For much of the past three years, Food Empire Holdings (SGX: F03) has been viewed through a single dominant lens: Geopolitics.

The company is often treated as a proxy for the Russian economy. Currency volatility, sanctions risk, and geopolitical uncertainty often dominate the narrative. As a result, Food Empire has historically been valued with a significant “fear discount.”

That framing did not emerge without reason. Historically, Food Empire’s geographic exposure was skewed toward markets where macroeconomic and political volatility frequently overshadowed business fundamentals, particularly Russia and Ukraine.

What is less widely discussed, however, is how the company has been quietly repositioning itself. Today, that repositioning has begun to alter the structure of its business

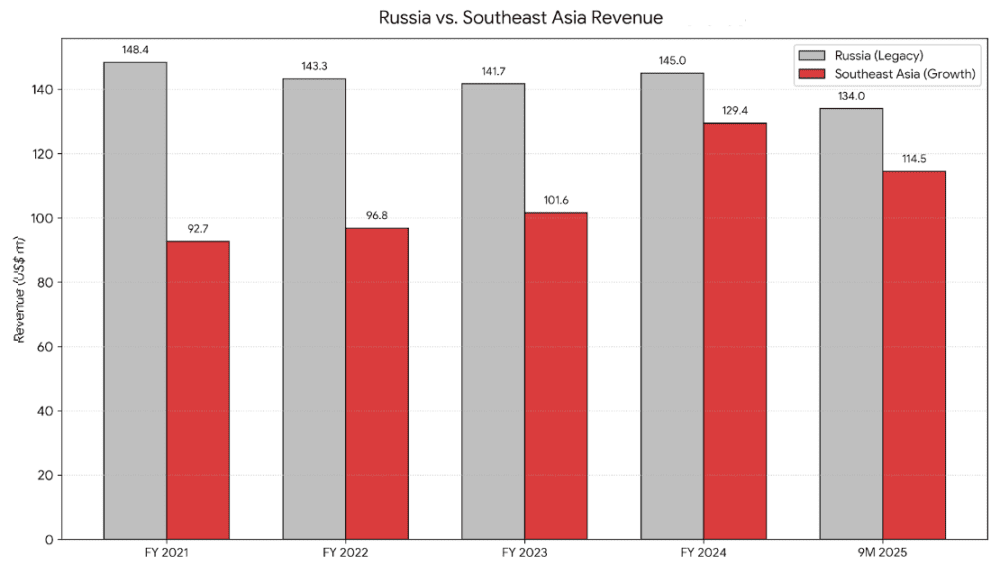

A Structural Data Point: The 2025 Revenue Crossover

For years, Food Empire’s expansion into Southeast Asia, was viewed as incremental. The prevailing assumption was that while the region provided growth, it would remain secondary to the company’s Russian operations.

In the first quarter of 2025, that assumption was challenged.

For the first time in the Group’s history, revenue from Southeast Asia (US$40.0 million) exceeded revenue from Russia (US$39.4 million).

While the Russian segment reclaimed the top spot in subsequent quarters, underscoring the resilience of the legacy business, the Q1 crossover was a critical leading indicator. It proved that the gap has narrowed to the point where Southeast Asia is no longer a distant second, but a statistical peer.

This convergence is driven by pace. In the first nine months of 2025 (9M2025), the Southeast Asia segment expanded by 20.8%, fueled largely by Vietnam, which recorded 29.3% year-on-year revenue growth and now accounts for over 60% of the segment’s total.

Carving A Niche In Vietnam

Food Empire’s flagship instant coffee brand, Café PHO, has carved out a niche on its own, achieving an estimated 15% market share in Vietnam’s instant coffee segment. Approximately 88% of the company’s sales in Vietnam are generated through “General Trade”, which comprises of small independent retailers, wet markets, and roadside stalls.

This distribution model introduces both complexity and durability. Distributing across thousands of small outlets requires time, local knowledge, and sustained execution. But once shelf space is secured, it tends to be relationship-driven, suggesting that market share gains are not easily displaced.

In fact, management has guided that the Vietnam segment is on track to cross the US$100 million revenue milestone in FY2025.

More importantly however, the company is not relying solely on new capacity to support this growth. Through targeted automation upgrades, Food Empire expects to increase output from existing production lines by approximately 15% in 2026 and 30% in 2027, suggesting that recent growth momentum in Southeast Asia can be supported without an immediate capital expenditure lull.

And what makes this shift even more consequential, is how management has chosen to respond once that growth has been established.

Capital Allocation as an Indicator of Intent

Food Empire is currently constructing a US$80 million freeze-dried coffee manufacturing facility in Vietnam. Relative to the size of the Group, this represents a significant long-term investment. Such a commitment suggests that management views Southeast Asia not as a short-term growth contributor, but as a region requiring expanded production capacity over time.

Alongside this consumer-facing investment, the company has also committed US$37 million to expand its spray-dried coffee facility in India by approximately 60%, with completion expected by end-2027. Rather than targeting India as a branded market, management has positioned these operations as an ingredient supply base, supporting both its consumer brands and external B2B clients while reducing reliance on third-party suppliers. In an environment of volatile coffee bean prices, this vertical integration provides a degree of margin protection that pure branded players lack.

These capital commitments – US$117 million across Vietnam and India, indicate that management is building infrastructure to support sustained growth rather than optimizing for near-term returns.

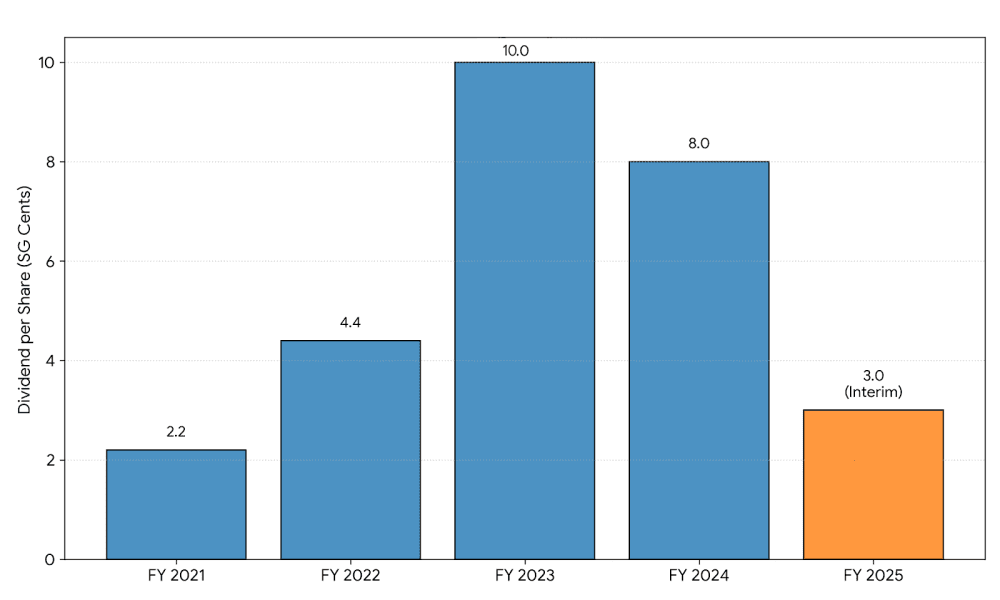

Notably, this reinvestment has been balanced alongside shareholder distributions. In 2025, the Group declared its first-ever interim dividend of 3.0 Singapore cents per share.

This acceleration of returns, coupled with the buyback of approximately 3.6 million shares, does indicate that the management is pursuing expansion while maintaining the financial flexibility to reward shareholders.

The Fifth Perspective

Historically, Food Empire’s share price has been highly volatile, largely driven by two structural factors: a high concentration of earnings in a single geopolitical region, and currency translation effects from the Russian ruble.

That is no longer the whole picture.

We’ve seen this pattern before.

The last time we identified it early, we made a 243.5% return in two years.

Food empire’s growth is VERY similar to Super Group’s ingredient growth…

The company now operates with three interconnected pillars, which, when viewed together, point to a business that is no longer defined by a single geography

- a mature, cash-generative Russian business,

- a growing Southeast Asian consumer segment led by Vietnam, and

- an India-based production and ingredient platform that supports margin control and supply continuity.

While this does not remove risk or predetermine future outcomes, the evolving business structure suggests that Food Empire today is materially different from how it is often framed.

And while the market has begun to recognise elements of Food Empire’s transformation, whether that recognition has fully caught up with the company’s evolving geographic balance and supply chain structure remains an open question. Narrative shifts, after all, tend to arrive in stages.