The war between the U.S. and Iran has rattled markets. Oil prices are spiking. Headlines are screaming about escalation. And your gut is telling you to sell everything and move to cash before things get worse.

Sound familiar?

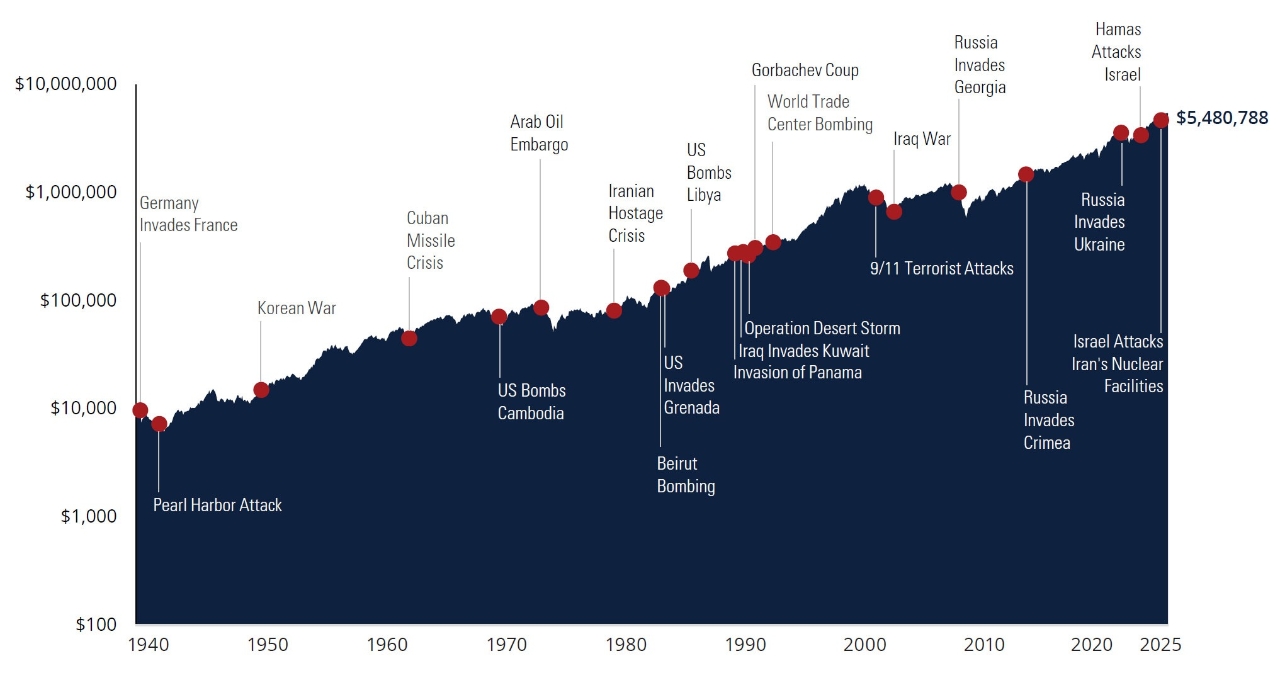

This happens every time a new conflict breaks out. It happened when Russia invaded Ukraine in 2022. It happened after 9/11. It happened during the Gulf War in 1990. Every single time, investors who panicked and sold their stocks, watched the market recover without them.

The truth is, while war is devastating on a human level, it has had remarkably little long-term impact on the stock market. And understanding why can help you avoid one of the most common and costly mistakes an investor can make: selling at the worst possible time.

The initial drop is scary, but it doesn’t last forever

When a war breaks out, markets sell off. That part is predictable. The stock market hates uncertainty, and the start of a conflict is about as uncertain as it gets. Nobody knows how long it will last, whether it will escalate, or what the economic fallout will be.

After 9/11, the S&P 500 fell roughly 12% in five trading days. When Russia invaded Ukraine, global markets sold off sharply. The Gulf War saw the S&P 500 decline about 17% in a matter of months. These are scary numbers. But they all have one thing in common: they were temporary.

After the Gulf War’s 17% drop, the S&P 500 ended 1991 up over 29%. After 9/11, the market bounced back more than 21% in just 10 weeks. And the S&P 500 has risen over 60% since Russia’s invasion of Ukraine. Historical data shows that stocks delivered positive returns within one year of 73% of all armed conflicts since World War II. The longer you stayed invested, the better your odds became.

Middle East conflicts and energy prices

Investors react to conflicts in the Middle East due to the potential impact on energy prices. Iran sits near the Strait of Hormuz, a narrow shipping channel through which roughly one-fifth of the world’s oil supply passes each day. Any escalation that threatens shipping routes, oil infrastructure, or regional stability can push oil prices higher in the short term.

Higher energy prices can increase inflation, raise transportation and production costs, and temporarily pressure global markets. However, history shows that these oil shocks are usually short-lived, with the effects vanishing after two years. Global energy markets adjust through increased production from other countries, strategic reserves, and demand changes.

Most wars today are local, not global

Modern wars are very different from the World Wars. In the 1940s, the entire global economy was upended. Factories across Europe and Asia were destroyed. Trade routes collapsed. Entire nations were occupied. That is not what is happening today.

Today’s conflicts, whether in the Middle East, Eastern Europe, or elsewhere, are geographically contained. They are devastating for the people caught in them. But localised conflicts are unlikely to reshape the global economy the way World War II did.

More importantly, these wars are not happening on American soil. The United States, home to the world’s largest and richest stock market, continues to operate with its infrastructure, technology companies, factories, and financial system fully intact. When you invest in the S&P 500, you’re investing in 500 of America’s biggest companies. Those companies are still running. Their employees are still going to work. Their customers are still buying products.

War may dominate the headlines, but it is not shutting down Apple, Microsoft, Amazon, or the thousands of other businesses that make up the U.S. economy.

Global business doesn’t stop

Think about your own daily life during a war overseas. You still go to work. You still pay your bills, buy groceries, use your phone, and stream shows in the evening. Billions of people around the world are doing the exact same thing. The overwhelming majority of global economic activity simply carries on.

The companies in the S&P 500 are also global businesses. A regional conflict might disrupt one supply chain or one market, but these companies are diversified across the entire world. They’ve been through this before, and they’ve adapted every time.

At the end of the day, the most important driver of stock prices is corporate earnings, and wars have typically had very little impact on the ability of most companies to make money. Even during the Russia-Ukraine war, which disrupted energy and food markets significantly, the S&P 500 recovered and went on to hit new all-time highs.

The risk of emotional investing

During wartime, it’s natural for investors to focus on the conflict as the biggest threat to their portfolio. But history suggests that emotional reactions to uncertainty often do more damage than the conflict itself.

When you sell during a panic, you lock in your losses permanently. Then you sit on the sidelines waiting for things to “feel safe” again. But by the time the news improves and you feel comfortable buying back in, the market has already recovered, and you’ve missed the best days.

The data backs this up. Investors who exit the market during negative headlines almost never come back in at the right time. Some of the strongest trading days in history have occurred right in the middle of the worst crises. If you’re not invested on those days, you miss them entirely.

Research has also shown that once a conflict is underway, it transforms from an unknown fear into a measurable risk. Investors begin to price it in, adjust their expectations, and move forward. The market doesn’t need good news to rise; it just needs less uncertainty.

That’s why the S&P 500 fell 12.3% in the three months before the U.S. entered World War II, but returned 16.9% over the entire war. The anticipation was worse than the event itself.

What should you do?

1. Stay invested. The data from every major conflict in the past 80 years points to the same conclusion. Selling during the fear has historically been a losing strategy. Holding through the volatility has not.

2. Turn off the noise. 24-hour news coverage is designed to keep you watching, not to help you make good investment decisions. The more war headlines you consume, the more likely you are to make an emotional decision you’ll regret.

3. Remember what you own. If you’re invested in the S&P 500 or a diversified index fund, you own shares in companies that have survived many wars, recessions, and crises of the past century. These businesses are not going away because of a regional conflict on the other side of the world.

4. Consider buying, not selling. When the market drops 10-15% because of geopolitical fear and the underlying economy hasn’t changed, quality companies are essentially on sale. Some of the best long-term returns in stock market history have been earned by investors who bought when everyone else was running for the exits.

The fifth perspective

War is a human tragedy, and nothing in this article should make light of that. But as an investor, you owe it to yourself to separate emotion from evidence.

The evidence is clear: the S&P 500 has risen through every major conflict in modern history. Today’s wars are localised, not global. Corporate earnings, the real driver of stock prices, remain largely unaffected.

The initial volatility is real and frightening. We cannot predict how the Iran war will unfold or how energy prices will move in the short term. But history reminds us to stay calm, stay invested, and trust that time in the market beats trying to time the market.