether the proceeds find their way back to minority shareholders. Centurion passed that test in February 2026, when the board proposed a special dividend-in-specie, distributing one CAREIT unit for every 10 Centurion shares held.

Singapore’s worker housing shortage is a genuine social challenge. But from an investment standpoint, Centurion has done something rarer than simply benefiting from a supply constraint. It has built a business model around being the indispensable operator of the solution.

Today, Centurion is a company that controls a licensed, recession-proof oligopoly, earns management-firm margins, and is still being priced like a concrete pourer.

The market may have stopped watching too early.

Disclaimer: The author holds position in Centurion. The views expressed are his own and do not constitute financial advice.