Last year, I wrote an article on Hartalega Holdings Berhad when the nitrile glove manufacturer had a market capitalization of RM11.7 billion. Today, Hartalega has a market capitalization of RM20.2 billion, a remarkable growth of 72.6% over the last 12 months. Hence, it remains amongst the top three largest rubber glove manufacturers in the world.

In this article, I’ll bring an update on Hartalega’s financial results, its ongoing development of its Next Generation Integrated Glove Manufacturing Complex (NGC), and introduce a few valuation metrics to assess Hartalega as an investment at its current stock price. Here are 12 things you need to know about Hartalega before you invest.

Track record

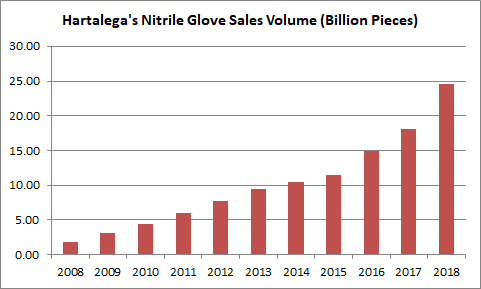

1. Hartalega has achieved a compound annual growth rate (CAGR) of 29.46% on sales volume for nitrile gloves for the last 10 years, increasing from 1.86 billion pieces in 2008 to 24.60 billion pieces in 2018. The rise in sales volume is in line with Hartalega’s ongoing efforts in expanding its production capacity over the decade. This includes the commissioning of Plants 4, 5 and 6 at Bestari Jaya, Selangor from 2008 to 2014 and Plants 1, 2, and 3, at the NGC, Sepang, Selangor from 2014 to 2018.

Source: Annual Reports of Hartalega

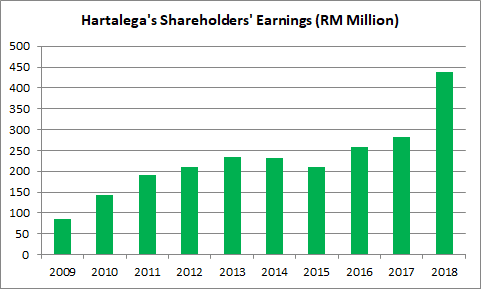

2. Hartalega has achieved a CAGR of 20.69% in revenue over the past 9 years, increasing from RM443.2 million in 2009 to RM2.41 billion in 2018. Its sales growth is in tandem with its rapid increment in sales volume for nitrile gloves during the period. As a result, Hartalega has reported continuous growth in shareholders’ earnings, from RM84.5 million in 2009 to RM438.9 million in 2018.

Source: Annual Reports of Hartalega

3. From 2009 to 2018, Hartalega generated RM2.37 billion in cash flows from operations. It raised RM531.14 million in net equities and long-term borrowings. Out of which, Hartalega has spent:

- RM374.43 million in property, plant & equipment

- RM1.64 billion in capital work-in-progress

- RM961.46 million in dividend payments

This means, Hartalega is a cash-producing business and doesn’t need to continually raise equity or debt to expand its operations or reward its shareholders with dividends.

4. As at 31 March 2018, Hartalega reported its non-current liabilities to be at RM221.0 million. Thus, its gearing ratio works out to 0.11. The company is in a net cash position of RM156.6 million and has a current ratio of 2.09. It is an improvement from a gearing ratio of 0.14 and a net cash position of RM120.3 million from a year ago (as at 31 March 2017). This is important as Hartalega needs capital to for the development of NGC which is explained below.

Next-Generation Integrated Glove Manufacturing Complex

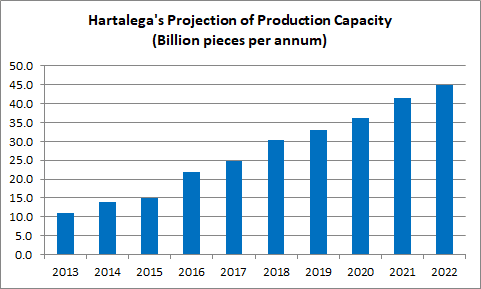

5. In 2014, Hartalega commenced on an eight-year master growth plan known as the NGC. Located at Sepang, the original plan of the NGC comprises the development of six manufacturing plants which house 12 production lines capable of producing 4.7 billion pieces of gloves annually per plant. Combined, the NGC would increase Hartalega’s glove production capacity from 14 billion pieces in 2014 to 42 billion pieces by 2022 upon completion.

6. Based on its latest Q4 2018 report, Hartalega has commissioned all 12 production lines at Plant 4. Hence, the first four plants — Plant 1, 2, 3, and 4 — are now fully operational. As at 31 March 2018, the company has an installed manufacturing capacity of 32 billion pieces of gloves per annum. Hartalega started construction of Plant 5 in July 2018, with Plant 6 soon to follow. The board has also confirmed its plan to introduce Plant 7 at the NGC – an additional plant to the original plan. Plant 7 is tailored towards smaller and specialty orders and has a glove manufacturing capacity of 2.6 billion pieces annually. Upon its completion, Hartalega’s glove production capacity will exceed 44 billion pieces per annum. The production lines equipped at the NGC are state-of-the-art and can produce an average of 45,000 pieces of gloves per hour. They are 1.8 times more efficient than Hartalega’s existing 55 plants at Bestari Jaya where their average output is 25,000 pieces of gloves per hour.

Source: AGM Investor Presentation and Q4 2018 report

7. Hartalega is in the process of upgrading its Enterprise Resource Planning (ERP) system to reduce cost and wastage during its manufacturing process. Costing RM14 million, the ERP system will be first piloted in plants at the NGC by end of 2018. Subsequently, it plans to implement them in plants at Bestari Jaya in 2019.

Research and development

8. In 2018, Hartalega made a breakthrough in its R&D efforts as the company developed the first non-leaching antimicrobial glove in the world. It was jointly developed with UK-based antimicrobial R&D company, Chemical Intelligence. The new gloves contain an active molecule which quickly kills any existing microorganisms on the external sides and are better at preventing healthcare-associated infections (HAIs) compared to conventional rubber gloves. Hartalega invested over US$10 million to develop the gloves and has launched it in the UK. Subsequently, the company is currently working to secure U.S. Federal Drug Administration approval to launch the product in the U.S. market.

Valuation

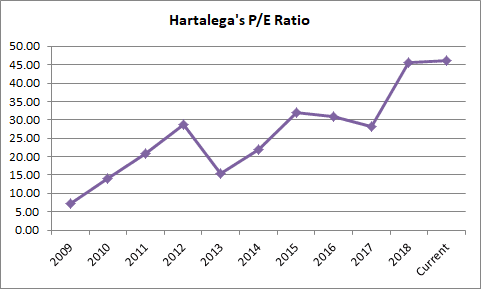

9. P/E ratio. As at 16 August 2018, Hartalega’s stock price is trading at RM6.78 per share. Its latest earnings per share is 13.3 sen. Therefore, Hartalega’s current P/E ratio works out to 51.1 — the highest it has been over the last 10 years.

Source: Data obtained from Hartalega annual reports

10. PEG ratio. Some investors may view that it is okay to buy stocks with high P/E ratios as long as they are still growing fast. To allow for this, we have to use the PEG ratio to determine a stock’s value in relation to its P/E and earnings per share (EPS) growth. The PEG ratio is calculated by taking the stock’s P/E divided by its EPS growth rate. A PEG ratio below 1.0 is considered undervalued and vice versa. Over the past 10 years, Hartalega has achieved a CAGR of 20.09% in shareholders’ earnings (RM84.5 million in 2009 to RM438.9 million in 2018). Based on this, Hartalega’s PEG ratio is 2.5 – an overvaluation at current prices.

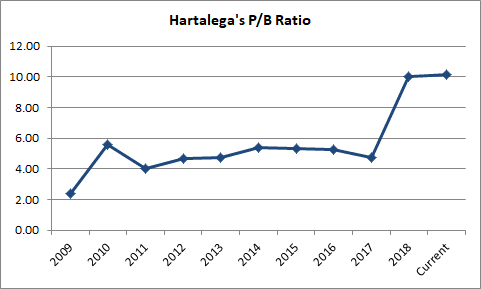

11. P/B ratio. As at 31 March 2018, Hartalega has RM0.603 in book value a share. At RM6.78 a share, Hartalega’s current P/B ratio works out to 11.3 — the highest recorded over the last 10 years.

Source: Data obtained from Hartalega annual reports

12. Dividend yield. Effective from FY 2018, Hartalega revised its dividend policy to distribute a minimum of 60% of annual net profits to shareholders as dividends, an increase from a minimum of 45% previously. For 2018, the board declared 7.95 sen in dividend per share, which is 60% of 13.3 sen in EPS. If Hartalega maintains its dividend per share at 7.95 sen, its dividend yield works out to 1.17% — lower than the fixed deposit rates of 3.0-3.5% offered by Malaysian banks presently.

The fifth perspective

In short, Hartalega has built a proven track record of growing sales, earnings, and dividends to shareholders over the past 10 years. The company has maintained a strong balance sheet and provided an open discussion of its growth plans at great length, which demonstrates good communication between the management and shareholders.

From an investor’s point of view, Hartalega’s stock price currently looks expensive despite the company’s great fundamentals. With its PEG ratio significantly above 1.0 and its P/E and P/B ratios at historical highs, it might be wise to wait for a better time to consider the stock.

Hi, it is 5 plants at Bestari Jaya fyi. For point no.6. Thanks!

Hi MQ,

Thanks for the comment. I checked both the Q4 2018 and Q1 2019 reports of Hartalega:

– From Q4 2018, it commissioned 4 Plants with 48 production lines.

– From Q1 2019, it commissioned Plant 5 in August 2018.

Regards

Ian