Mapletree Commercial Trust (MCT) is an SGX-listed REIT that owns a portfolio of retail and office properties in Singapore. As at 31 March 2018, MCT’s property portfolio was valued at S$6.7 billion.

As an MCT unitholder, the REIT has given me steady dividends and capital gains over the last few years, driven mainly by the consistent performance of VivoCity and the acquisition of Mapletree Business City I (MBC I).

I attended MCT’s annual meetings in 2016 and 2017 where the management reported solid growth and a strong set of results each time. Will it be third time lucky this year?

Here are seven things I learned from the 2018 Mapletree Commercial Trust AGM:

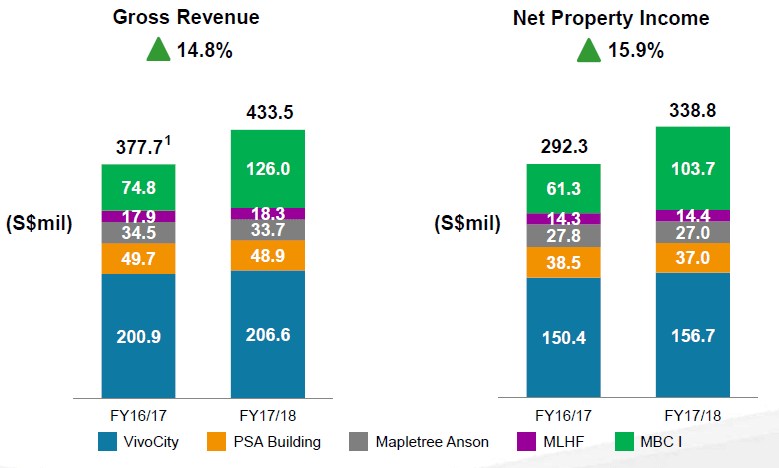

1. Gross revenue grew 14.8% year-on-year to S$433.5 million and net property income grew 15.9% to S$338.8 million. This was mainly due to a full-year contribution from MBC I, and higher contributions from VivoCity and Merrill Lynch HabourFront. VivoCity remains the largest revenue contributor at 47.7% of total revenue.

Source: Mapletree Commercial Trust 2018 AGM presentation slides

2. Distributable income grew 14.6% year-on-year to S$260.4 million and distribution per unit (DPU) grew 4.9% to 9.04 cents. Based on its latest annual DPU and MCT’s share price of S$1.61 (as at 20 August 2018), its current distribution yield is 5.6%. To get the latest yield for MCT and other Singapore REITs, you can check out Singapore REIT data.

3. Gearing level is 34.5% as at 31 March 2018 — 180 basis points lower than the year before. Its current gearing ratio leaves MCT with a debt headroom of S$1.2 billion. 78.9% of borrowings are at fixed interest rates and average cost of debt is 2.75%. Average term to maturity is 3.9 years.

4. Committed occupancy rate for the portfolio is 99.5% as at 31 March 2018. Portfolio weighted average lease expiry is 2.7 years. At VivoCity, tenant sales grew 0.7% year-on-year to a record S$958.2 million and shopper traffic grew 1.4% to 55 million shoppers.

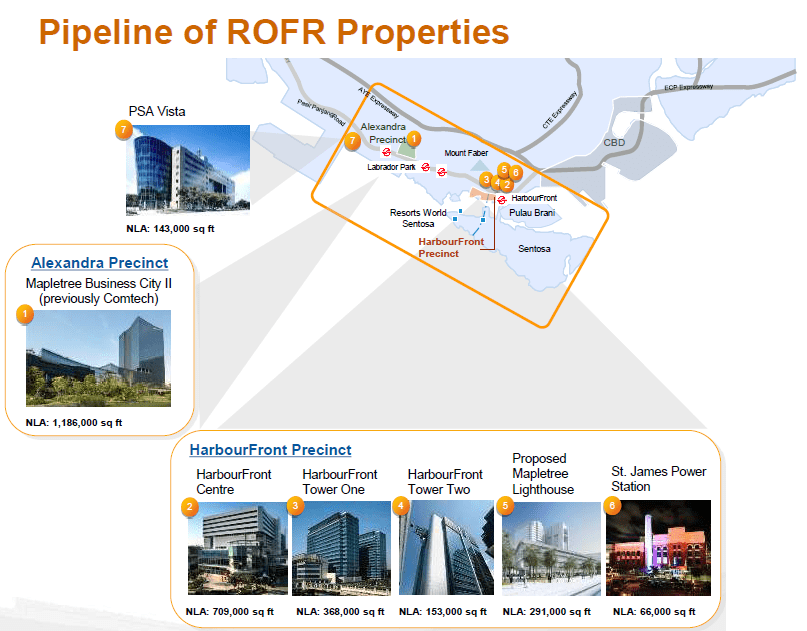

5. A unitholder was concerned about the recent moves by many Singapore REITs to invest overseas. He personally preferred a REIT to focus on one singular market/currency as he could geographically diversify his portfolio on his own. He wanted to know if MCT had any plans to invest overseas. Chairman Tsang Yam Pui first clarified that MCT’s investment mandate has no restrictions on investing overseas. However, as a matter of strategy, the REIT remains focused on Singapore. MCT’s pipeline of ROFR (right-of-first-refusal) properties from its sponsor are all based in Singapore and there is no need consider foreign assets for the time being.

Source: Mapletree Commercial Trust 2018 AGM presentation slides

6. Another unitholder was worried about the trend of malls closing down in the U.S. due to the rise of e-commerce and wondered if MCT, and VivoCity in particular, would be affected. CEO Sharon Lim said that VivoCity has the ‘right ingredients’ to compete with the threat of e-commerce: The mall is Singapore’s largest at 1.07 million square feet and is able to offer a complete trade mix that caters to the entire family due to its size. It is well-connected with an MRT station below and bus interchange nearby. The Sentosa monorail is connected to the mall and the Sentosa cable car is located close by. During weekdays, the mall benefits from the office crowd from the surrounding Alexandra precinct. Due to these factors, VivoCity has seen consistent growth in tenant sales and shopper traffic and the CEO believes the mall is well-equipped to navigate the threat posed by e-commerce.

7. A unitholder shared that Twenty Anson was recently sold at S$516 million (at 19.2% above valuation and a cap rate of 2.5%) and wanted to know if MCT would consider selling Mapletree Anson if it received a similarly high offer. The CEO said the board had not considered selling the property. Valued at $2,123 per square foot, it is the most expensive asset on a per square foot basis in MCT’s portfolio.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

Hi Adam,

I recently took positions in MCT. The growth potential of this stock is near insane level. With today surge to of 3% to $2.03 per share, what is your take on this reit at its current value? I intend to buy more in the next few months or so , but I’m afraid it might be overvalued.

Would Appreciate your advice.

Hi Chris,

I’m not one to give direct advice but I think MCT is overvalued at the moment, when comparing its current P/B to its historical averages.