Nike, a global giant and iconic brand in the athletic wear industry, has long been synonymous with innovation, performance, and style. At the heart of its business model is a powerful combination of cutting-edge product design, aggressive marketing campaigns, and strategic endorsements from top athletes. This powerhouse strategy helped Nike build an empire with loyal customers spanning across continents.

However, even giants stumble. Nike’s stock has taken a significant hit, plummeting by as much 30% before staging a slight recovery recently. This dramatic decline has raised eyebrows among investors and prompted many to question what’s happening behind the scenes. This article will dive deep into the underlying causes of Nike’s recent stock performance issues. More importantly, for investors like you, we’ll explore whether this sharp decline offers an opportunity to invest in one of the world’s most enduring brands at a potentially undervalued price point. Join us as we dissect the numbers and analyse if Nike’s current struggles could translate into future gains for savvy investors.

Poor financial performance and outlook

The recent financial performance of Nike has left investors deeply concerned. In its fiscal Q4 2024 results, the company reported revenues of US$12.6 billion, which signifies a 2% decrease compared to the previous year. This disappointing report highlights Nike’s struggle to maintain growth momentum and adapt to evolving market dynamics.

More troubling than the immediate shortfall in revenue is Nike’s outlook for fiscal 2025, which paints an even grimmer picture. The sportswear giant anticipates a substantial 10% decline in sales for the upcoming financial year. Such bleak projections underscore persistent issues within the company’s operational strategies and market positioning. These forecasts naturally spooked investors who demand consistent growth and stability from leading blue-chip stocks like Nike.

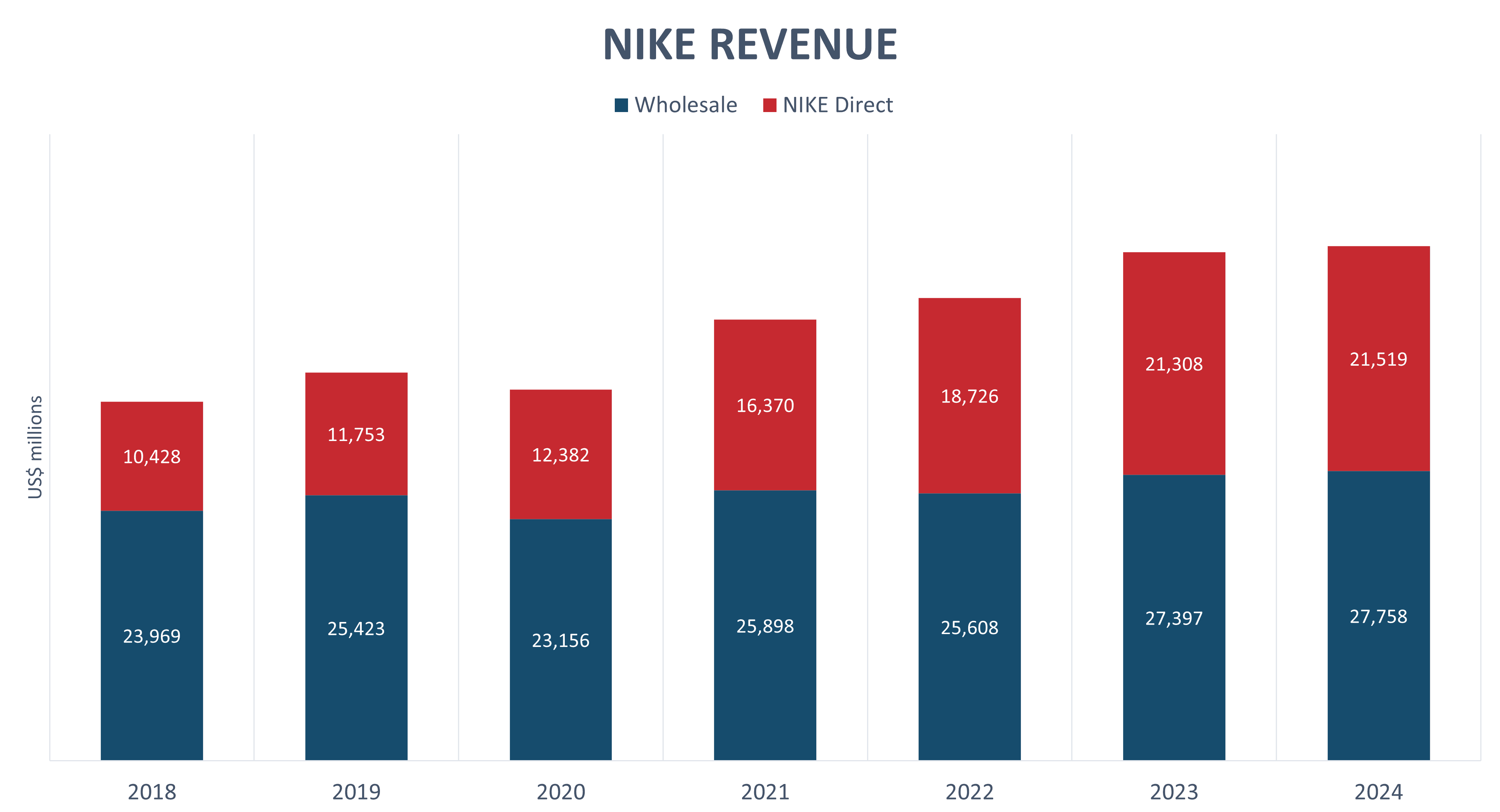

Management mishap

In late 2017, Nike strategically transitioned from its traditional wholesale distribution channels to a direct-to-consumer (DTC) model. This shift marked a significant departure from its previous business strategy, which had relied heavily on partnerships with retailers around the globe. The company believed focusing on DTC would enhance brand control, allow for a more personalised customer experience, and ultimately increase profitability by cutting out the middleman.

However, as Nike’s DTC model expanded over the years, it became clear that its wholesale business had stagnated, and overall results were mixed. By pulling back from established retail spaces, Nike decreased its visibility and accessibility for many consumers, ultimately leading to slowing sales figures. Furthermore, the strategy strained relationships with wholesale partners who played a crucial role in building Nike’s brand over the years. These partners often provided valuable market insights and broad distribution networks that helped Nike maintain a strong market presence.

Amid economic pressures, many consumers are also increasingly seeking flexibility and variety in their shopping experiences, turning to retailers like Amazon and Foot Locker that offer competitive pricing and a wider range of options, as opposed to shopping at a Nike store.

Competition

Compounding Nike’s strategic missteps, emerging athletic brands like Hoka and On Running have capitalized on the company’s retreat from key wholesale channels. These challenger brands have managed to capture critical market segments by leveraging innovative product technology and fresh, impactful marketing strategies that resonate strongly with today’s consumers.

In contrast, Nike’s own product lines have recently struggled to consistently adapt and meet evolving consumer preferences. New product launches have failed to generate the same level of buzz and customer excitement as hit offerings from rival brands, particularly in the running category where newer competitors are excelling.

Additionally, Nike’s once-powerful endorsement deals and marketing campaigns appear to have diminished in influence amidst a dynamic, heavily saturated competitive landscape. The brand’s traditional promotional approach seems less impactful as consumers are bombarded with a proliferation of engaging content from a diverse array of athletic and lifestyle brands.

Can Nike bounce back?

Despite the alarming drop in Nike’s stock price, investors should remember that this is not the first major setback the company has faced. Historically, Nike has demonstrated a robust ability to rebound from adversity. For instance, the brand’s stock took significant hits during the 2008 financial crisis and the COVID-19 pandemic, but subsequently recovered due to its resilient brand presence. Many sports apparel companies like Reebok and Under Armour have also attempted to challenge Nike’s dominance over the years, but Nike has remained dominant in its field.

Nike is now making strategic moves to re-embrace wholesale partnerships after pivoting towards a direct-to-consumer (DTC) strategy. CEO John Donahoe has acknowledged the need to be ‘where the consumer is’, and the company will adopt a more balanced approach to growing the entire marketplace rather than solely focusing on DTC. To strengthen relationships with wholesale partners, Nike has held summits to showcase its upcoming product innovation pipeline. The company is exposing its three-year roadmap to these partners and has received positive feedback, with a strong order book for the 2024 and spring 2025 holidays.

Nike is also enthusiastic about its multiyear innovation pipeline, with upcoming launches slated for the running, basketball, and lifestyle segments. Despite increasing competition from established brands like Adidas and Puma, as well as emerging players like On Running and Hoka, Nike maintains strong fundamentals. The company’s extensive athletic sponsorships, global brand equity, and legacy of pioneering products continue to bolster investor confidence in the long-term durability of the Nike brand.

Valuation

In examining Nike’s current trading valuations, the stock is currently undervalued relative to its historical intrinsic value. The company’s stock is trading at a trailing price-to-earnings (P/E) ratio of around 21, one of the lowest levels observed in the past two decades for a company that has consistently delivered solid growth. This relatively low P/E ratio suggests the market may be pricing in a gloomy near-term outlook, potentially due to predicted revenue declines in fiscal 2025.

Investors might see the current stock price volatility as an opportunity to objectively reassess Nike’s strategic shift, rather than a sign of the brand’s decline. If Nike can effectively address the overreliance on its previous DTC-focused strategy and find the right balance between direct and wholesale channels, the company is well-positioned to regain momentum and capitalize on emerging market trends.

The fifth perspective

While the company’s recent stock price volatility and strategic missteps warrant close attention, Nike’s long-term fundamentals remain strong. looks poised to weather the storm and maintain its position as the number one global sports and lifestyle brand. While near-term challenges may persist, the stock’s current valuation could offer a compelling opportunity for investors confident in Nike’s ability to navigate the evolving competitive landscape and deliver sustainable shareholder returns over the medium to long term.