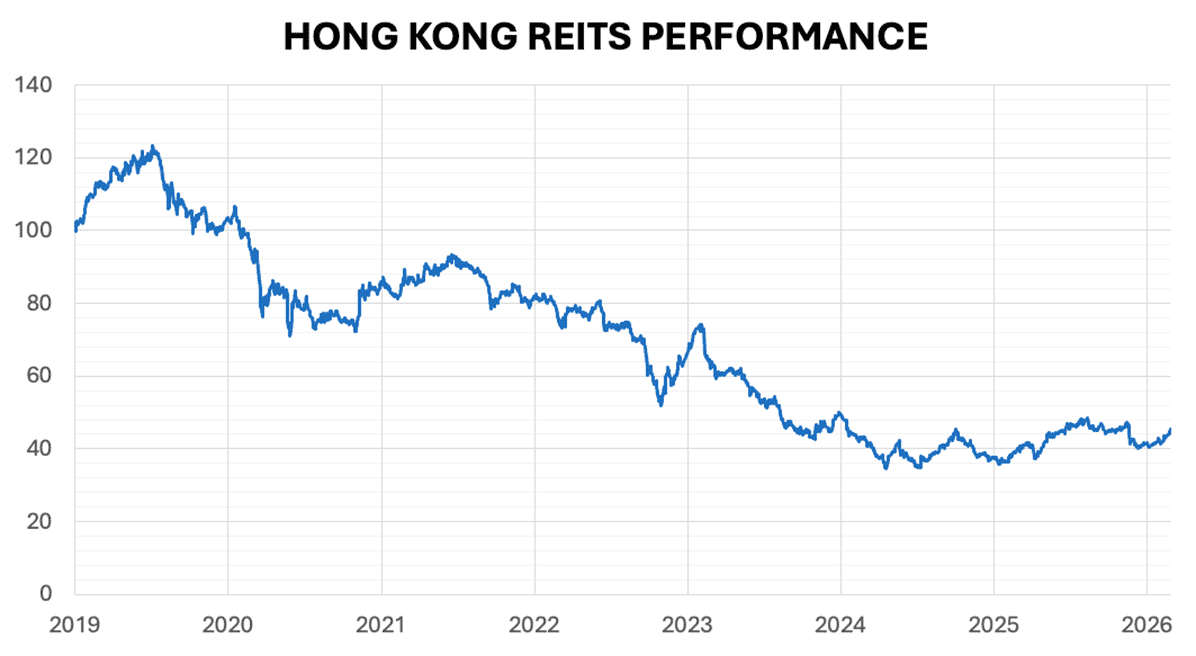

The Hong Kong REIT (HK-REIT) market in 2025 and early 2026 remains a story of deep value versus persistent structural headwinds. Unlike the sustained recoveries seen in Singapore and Malaysia, Hong Kong’s rebound has remained muted. This lackluster performance is primarily due to a broader macroeconomic slowdown. Even as the streets grew more crowded when I visited Hong Kong in 2025, tenant sales and the rental turnovers for REITs remained stubbornly below 2019 levels.

The retail sector is also grappling with a significant consumption leak as Hong Kong residents increasingly travel cross-border to Shenzhen for more affordable shopping and dining. Simultaneously, the office segment continues to struggle with a chronic oversupply of space, which has kept vacancy rates high, forcing landlords to offer aggressive incentives and flexible terms. Consequently, rental growth remains stagnant, with older or decentralized assets facing a persistent downward drift in valuations as tenants prioritize premium and high-specification buildings.

Investing in Hong Kong stocks since the 2019 protests has been challenging. HK REITs, in particular, have declined significantly, which has been discouraging for many investors. However, those who invested in these REITs since their IPOs may find their long-term results more resilient than expected.

If you are investing in REITs or dividend stocks (of which Hong Kong has many), I strongly suggest taking into account the dividends you have received when measuring your overall returns. This will give you a clearer perspective on overall performance.

This is what we have been doing when calculating investment returns for S-REITs and M-REITs since their IPOs. We will apply the same approach to Hong Kong REITs that have been listed for at least 10 years to evaluate their long-term performance, as short-term market movements are often driven by sentiment.

Once again, we assume that David (a fictional character) invests HK$10,000 in each Hong Kong REIT from its listing date. As a hard-core income investor, he does not inject additional capital to subscribe to any rights issues (if any) and accepts any resulting share dilution. We also assume that he does not sell his nil-paid rights, even though he could have made a profit from them.

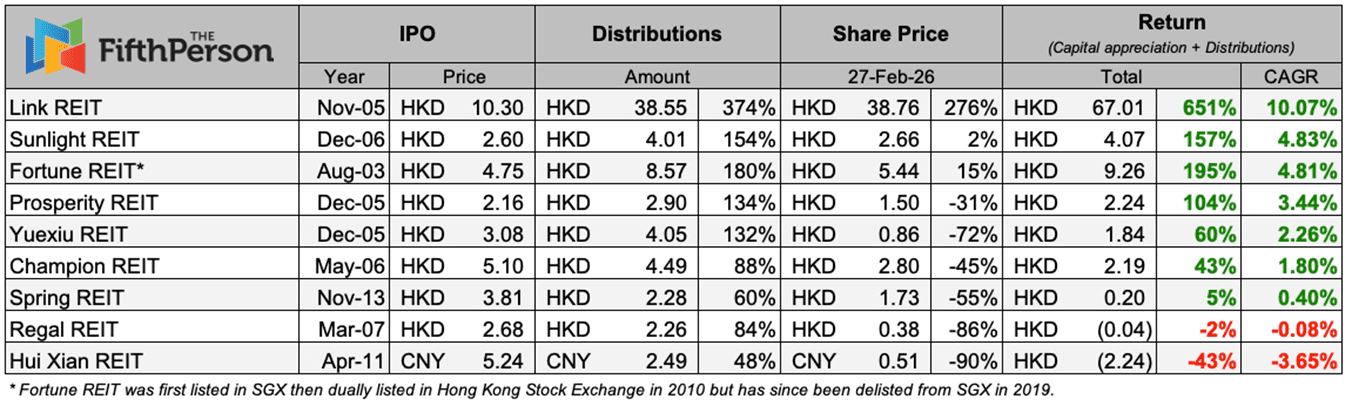

For example, if David had invested in Fortune REIT during its IPO, his initial investment of HK$10,000 would have increased slightly to HK$11,500 (+15% in capital gains) by 27 Feb 2026.

However, when we include the dividends he has received over the years, his total investment would have grown to HK$29,500 (+195% in total return). Overall, his annualised return in Fortune REIT from 2003 to 2024 is 4.81%. While the return is not exceptional, David still benefited from a steady stream of dividend income despite the challenging property market conditions.

If David had invested HK$100,000, his investment would have grown to HK$295,000. In essence, the more capital he invests, the greater his absolute returns. And the longer he holds, the more dividends he receives. After investing for more than ten years, here are the top three best-performing Hong Kong REITs for David.

Note: We’ve excluded brokerage costs, currency exchange gains/losses and taxes that might be applicable to foreign investors.

3. Fortune REIT (annualised return: +4.59%)

Since 2003, every HK$10,000 invested in Fortune REIT would have grown to HK$11,500. Including dividends, each HK$10,000 would have cumulatively increased to HK$29,500.

2. Sunlight REIT (annualised return: +4.83%)

Since 2006, every HK$10,000 invested in Sunlight REIT would have remained relatively flat at HK$10,200. However, including dividends, each HK$10,000 would have more than doubled to HK$25,700.

1. Link REIT (annualised return: +10.07%)

And the most prosperous REIT in Hong Kong is not Prosperity REIT, but Link REIT. Since 2005, every HK$10,000 invested in Link REIT would have grown to HK$37,600. Including dividends, each HK$10,000 would have cumulatively increased to HK$75,100!

In summary, here is David’s overall performance:

Similar to many Singapore and Malaysian REITs, Hong Kong REITs have generally delivered positive total returns—except for Hui Xian and Regal REIT. Hui Xian, for instance, declined by about 90% in terms of capital gains. However, when dividends accumulated over the years are included, the overall loss narrows to around 43%.

Due to weak sentiment in the Hong Kong and China markets, most REITs—apart from Link REIT, Sunlight REIT, and Fortune REIT—have recorded negative capital gains. But once dividends are factored in, the overall performance becomes much clearer. In many cases, dividends contributed the bulk of total returns, helping to offset capital losses.

It’s also worth noting that David did not inject additional capital to subscribe to any rights issues; the results above reflect his actual outcomes. His losses in Hui Xian could be offset by gains from his other REIT investments. That said, if he had participated in rights issues (where available), he could have achieved even better returns, as rights are typically offered at a discount.

Most importantly, David continues to receive regular quarterly dividend income from his Hong Kong REIT investments, rain or shine.

As you can see, REITs remain a compelling option for those looking to build a steady and consistent stream of passive income. However, it’s important not to buy or avoid a REIT based solely on past data, as historical performance is not necessarily indicative of future results.

Having a sound investment process is essential to help you identify and invest in the right REITs—ones that can deliver both sustainable income and potential capital growth over time.

???? Announcement: Enrolment for Dividend Machines closes this Sunday, 22 March 2026! If you’re looking to learn how to invest in dividend stocks and REITs while building multiple streams of passive income, we highly recommend checking out Dividend Machines before enrolment closes! Once the deadline passes, Dividend Machines won’t reopen until 2027. Start investing for cash flow today!