The upcoming IPO of Ant Group has certainly left me excited — I’m personally a huge believer in the potential of fundamentally-sound companies with strong growth drivers.

At the same time, putting our emotions aside, we should be wary of investing in companies at the IPO stage if they have not yet demonstrated a consistent track record of profitability. Over the week, I analysed the various reasons why much hyped-about companies at the IPO stage flopped. So let me share with you my findings behind three recent notable IPO flops:

1. Snap

In March 2017, Snap Inc. IPOed with much investor excitement. Its share price surged by 10-20% within two trading days. However, tech analysts’ warning about this euphoria proved prescient as Snap’s share price tumbled by more than 50% over the next two years. It has since struggled to provide any glimpses of an attractive, long-term investment.

Although Snap has managed to increase its revenue consistently over the past five years, it has still not turned a profit during that time. They have incurred huge expenses that have left its operating income in the red even before taxes and interest costs.

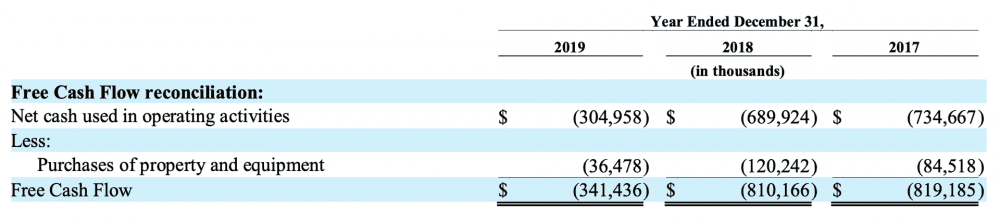

Unfortunately, Snap has also been burning cash year after year as seen from its negative operating cash flow figures. Needless to say, Snap’s further cash outflow due to CAPEX leaves it with negative free cash flow, a very unhealthy financial position. Cash is king, so why invest in a business that cannot generate cold, hard cash?

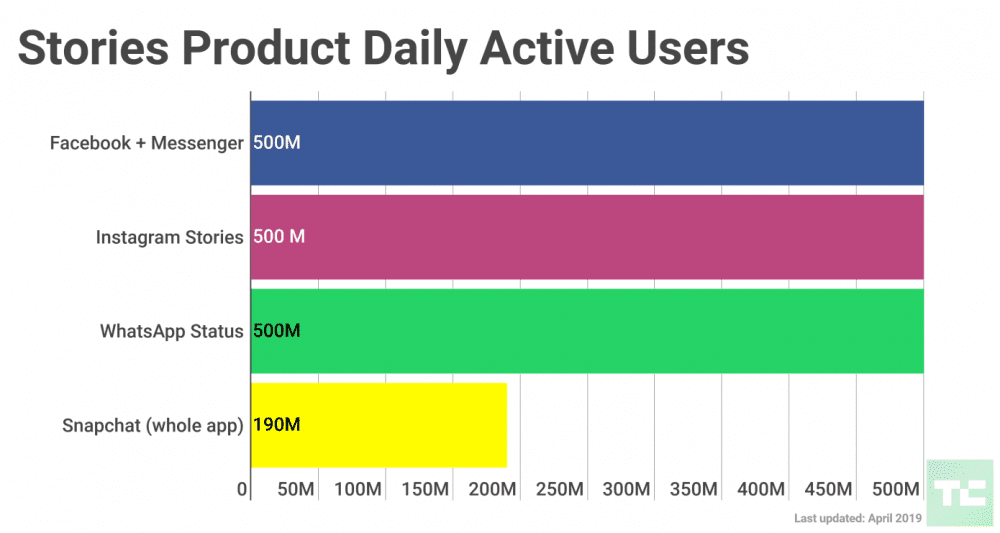

The number of daily active users on Snapchat clones like Instagram Stories and WhatsApp Status have also been much greater than on Snapchat. Isn’t it sad that Instagram, Facebook, and WhatsApp are beating Snapchat handily at its own game?

Snap is also losing badly to much larger competitors like Facebook. Almost all of Snap’s revenue is derived from advertising dollars. So to be profitable, Snap essentially pits itself against advertising giants like Alphabet and Facebook, who together form a strong duopoly in the advertising market.

2. Uber

Investing in a loss-making company is not necessarily a bad thing if it has a business model that might enable its profitability in the future. Case in point: Beyond Meat, whose recent IPO didn’t turn out too shabby. Beyond Meat dominates the plant-based protein sector and is well placed to capitalise on the growth of the alternative meat market.

Uber is a counterexample — Uber has failed to live up to investors’ hype that it would be the next Facebook with its share price still underwater since it listed at $45. Uber is a technology company that connects taxi drivers and commuters via its Uber app. It neither owns any cars nor employs any drivers. Like Snap, Uber still remains highly unprofitable 11 years after its founding in 2009.

To generate profitability, Uber can either increase its revenue by raising its fares or to cut costs by reducing the amount it pays to drivers. But Uber can do neither. Uber drivers are already protesting against their low pay and poor working conditions. In some U.S. states, Uber drivers are earning below their respective states’ minimum wage. Uber has no room to cut drivers’ pay.

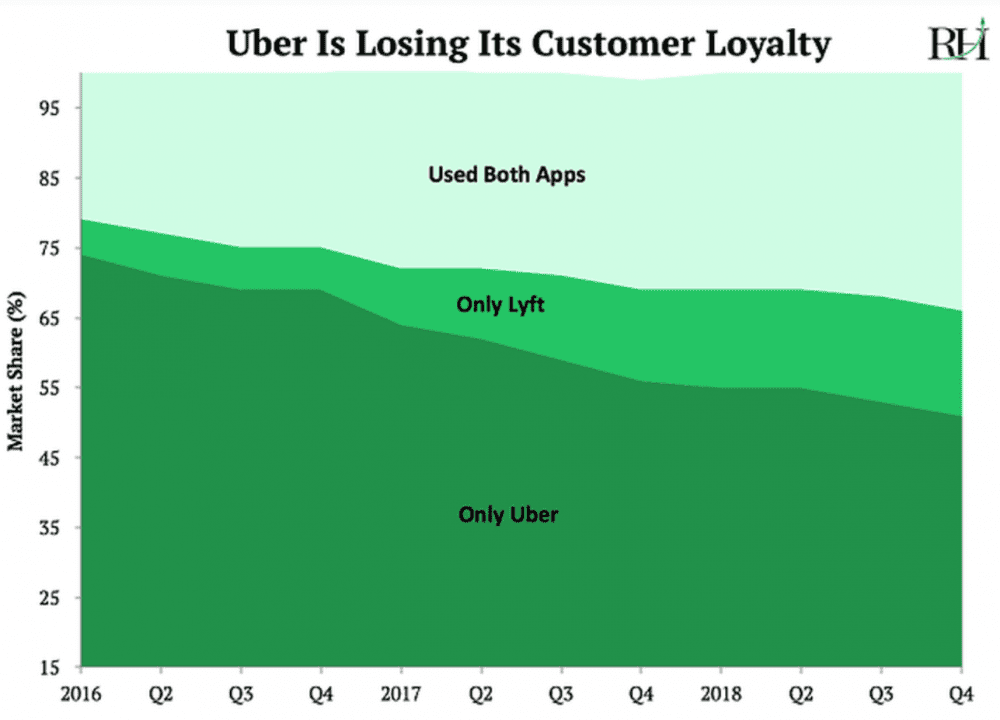

Uber also lacks any pricing power as its features and brand equity are not in any way superior to its closest competitor in the U.S., Lyft. Switching costs are also low — I can install both Uber and Lyft apps on my phone and use either. So the only way Uber and Lyft try to set themselves apart from each other is to constantly undercut each other by lowering prices.

To provide a counterexample, it would be a technical nightmare to switch my company’s productivity suite from Microsoft to Google, so both Microsoft and Google try to outcompete each other by making better products. It will be extremely jarring for me to use both Microsoft and Google productivity suites at the same time.

But since Uber and Lyft dominate the ride sharing market in America, can’t they collude and set profitable prices for themselves? Apart from the fact that this invites regulatory scrutiny, they can’t because they operate within a broader industry called transport. Uber has to compete with public transport, your personal automobile, and your feet as well!

Uber’s global expansion plans have also been unsuccessful as domestic ride hailing services in London, Russia, China have managed to uproot Uber in their domestic markets. Thus, Uber’s business model lacks the economic moats and any geographic growth drivers to become profitable in the future.

Uber is certainly a disruptor in the taxi business and has changed the way we commute. So although it’s true that Uber is some sort of a tech/social ‘revolutionary’, we as investors should not be enamoured by castles in the air but by solid business models.

3. Slack

Since Slack’s IPO in June 2019, its share price has tumbled by almost 50%, before work-from-home arrangements in light of COVID-19 lifted Slack to just beneath its IPO price of $26 again.

Apart from its lack of profitability, Slack’s poor market performance is due to the intense competition it faces from its business communication platform competitor, Microsoft Teams. While Slack is a stand-alone app, Microsoft Teams is instantly plugged into Microsoft’s larger ecosystem of its enterprise software suite which includes Office, Outlook, OneDrive, etc. (Although Slack can also be integrated with Microsoft and other third-party apps.)

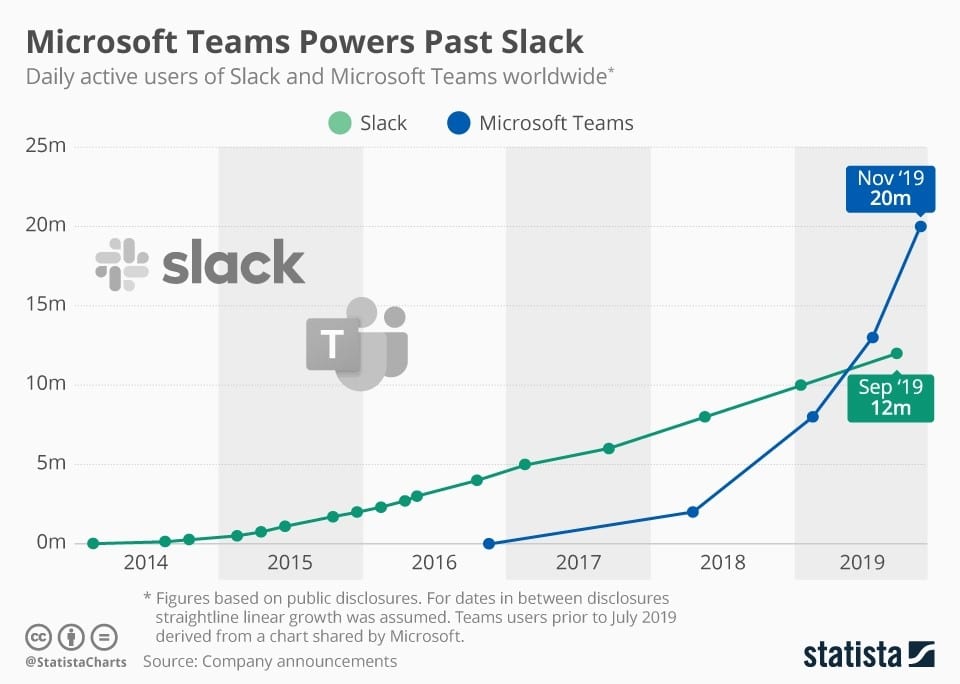

After the COVID-19 pandemic normalised work-from-home arrangements, the number of daily active users on Microsoft Teams overtook that of Slack’s. This is probably due to companies realising the need for a business communication platform as they are now geographically dispersed, and they find Teams conveniently residing in their Microsoft 365 suite of products.

On the other hand, in June this year, Amazon gave Slack a vote of confidence by signing a multi-year agreement with it to use Slack for all its 800,000 plus employees. This is a good opportunity for Slack to build up a network effect as Slack can multiply across Amazon’s supply chain partners and retailers. Slack’s market presence and satisfaction levels among its users are also quite on par with Microsoft Teams’ users.

The use of Slack and Teams is also divided between small and big companies. Small companies prefer using Slack due to its innovation, while big companies prefer using Teams for its security.

The points raised here are not for anyone to make a judgement as to whether Slack or Teams is ‘better’. Rather, it is to illustrate the multi-dimensional competition between Slack and Teams in this business communication space. Because of this intense competition, it is not clear whether Slack can outdo Teams in the future. But before Slack demonstrates profitability, it is wise for fundamentals-driven investors to be cautious about investing in Slack.

The fifth perspective

The growth of tech unicorns is always an exciting one — their innovation can dramatically transform the lives of mankind for the better. But remember, when we invest, we do not invest just from the viewpoint of the fan or consumer, but as an investor.

So before we invest in any company, we should always make sure that they are fundamentally-solid businesses with strong economic moats and growth prospects. Don’t fall in love with a stock no matter how sexy it is, and let emotional ties get in the way of sound investing decisions.

For Slack, can you please also compare with Zoom, a popular web-meeting platform, that gained huge demand during this Covid-19 period.

Hi Ing Hwa,

Thanks for the suggestion. Slack and Zoom’s core features in the digital collaboration environment are different from each other.

Slack mainly offers convenient instant messaging and quick file sharing for its clients. Zoom is best known for its video-conferencing technology. As they offer quite complementary capabilities, Zoom and Slack can thus integrate themselves on each other’s platforms. This was a reason I decided to compare Slack to Teams, who behave more like substitutes to each other, rather than Zoom!

While not mutually exclusive, companies/individuals may choose to opt for only either Slack or Zoom out of budgetary constraints. So then, how to choose? As Zoom and Slack both rank highly on security, user experience and app integrations, it can be hard to decide between the two.

Their differences can be subtle – For example, Slack is well-known for its highly configurable collaborative environment while Zoom is great for companies who video-conference often.

From an investor’s perspective, companies in the digital collaboration industry do not appeal to me since they fail to convince me of any possible economic moats around their services.

I may not have answered your question quite directly, but I hope my reply provides my views about the digital collaboration space as an investor.

Cheers,

Dean