Real estate investment trusts (REITs) are a long-time favourite among income investors. REITs typically pay a relatively high and stable dividend as they must distribute 90% of their income to unitholders.

At the same time, REITs are also a leveraged instrument; they will typically employ a certain level of debt to purchase property. In Singapore, a REIT is allowed to borrow up to 50% of its property portfolio value. But with debt comes risk. The more debt a REIT has, the riskier it becomes. A REIT must be able to service its interest payments and loan obligations on time in order to avoid a default. In recent years, there have been examples of REITs defaulting on their loans and suspended from trading.

However, with interest rates rising in an inflationary environment now, is it still wise to invest in REITs?

How interest rates affect REITs

Since REITs normally have some level of debt on their books, a rise in interest rates will mean that REITs will face a higher interest expense. This has a negative impact on income and could potentially affect a REIT’s dividend. For REITs that are highly leveraged, a spike in interest rates can be a problem – especially if the REIT has a high proportion of its debt at floating interest rates.

Knowing this, one could expect the prices of REITs to underperform during periods of high interest rates. But is this true?

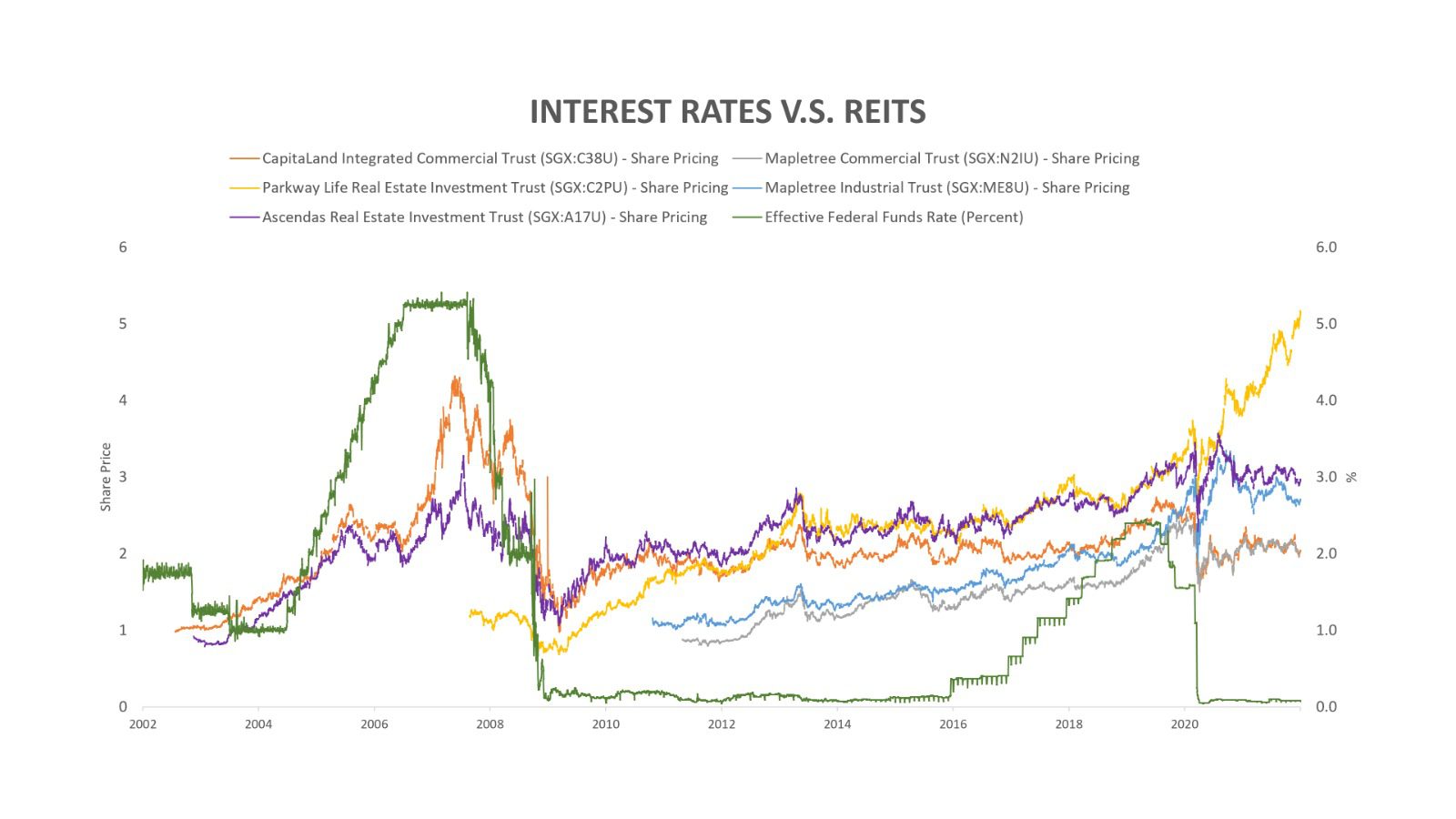

To find out, we selected a list of Singapore REITs with a longer listing history and compared their price performance against the U.S. federal funds rate (since U.S. interest rates largely affect Singapore’s domestic interest rates).

As you can see from the chart above, the unit prices of S-REITs actually have a positive correlation with interest rates. And this relationship is also true in the U.S. But why is this so?

To understand why REITs seem to do well during periods of high interest rates, we must first consider the reason why interest rates go up. The U.S. Federal Reserve usually raises rates when the economy is heating up and inflation starts to escalate. A growing economy points to higher demand for real estate which supports higher occupancy rates and higher rents. This leads to higher REIT income and dividends, which eventually pushes REIT prices up.

However, not all REITs will have the ability to raise rents all the time. It’s important to pick REITs that own a portfolio of high-quality properties that will attract sizeable demand during a growing economy.

So how you identify a high-quality REIT?

Quality, quality, quality

The more famous expression when it comes to real estate is: ‘Location, location, location.’ For a REIT, quality is the key when it comes to picking an investment. Here are some factors for you consider when evaluating a REIT for your portfolio.

1. Sector dynamics

REITs operate in different sectors including retail, office, industrial, healthcare, and hospitality. It’s important to understand the macro factors that influence a particular sector and, therefore, a REIT’s performance.

For example, hospitality REITs underperformed during the COVID-19 pandemic as global travel practically ground to a halt for two years. A REIT could own a portfolio of the best hotels in the world, but still struggle to fill enough rooms. On the other hand, industrial REITs that own a portfolio of data centres did extremely well as consumer habits shifted online and the demand for digital services boomed during the pandemic.

2. Quality of real estate assets

A high-quality property is one that can attract high and steady demand from tenants over the long term. For example, a retail REIT should ideally own malls that are well-located, easily accessible, and see consistently high shopper traffic.

A good way to gauge tenant demand is to have a look at a property’s occupancy rate. A long-term track record of consistently high occupancy rates (>95%) is a good indicator that a property is high in demand among tenants. So even if one tenant were to leave, a new one is ready to take its place. It’s also good to check if the property is charging market (or above market) rents to ensure that the demand isn’t artificially boosted by lower prices.

3. Gearing ratio

Like we mentioned above, REITs typically borrow money to purchase properties and it’s important that the amount of debt is at reasonable levels. In Singapore, a REIT is allowed to borrow up to 50% of its property portfolio value. In practice, most Singapore REITs have leverage ratios around 30-40% which gives them more headroom to manage their debt.

It’s also good to note the proportion of loans that are at fixed or floating interest rates. A REIT with a higher proportion of floating interest rate debt is more vulnerable to spikes in interest rates which could impact its income and dividend.

4. Growing distribution per unit

Most people invest in REITs for their dividend (or distribution). So the litmus test for a well-performing REIT is its ability to pay a steady and growing distribution per unit to investors. A multiyear track record of higher DPUs is often a good sign that a REIT is well-managed and able to increase its property income through good acquisitions and/or higher rents over the years.

5. Distribution yield

Distribution (or dividend) yield measures the amount of DPU paid as a percentage of unit price. One of the biggest mistakes new investors make when it comes to investing in REITs is that they tend to focus on high yields alone.

In simplest terms, the higher the yield, the more attractive the REIT. But this is rarely true, because in many cases an extremely high yield typically points to a risky investment. The simple explanation is because high-yield REITs are unusually high for a reason – no one wants to buy them.

For example, a REIT that’s facing serious financial difficulties would lead to investors avoiding and selling its units. This causes the unit price to fall. And a lower unit price gives you a higher yield. The problem is that the REIT is unlikely to maintain its distribution due to its financial difficulties. So even if the high yield looks really enticing right now, it may drop very soon!

On the other hand, a successful REIT has more investors buying its units. This causes its unit price to rise. And a higher unit price equals a relatively lower distribution yield. At the same time, too low a yield may indicate that a REIT is currently overvalued. It’s useful to compare a REIT’s current yield with its historical yields to give you an indication of where it stands in terms of valuation.

The fifth perspective

The above points are not meant to be exhaustive, but they are a good place to start your research. REITs are a steady investment that historically tend to well during inflationary periods. At the same time, not all REITs are equally well-equipped to handle the rise in interest rates. Quality is key when it comes to picking the right REIT investment.

Many investors are wondering what’s in store in 2023 for their investments. Investors have been asking us on the outlook for many different markets – should I continue to have faith in Asian equities? Should I put more money into safer havens such as Singapore Government Securities (SGS) or Singapore Treasury Bills (T-bills)?

With the outbreak of a Russia-Ukraine war that is still ongoing in Europe, supply chain and global energy issues that have pushed inflation to levels not seen in decades. There is the possibility of more tensions in the US-China relationships going forward and their ramifications for global markets.

In attempts to tame inflation, numerous central banks around the world have had to tighten monetary policy over the past year. The low interest environment that had been present since the last global financial crisis, now seemingly belongs to a bygone era. It Is likely that high interest rates and inflation look set to stay with us for some time yet. With the many troubles affecting the global economy, and economic data painting a mixed picture, further fears surrounding a recession are on the rise.

At FSM Invest Expo 2023, we will revisit the important investment principles and concepts that investors cannot afford to ignore, and which have stood the test of time through various macroeconomic conditions.

Join us on 7 January 2023 at Suntec City Convention Centre, Hall 403, in Singapore! Hear from our line-up of speakers and speak with industry experts to gain insight into the markets. Find out what’s different, and what is not, and discover some of the strategies and opportunities that you can tap into in order to continue investing globally and profitably. Register now!

I remember attending the Fifth Person “Dividend Machines” course back in 2016. Personally, I think almost anybody considering investing in Singapore REITs would benefit tremendously from it before they buy any shares in a REIT or dividend stock.

Too many of the people I see investing in REITs just look at the dividend yield, and they don’t consider the risk factors that are associated with that particular company. In Singapore, a lot of people also talk about the dividends or yield “giving” rather than PAYING. Every investor needs to grasp the concept that investments don’t “give” anything, you’re being PAID for risking your hard-earned money when you invest. The good thing is that it’s not difficult to analyze REITs, and the information and data that we need to consider are easily and freely available. The individual investor just needs to understand how to use it.

Agreed, Jonathan! REITs are relatively simple to understand (compared to businesses and their various moving parts) and a great way to build a portfolio for passive income.

The article totally missed the point that current inflationary trend is not because of real economic growth, but rather due to the over printing of money during the covid pandemic. REITs doing well during real growth vs during artificial growth (as a result of free money policy) is a very big difference.

This is a really good point. Thanks for highlighting it!

We also think that the current inflation is due to demand returning — and surpassing — pre-Covid levels, while supply is struggling to keep up after downsizing during the pandemic. Demand can turn on in an instant, but supply chains take time to (re)build. We cover more about this here: https://fifthperson.com/demand-supply-lag-inflation/

So our opinion is that the demand/growth is real as the economy returns to normal. But lagging supply chains, the war in Ukraine (sending food and energy prices up), and printing of money have all contributed to the inflation we see now.