One of the major threats to a retirement fund is inflation. With rare exceptions, the cost of living will always increase — you could buy a satay stick for one cent in the 1960s and those of us who grew up in the 1980s will remember how a big a sum $500 used to be. As such, a lot of people who make sweeping statements — such as “I’ll only need $1,000 a month to survive” — may be far off the mark.

Here’s a look at how much your lifestyle might cost in 2047.

In the following example, we will work out the cost of items today and how they would change by 2047. This follows an assumption that the overall rate of inflation is 3%. This is more or less in line with Singapore’s core inflation* over the past decade and most developed countries have a comparable rate of inflation. (*Core inflation excludes the rising cost of private transport and private housing.)

Here’s the formula: Principal x (1 + inflation rate)^number of years

So let’s assume you’re 35 years old today. By 2047, you will be 65 years old, retired, and getting around $1,300 a month from CPF payouts — which is what many Singaporeans will get from CPF LIFE if they have the full retirement sum of $166,000.

Is that enough come 2047?

Essential expenditures

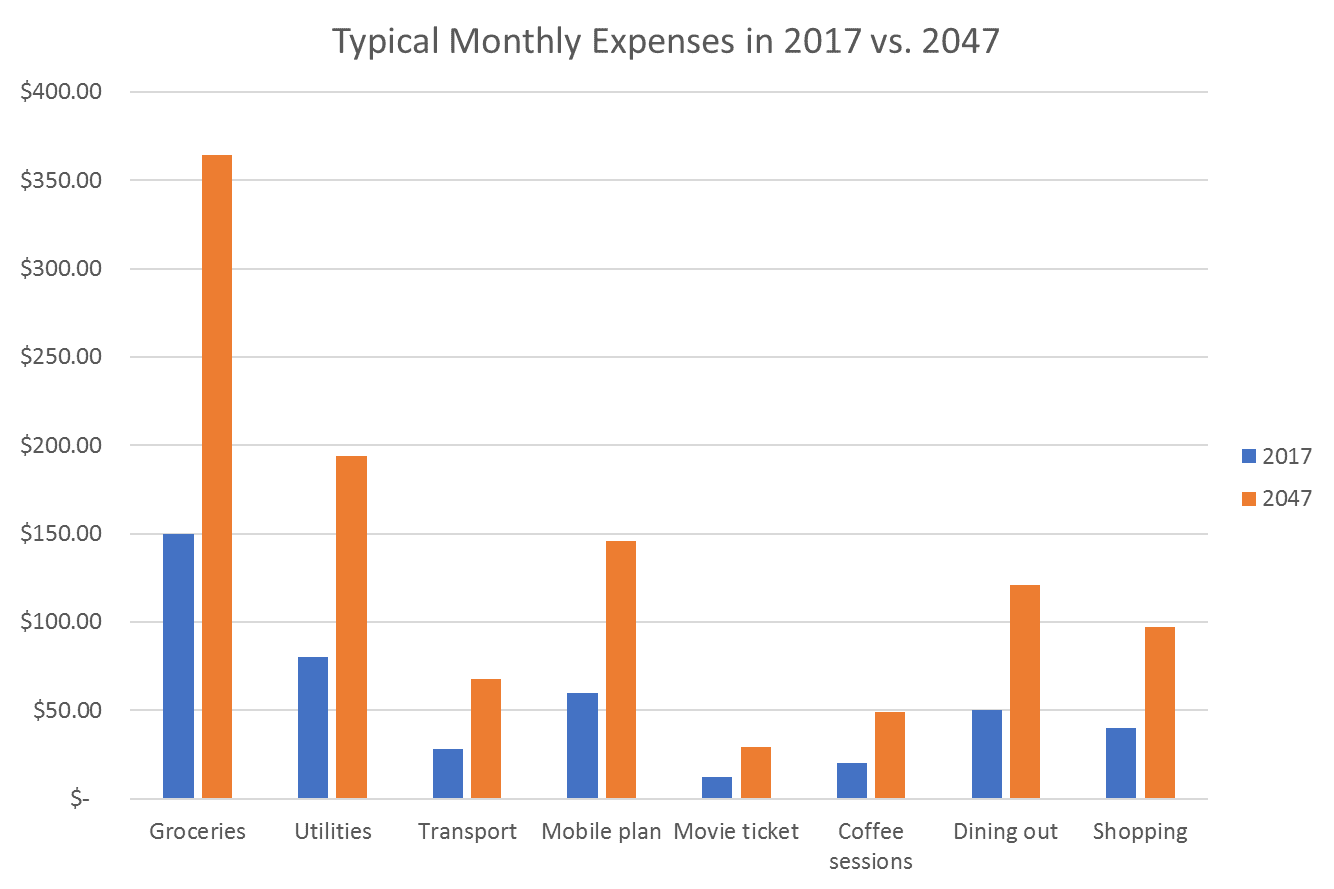

Let’s look at your basic essentials first:

One month of groceries

Current cost: $150 and we’ll assume that’s enough to give a single person three meals a day for the entire month.

Projected cost in 2047: $364

Utilities

Current cost: $80 per month for a single person in a three-room flat

Projected cost in 2047: $194

Public transport costs

Current cost: Most people spend around $14 a week on public transport. But we will factor in senior citizen concessions and the fact that you may not travel as much. Let’s halve it to $7 a week which makes it $28 a month

Projected cost in 2047: $68 per month

Mobile phone plan

Current cost: $60 per month

Yes, we will assume that having a mobile plan with data is an essential since this generation can’t live without their phones anyway.

Projected cost in 2047: $146

Total for essential expenditures in 2047: $772

Seems like a lot? Let’s look at some more expenses.

Typical leisure expenses

We’re going to assume you don’t go on big adventures abroad and mostly stay within the neighbourhood.

Let’s say you…

Catch a movie once a month

Current cost: $12 for a ticket. We assume cinemas still exist in 2047 even with Netflix on the rise.

Projected cost in 2047: $29

Lim kopi session with friends once a week

Current cost: $5 for two cups of coffee and maybe one plate of food. So about $20 a month

Projected cost in 2047: $49

Dining out once a month

Current cost: $50 for a three-course meal at a decent restaurant.

Projected cost in 2047: $121

Shopping

Current cost: Let’s assume you buy a book or a new t-shirt on occasion. About $40 a month as a conservative estimate.

Projected cost in 2047: $97

Total for leisure expenses in 2047: $296

Assuming that you only receive $1,300 from your CPF LIFE, that leaves you with around $232 after accounting for essentials and everyday leisure expenses. With that amount left, let’s see what you can afford to enjoy and have fun with during your golden years.

Travel and entertainment

Return ticket to Thailand with hotel accommodation for one week

Current cost: A budget ticket might set you back about $250 and a decent hotel would be around $100 a night. Add around $50 a day for spending, so a simple week-long vacation in Thailand would be $700.

Projected cost in 2047: $1,700

Wow! That’s more than your entire month’s payout. Okay scrap that idea. We’ll need to save up for months before we can have some authentic pad thai. Let’s look at something else…

A three-day staycation at a boutique hotel in Singapore

Current cost: A single night at a chic boutique hotel costs around $250 a night. So a three-day, two-night staycation would set you back $500. Slight cheaper than a week in Thailand — and you get still to lim kopi with your friends in the morning.

Projected cost in 2047: $1,214

Crap. That’s still way over budget. Need to save up some more before we can even do a staycation. How about…

A day with the family at Universal Studios Sentosa

Current cost: $38 for a senior citizen (and assuming rest of the family pay for themselves)

Let’s assume you also buy a nice meal while you’re there which runs to about $20. You’ll probably also buy a souvenir or something for your grandchild, so let’s say that costs $40. Altogether you’ll spend about $98 for a day in Sentosa.

Projected cost in 2047: $234.

Yes! We just have enough to pay for ourselves to spend a day at Universal Studios with the family. (We actually only have $232 left over after all our monthly expenses but we can probably find two dollars from the drawer somewhere!)

Conclusion

As you can see, $1,300 from CPF alone buys you a fairly spartan lifestyle in 2047. A meal at restaurant once a month, a movie, and coffee shop sessions with your friends – and you have barely enough left over for a day at Sentosa.

While there’s absolutely nothing wrong with a simple lifestyle, the question is: Is this enough to retire on? We haven’t even factored in medical expenses and emergencies.

So even a small increase in your post-retirement income of a few hundred dollars can be life-changing. If you build a balanced portfolio of value-growth and dividend-paying stocks today, you could easily have another $300-500 a month (or more) to complement your CPF payouts.

You could afford more holidays and continue to enjoy the hobbies you have right now. You could treat your grandchild or help your children in a bad patch without needing to count pennies.

Do consider if that’s worth investing a little more today.

(Editor’s note: This example assumes the CPF Full Retirement Sum and monthly payouts remain at $1,380 and are not revised upwards. If the retirement sum is revised upwards, the payouts will likewise increase.)

A very good article. Eye opener for many.

Indeed!

Another major cause of insufficient savings for retirement years in addition ot inflation, may include the WANTS OF PEOPLE WHICH ARE UNLIMITED AND CAN BE CONTROLLED BUT NOT DUE TO POSSIBLE ADDICTION. COST OF NEEDS WILL GO GO UP BUT CAN BE MANAGED. Some examples can include:

[a] a phone may be a need but a simple one costs little but the greed for expensive ones and then replacing them with latest models is a a waste of funds as the existing ones serve the needs.It is commonly perceived that over 90% of the features are never used and this is human train where the brain is used less than 90%.

[b] Transport may be need which can be satisfied by public transport or a small car but the WANT IS EXPENSIVE MERCEDES or other high end modesl.

[c] Cost of food is cheapest when cooked at home but this cost goes higher according to the type of place where one drinks or eats as as the costs include for services/facilities not used.

[d] Condo occupants have to pay for swimming pool maintenance even if the persons may not know how to swim and thus not use.

SAVINGS WAS NEXT TO GODLINESS BUT NOW IT IS A SIGN OF STUPIDITY AS IN SOME COUNTRIES SAVINGS ARE TAXED. On the other hand ALL ARE URGED TO FOLLOW GOVERNMENTS AND BE IN PERMANENT DEBT [CRE CARDS/CAR-HOUSE LOANS/borrowings]

and if not paid the Authorities will guide one on how to delay or even in some cases to default and let the loans be written off. LEADERSHIP BY EXAMPLE AS 99.9% OF GOVERNMENT HAS NEVER AND NEVER WILL PAY PUBLIC DEBT BUT CONTINUE TO INCREASE.

Modern Capitalistic System Economy designed by experts for self enrichment and thus may be among the biggest frauds of modern times.

is the 1300 tax exempt?

u hv left out sncc (hdb)which is essential

Hi Jo,

For this example, we assume that your HDB/home has been fully paid by that point.

one more thing, re transport, I don’t tink u shd take into a/c snr concession bc wont know if there will b such a thing come 2047. for cal purpose, shd use normal fare structure

Then you can simply double the figure listed 🙂

oh jz realize tat at 1300 per month, one is not likely to hv to pay tax.

The first part of the calculation is already wrong. $150 for 3 meals a day for the entire month? Which means, $5 a day for 3 meals? How is that possible. It should be $450 a month if you think about it. So with what you call as inflation rate I believe it would be about $1000 in 30 years time.

Hi Carly,

If you read, the $150 is for groceries for cooking/eating at home.

If that’s not enough, it only shows how little $1,300 a month is for retirement and why investing today is so important 🙂

You have forgotten about health issues.

Increasing age means increaseing health problems. More money needed to maintain health or for hospitalisation/outpatient bills which maybe unforeseen.

Paying for shield plans ?

Yes, this was quoted in the article.

“While there’s absolutely nothing wrong with a simple lifestyle, the question is: Is this enough to retire on? We haven’t even factored in medical expenses and emergencies.”

Life styles should be based on ‘Needs’ which can provide sufficient savings for retirement periods. Most spend while earnings on the assumption that there is no tomorrow and then complain even though the writings is not only on the wall but the well explained by all including the current elderly and yet do not want to learn in spite of their high literacy rates be it acquired from local or UK/US universities.

May be this may be one reason why many high profile professionals in many countries are turning to fraud and corruption.

Quote:

“While there’s absolutely nothing wrong with a simple lifestyle, the question is: Is this enough to retire on? We haven’t even factored in medical expenses and emergencies.”

Un-qoute:

There is a phrase that we always heard:

“One can afford to die but cannot afford to fall sick”.

However, before the last recourse above, one can consider to look for 2nd, 3rd or even multiple sources of passive income via various investment instruments. In my humble opinion, this website is one of the many sources for investment ideas.

Most of the sicknesses are urban diseases and so are the components of lifestyles. May be better to retire in some rural areas where the conditions are healthier and needs are limited. In Singapore you need at least SD5K for decent retirement but in smaller towns of Malaysia the need may be less than RM5K [SD1.7K] ONE SHOULD NOT HAVE CITY LIFESTYLE UNLESS ONE CAN AFFORD AS IT WOULD BE BETTER TO MIGRATE TO A CHEAPER AREA IF FUNDS ARE LIMITED.