Mapletree Industrial Trust (MIT) is a SGX-listed REIT with 87 industrial properties in Singapore and 27 data centres in North America. Flatted factories and hi-tech buildings make up the bulk of MIT’s Singapore properties, and it has also sought to tap on the secular growth of data centres in North America recently.

Although MIT’s share price plunged by about 36% during March due to the pandemic, it has rebounded strongly by more than 60% to S$3.16 from its low of S$1.91. COVID-19 has certainly hit the economy hard, so I wanted to find out how MIT was responding to the challenges posed by the pandemic. Here are seven things I learned from MIT’s 2020 AGM:

1. MIT’s distribution per unit (DPU) increased by 0.7% y-o-y to 12.24 cents in FY19/20. The increase in DPU was driven mainly by the 10.5% y-o-y growth of MIT’s net property income (NPI) from acquisition and development projects in Singapore as well as contribution from the 13 newly acquired data centres in North America. DPU did not grow proportionately to the growth in distributable income (14.5%) due to the enlargement of MIT’s unit base when MIT issued a private placement in FY19/20.

The tax-exempt income of S$6.6 million in 4Q FY19/20 was not distributed to unitholders to boost MIT’s cash management due to the economic uncertainty caused by the COVID-19 pandemic. Had it been distributed, MIT’s DPU would have increased 3.1% y-o-y.

2. MIT’s aggregate leverage ratio increased from 33.8% to 37.6% as of 31 March 2020 as the USD appreciated against the SGD during this period. At 37.6%, this is still well below MAS’ regulatory leverage ratio of 50%. Assuming an aggregate leverage ratio of 40%, this gives MIT a debt headroom of S$238.7 million for investment opportunities.

MIT’s interest coverage ratio (ICR) in FY19/20 was 6.9x, up from 6.6x in FY18/19. This is a healthy ICR, which means that for the year ending FY19/20, MIT can repay its interest expense incurred almost 7 times over with its NPI.

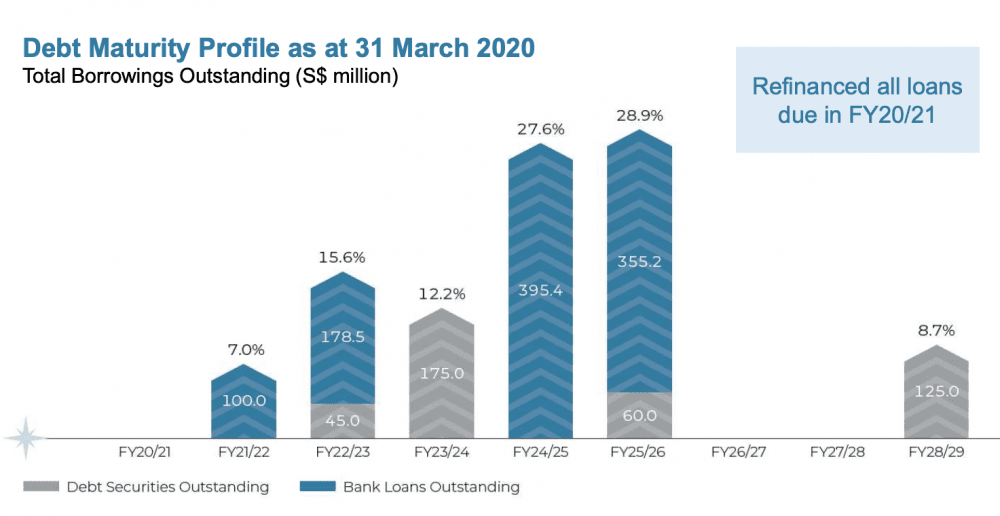

3. MIT does not have a well-spread debt maturity profile. MIT’s debt maturity profile uneased me — slightly over half of its debts are due in FY24/25 and FY25/26 alone. Although those loans are still some years away from maturing, I hope MIT can refinance some of those debts so that its debt maturity profile is more well-spread.

Source: Mapletree Industrial Trust 2020 AGM presentation slides

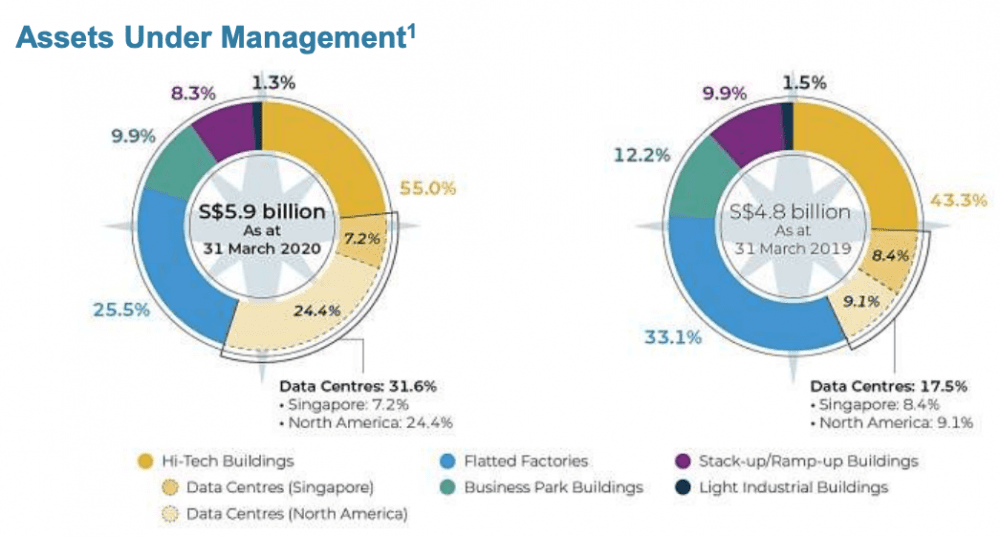

4. MIT acquired 13 data centres in North America — 12 in the U.S. and one in Canada in the later part of FY19/20. This acquisition effectively increases the share of data centres in MIT’s portfolio to 31.6% as of 31 March 2020, from 17.5% in 31 March 2019. The management said that MIT is actively looking to invest more in data centres and the share of data centres in MIT’s portfolio is expected to be more than 50% (though they did not specify nor estimate a time).

I’m glad MIT expressed its desire to increase its portfolio’s exposure to data centres. Given the explosion of data with the fourth industrial revolution well underway, data centres are going to be needed more than ever.

Source: Mapletree Industrial Trust 2020 AGM presentation slides

5. MIT’s Singapore properties face a challenging operating environment due to COVID-19. All of MIT’s Singapore properties remained open during the circuit breaker period from 7 April to 1 June 2020, with about 70-80% of its tenants continuing operations as they are essential services. Post-circuit breaker, about 90% of MIT’s tenants have continued/resumed business operations.

SMEs account for about 45% of MIT’s gross rental income and they have been more severely affected by supply chain disruptions and fall in business volume due to the pandemic. With Singapore’s GDP growth forecast to be -7.0% to -4.0% for 2020, MIT might not have an easy time ahead.

6. On a brighter note, MIT’s data centres which are mainly located in North America are expected to receive robust demand. All data centres are identified as essential infrastructure and remained open during the pandemic. Moreover, the pandemic has accelerated the digital transformation of companies, with the subsequent adoption of AI and cloud computing bound to drive the explosion of data. Subject to unitholders’ approval, MIT will be acquiring the remaining 60.0% interest in the 14 data centres located in the U.S., currently held by Mapletree Redwood Data Centre Trust.

7. The management shared plans on how they intend to navigate the adverse impact posed by the COVID-19 pandemic. To support its tenants, MIT provided up to S$13.7 million in rental rebates to support its tenants, with priority given to SME tenants. Together with government regulations that require landlords to support tenants as well, MIT estimates the rental relief provided to tenants to total S$20 million.

MIT is also anchored by a large diversified tenant base of more than 2,200 tenants with minimal dependence on any single tenant or trade sector. In such uncertain times, no business is guaranteed financial viability and MIT has done well in protecting itself from shocks to any of its tenants or sectors. Data centers also generally come with long leases and MIT’s recent acquisitions of data centers help ensure some portfolio resilience.

MIT is also quite financially flexible with its loans due in FY20/21 refinanced in 4Q FY19/20. MIT also has committed facilities of S$380million available for drawdown and sufficient debt headroom to expand either through acquisitions or asset enhancement initiatives.

The fifth perspective

MIT’s move toward the data centre industry looks to be a strong growth driver for the REIT over the next few years as our lives become increasingly digitised.

However, MIT’s share price has largely recovered since the COVID-19 crash and its dividend yield currently sits at 3.3%, which is on the low side. As an income investor, I may prefer to wait for a better price/yield if I were looking to invest in MIT.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

The points made about gearing and debt maturity are really something worth taking notice of. It’s also worth considering that MIT’s increased diversification into the US market brings with it some currency risk.

At some stage interest rates are going to rise. If that comes at the wrong time it could bite MIT’s investors.

Although MIT has been a fantastic investment for me personally (19.4% CAGR over 4.5 years!) I don’t like that they keep having placements when they want more capital. Why not rights issues?

I’ve already taken out a lot of profits along the way. Maybe it’s time to sell at bit and lock in more gains now that the yield is below the Singapore market average? (Valuation looking too rich to buy)

Hi Jonathan,

You’ve raised important points. I share your frustration that MIT prefers using placements as a equity raising option.

The raising of interest rates seem to be some time away given the expected prolonged economic downturn.

Nevertheless, MIT’s Price to Book ratio is at close to 2x so taking profits at the current trading price of SGD 3.15 is not a bad idea.

I think MIT stands on solid fundamental footing with its long term foray into data centres, especially as it leases some of its DC properties to a top DC player in Equinix.

Cheers,

Dean

How do you overcome private placement as retail investor? Do you buy off the market after announcement?

Private placements are not available to retail investors, only to institutions or high net-worth individuals. Once the private placement shares are issued, they trade on the open market at the market price just like any other ordinary share.